Goldman Sachs moves to foreclose on distressed Los Angeles properties

Goldman is taking a harder line on troubled real estate, pushing the Radford Studio Center to market and confronting a separate loan that has lost 69% of its value.

Goldman Sachs is showing a tougher workout culture in Los Angeles, where credit and real estate bankers are moving from patience to payoff and, in some cases, to foreclosure. The shift matters inside the firm because it puts more pressure on lending, special situations, and commercial real estate teams to recognize losses faster, market assets aggressively, and defend decisions that once might have been extended again.

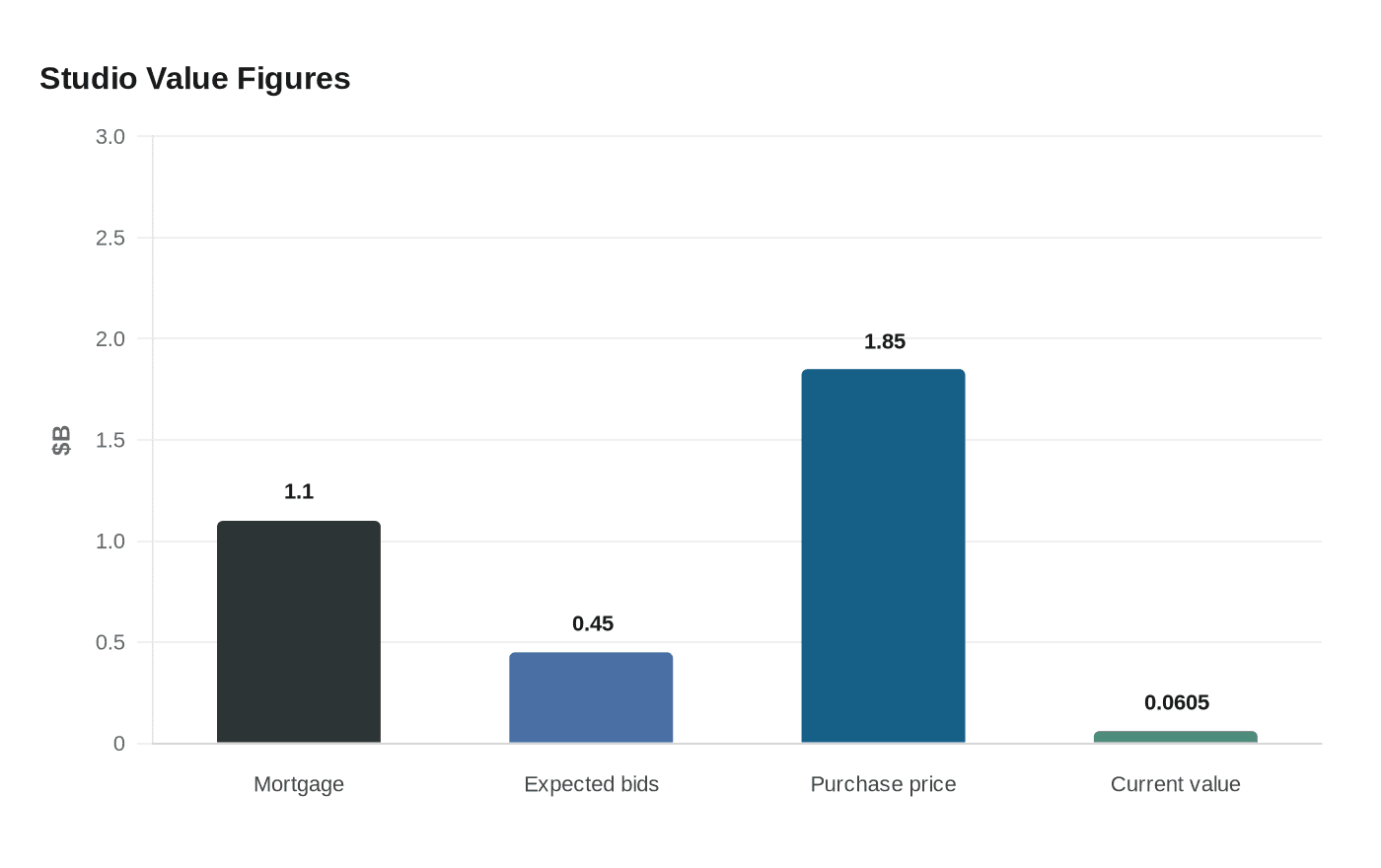

The clearest example is the Radford Studio Center in Studio City. Goldman took over the 55-acre, roughly million-square-foot studio lot after Hackman Capital Partners defaulted on a $1.1 billion mortgage and then hired Eastdil Secured to shop the property. Bids were expected around $450 million, roughly a quarter of Hackman’s $1.85 billion purchase price in December 2021. The asset was reported to be about 63% occupied, with 36% of space facing lease expirations that summer, as Los Angeles production slowed under the weight of strikes, cheaper overseas production, and consolidation.

That kind of sale puts a spotlight on how Goldman’s credit teams now have to think like liquidators as much as lenders. Instead of stretching a loan and hoping for a rebound, the firm is accepting that some assets will clear only at steep discounts. For bankers tied to these deals, that means more internal scrutiny, more coordination with outside brokers, and more reputational risk if a marquee property gets marked down sharply in public.

Goldman is facing a similar pressure point at Cerberus Capital Management’s Wedbush Center in downtown Los Angeles. Goldman originated the $128 million CMBS loan in 2018, but the tower’s value has fallen to $60.5 million from $197.5 million at issuance, a 69% drop over about seven years. Downtown Los Angeles office vacancy was reported at 34%, underscoring how hard it is to refinance or rescue weak office assets in the current rate environment.

The broader backdrop is even harsher. Lenders are increasingly selling troubled commercial real estate debt at discounts as large as 85% below payoff value, signaling the end of the old extend-and-pretend playbook. Deutsche Bank’s move to foreclose on Kaufman Astoria Studios after Hackman Capital defaulted on a $340 million loan that matured on Nov. 9, 2025, with the balance rising above $359 million, shows the same pattern. For Goldman employees on the front lines of these workouts, the message is unmistakable: preserve optionality when you can, but expect faster loss recognition, harder negotiations, and fewer chances to kick the can down the road.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?