Goldman Sachs Finds Workers Confident About Retirement, Yet Worried About Savings

Goldman sees workers saying retirement is on track, but most still fear outliving savings as debt and household costs keep crowding out paychecks.

The confidence gap is wider than it looks

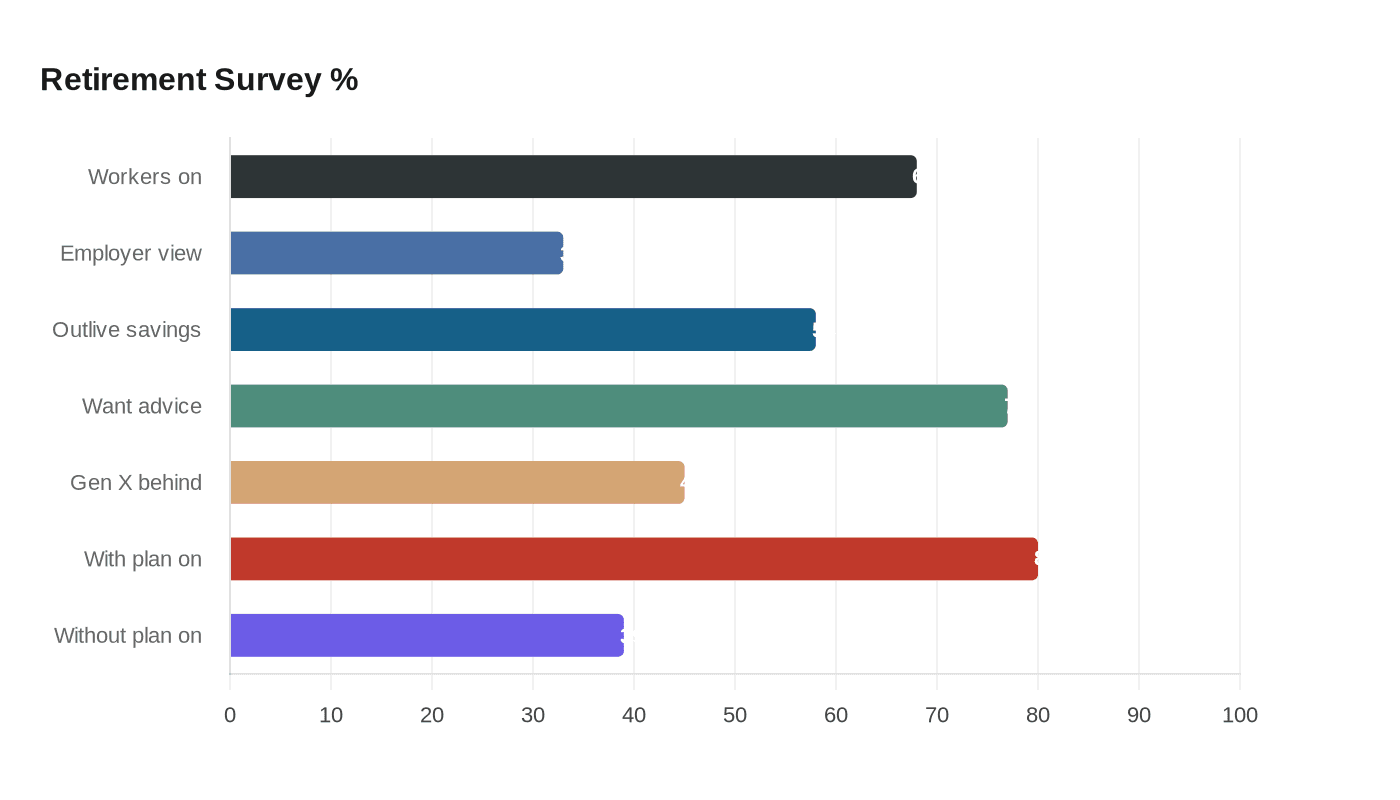

Goldman Sachs Asset Management’s latest retirement checkup lands on a familiar workplace problem: workers may feel fine about their future on paper, yet their paychecks are already spoken for. Goldman’s survey found that employers believe a median 33% of their workforce is on track for retirement, while 68% of working respondents said they are on or ahead of schedule. At the same time, 58% of those workers said they still expect to outlive their savings.

That is the squeeze in plain language. A strong salary does not automatically translate into a strong retirement if debt repayment, caregiving, education bills, and other household expenses keep taking priority every month. For Goldman employees, the message is especially relevant because compensation can look sizable in the aggregate, but bonus cycles, living costs, family obligations, and the pressure to keep up with a demanding career can make long-term saving feel optional until it is suddenly urgent.

