Goldman Sachs: Japan can fund about 30 more yen interventions

Goldman says Japan has room for about 30 more yen interventions, but the bigger signal is when Tokyo chooses to use that firepower. The last move was roughly $35 billion.

Goldman Sachs’ read on Japan is less about how much ammunition Tokyo has left than how carefully it will use it. The bank estimates the Ministry of Finance could still mount about 30 more yen interventions at last week’s scale, a sign that markets should treat each move as a timing decision, not a last stand. For macro traders, corporate treasurers and multinationals with Japan exposure, that means the real risk is a sudden, well-timed strike that punishes crowded short-yen positions.

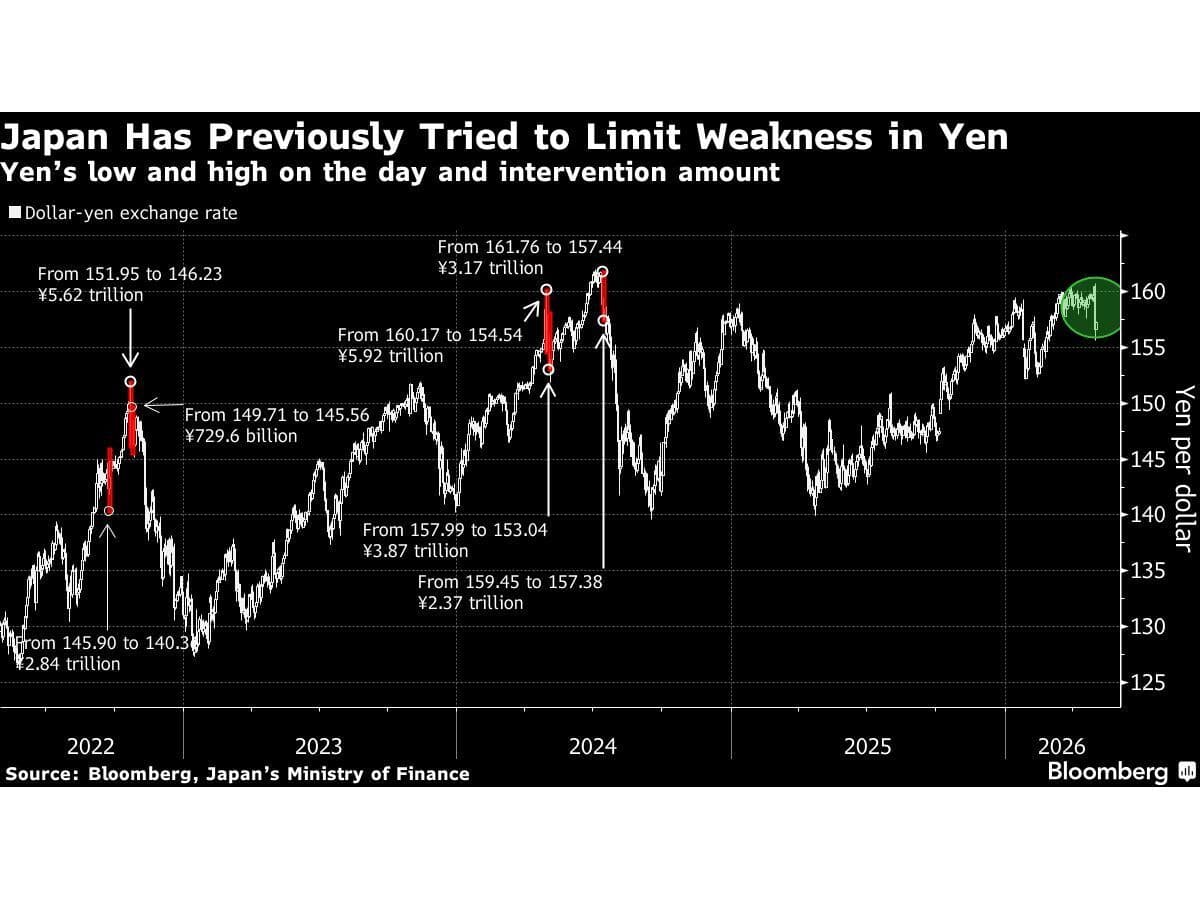

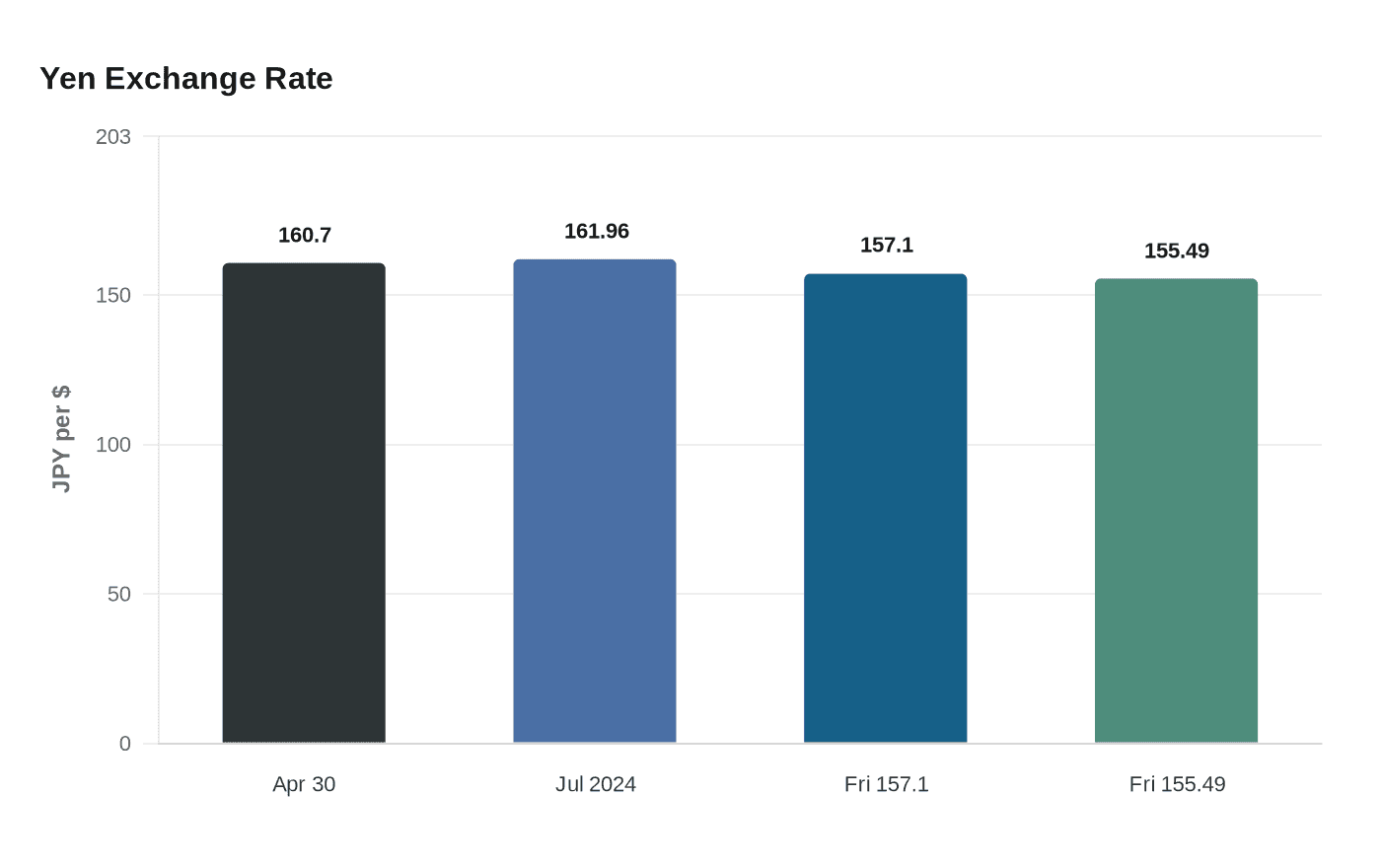

Japan’s latest intervention came on Thursday, April 30, after the yen slipped past 160 per dollar and briefly touched 160.7, its weakest level since July 2024. Central bank data released Friday suggested authorities may have spent as much as 5.48 trillion yen, or about $35 billion, to defend the currency. That was just shy of the roughly $36.8 billion Tokyo spent in July 2024, when the yen sank to 161.96 per dollar, a 38-year low.

Goldman Sachs economist Yuriko Tanaka said the estimate of about 30 additional interventions was based on Japan’s current foreign-exchange reserves. Those reserves were about $1.37 trillion in March 2026, and earlier this year they were around $1.4 trillion, giving officials plenty of room to act if they want to keep pressure on speculators. Atsushi Mimura, Japan’s top currency diplomat, warned on Friday that speculative positions were still in the market, signaling that another intervention remained possible.

The immediate market reaction showed how sensitive positioning has become. The yen strengthened from around 157.1 per dollar to 155.49 in early London trading on Friday before easing back, while the dollar logged its biggest weekly drop against the yen since early February. That kind of intraday swing matters far beyond trading desks. Corporate finance teams hedging yen revenues, import costs and dollar liabilities can see funding assumptions shift in hours rather than weeks.

The drivers behind the yen’s weakness have not gone away. Analysts point to wide U.S.-Japan interest-rate gaps and, more recently, higher oil prices linked to the Iran war. Japanese officials have argued that a weaker yen could worsen domestic inflation, which keeps intervention on the table even after a costly move.

Mizuho strategist Jordan Rochester said Tokyo’s warning was meant to deter traders and noted that Japan has sometimes followed an initial intervention with additional action, including in 2022 and 2024. That history is why Goldman’s estimate matters: it suggests Japan still has substantial firepower, but the next move could matter more than the last one.

Know something we missed? Have a correction or additional information?

Submit a Tip