Goldman Sachs lifts insurance targets, cuts energy price forecasts

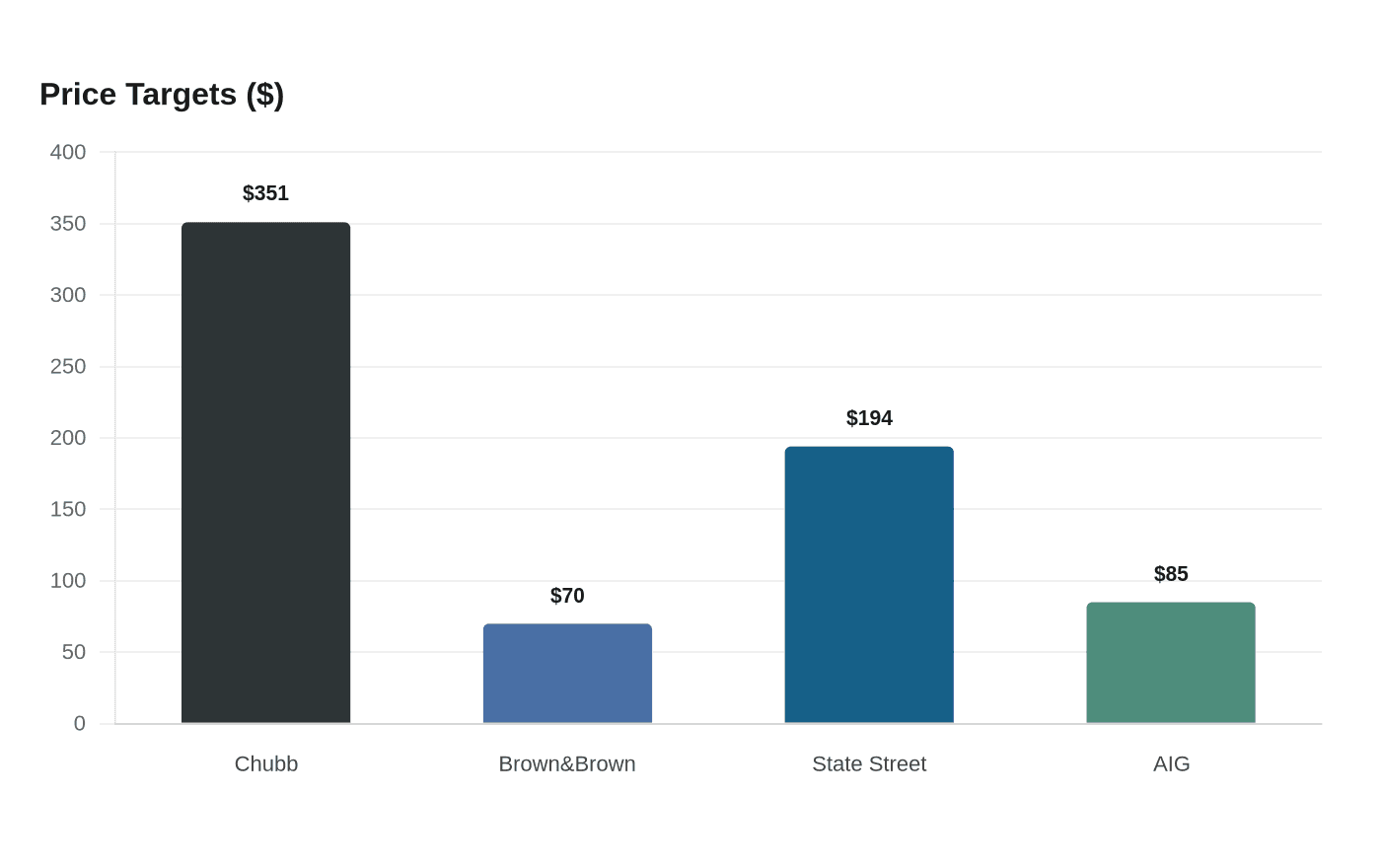

Goldman moved its conviction toward insurers and financials, lifting Chubb to $351 and State Street to $194, while trimming energy targets as crude pressure lingered.

Goldman Sachs shifted its sector call toward insurers and other financials, raising targets on Chubb, State Street and Brown & Brown even as it cut price forecasts across energy names including ConocoPhillips, Devon and EOG. The pattern points to a sharper preference for balance-sheet strength, capital deployment and earnings visibility over commodity exposure.

The clearest bullish call was on Chubb, where Goldman lifted its price target to $351 from $309 and kept a Buy rating. Goldman said the insurer can sustain a core operating return on equity of about 14% and pointed to capital deployment as a support for shareholder returns. In Goldman’s earlier October 2025 work, the bank said Chubb could deploy roughly 90% of operating earnings over the next two years, a level that reinforces the stock’s appeal in a market that has rewarded steady capital return more than cyclical growth.

Goldman also nudged Brown & Brown higher, raising its target to $70 from $62 while holding a Neutral rating, and moved State Street to a Buy with a target of $194 from $168. The State Street call is notable because it shows Goldman is not just favoring the obvious insurer trades. It is also leaning into financial names where higher rates, fee income and capital management can translate into more durable earnings than the energy group is offering right now.

American International Group has been another moving part in the same rotation. Goldman raised AIG’s target to $90 from $83 on March 5, citing improving earnings growth and return on equity, then later cut it to $85 from $90 after second-quarter 2025 results as pressure on the underlying loss ratio lingered. Goldman also modeled about $1.5 billion in net premiums written for 2026 from AIG’s renewal rights deal and quota share, while trimming projected share buybacks by $1.5 billion.

The energy downgrade lands in a different market. ConocoPhillips said on Feb. 5 that it would cut capital and operating costs by $1 billion in 2026 after weaker crude prices hurt profit. That kind of margin pressure is the backdrop for Goldman’s lower targets on ConocoPhillips, Devon and EOG, and it is the kind of message that matters for coverage teams deciding where client conversations will cluster next.

Goldman’s broader 2026 outlook remains constructive, with the firm expecting global growth of 2.8%, U.S. GDP above consensus and resilient corporate earnings. That makes the sector shift look less like a broad defensive turn than a tactical preference for insurers and financials that can keep compounding even if energy stays tied to the price of oil.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?