Why the payroll math still does not work

The practical issue is not whether workers understand retirement is important. It is whether enough cash is left after the rest of life gets paid first. Goldman says the affordability problem is being pressured by debt repayment, caregiving, education expenses, and other household costs, which means the challenge is not limited to lower earners or people without access to a plan.

That matters inside a firm like Goldman because high compensation can mask fragility. A worker may be earning a healthy total package, but if a large share goes to rent, childcare, student loans, elder care, or other recurring obligations, the monthly decision becomes immediate: contribute more to retirement, or preserve liquidity for the next bill. In that setting, retirement savings often lose to near-term cash flow, even when the worker is ambitious, well compensated, and serious about career progression.

Who is falling behind fastest

Goldman’s earlier research helps identify where the pressure is sharpest. In its 2024 Retirement Survey & Insights Report, more than 60% of working respondents said they expected to delay retirement because of competing priorities. The same survey found that 77% most wanted retirement investing and advice from their employers, which is a strong signal that workers are not asking for another glossy benefits brochure. They want help making the math work in real life.

The generational divide is also hard to ignore. Goldman’s 2024 survey on retirement savings found that 45% of Gen Xers were behind schedule, while Millennials were most affected by student loans, childcare, education costs, rising homebuying costs, and care for aging family members. That mix is especially important in a banking environment where workers can advance quickly on paper but still spend much of their cash flow servicing the past and funding the present. The people most likely to fall behind are often the ones in the middle of the career ladder, carrying family expenses while trying to build enough savings to preserve flexibility later.

What the numbers say about planning tools

Goldman’s 2024 data also showed that 80% of working respondents with a plan were more likely to have savings on track or ahead of schedule, compared with 39% without one. That gap is the clearest evidence in the research that access alone is not enough; usage, guidance, and structure matter just as much.

In practical terms, that means employees need more than eligibility for a retirement plan. They need personalized assumptions, plan-specific guidance, and tools that help them decide how to save when cash is tight. For a Goldman employee balancing a demanding job, long hours, and a career path shaped by performance reviews and bonus cycles, the difference between having a plan and using it well can determine whether retirement stays a distant goal or becomes a real target.

Why employers cannot assume confidence equals readiness

Goldman’s 2026 survey shows a striking disconnect between how employers see their workforce and how workers see themselves. That split suggests that many employees may feel they are making progress simply because they contribute something, or because their income sounds strong relative to peers. Yet the fact that 58% still think they will outlive savings points to a deeper unease about whether current contributions are actually enough.

This is where retirement benefits increasingly get judged like any other workplace tool: not by whether they exist, but by whether they help people handle volatility. Goldman’s conclusion is that traditional plan design alone may not solve affordability problems. Employers may need to move further toward guidance, advice, personalization, and practical planning tools that reflect each worker’s actual expenses, savings rate, and stage of life.

The broader market is saying the same thing

Goldman is not alone in seeing the strain. The Employee Benefit Research Institute’s 2026 Retirement Confidence Survey found that 64% of Americans felt confident they had enough money to live comfortably throughout retirement, down from last year. Workers’ confidence fell to 61%, and 65% said debt is a problem for their household, with one-quarter calling it a major problem. That combination mirrors Goldman’s theme: confidence can coexist with financial pressure.

Transamerica’s 2026 retirement survey points in the same direction. It found that 59% of U.S. residents believe they are building or have built a large enough retirement nest egg, while estimated median retirement-account savings among those not retired rose only from $44,000 in 2020 to $56,000 in 2025. Those figures suggest progress, but not enough to erase the sense that many households are still far short of where they need to be.

BlackRock’s 2025 Read on Retirement survey adds one more layer to the employer-employee mismatch. It found that 64% of workplace savers felt on track, while only 38% of employers believed the majority of employees were on track. That gap reinforces the same lesson Goldman is signaling: workers and plan sponsors often see retirement readiness very differently, and employers need better ways to close the distance.

What Goldman employees should take from this

For Goldman workers, the story is not simply about a retirement plan tucked inside a broader benefits package. It is about whether current pay, short-term obligations, and long-term goals are aligned well enough to make retirement saving sustainable. The people most at risk are not just lower earners; they are the employees carrying the heaviest mix of student debt, childcare, housing costs, and family responsibilities, especially those in the middle years of their careers.

The firm’s own research points to the fix: more personalized guidance, more usable planning tools, and retirement advice that accounts for what workers are actually paying every month. In a business where prestige, performance, and compensation are all supposed to create options, the real test is whether employees can turn those earnings into durable security before the next round of costs eats the margin away.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?