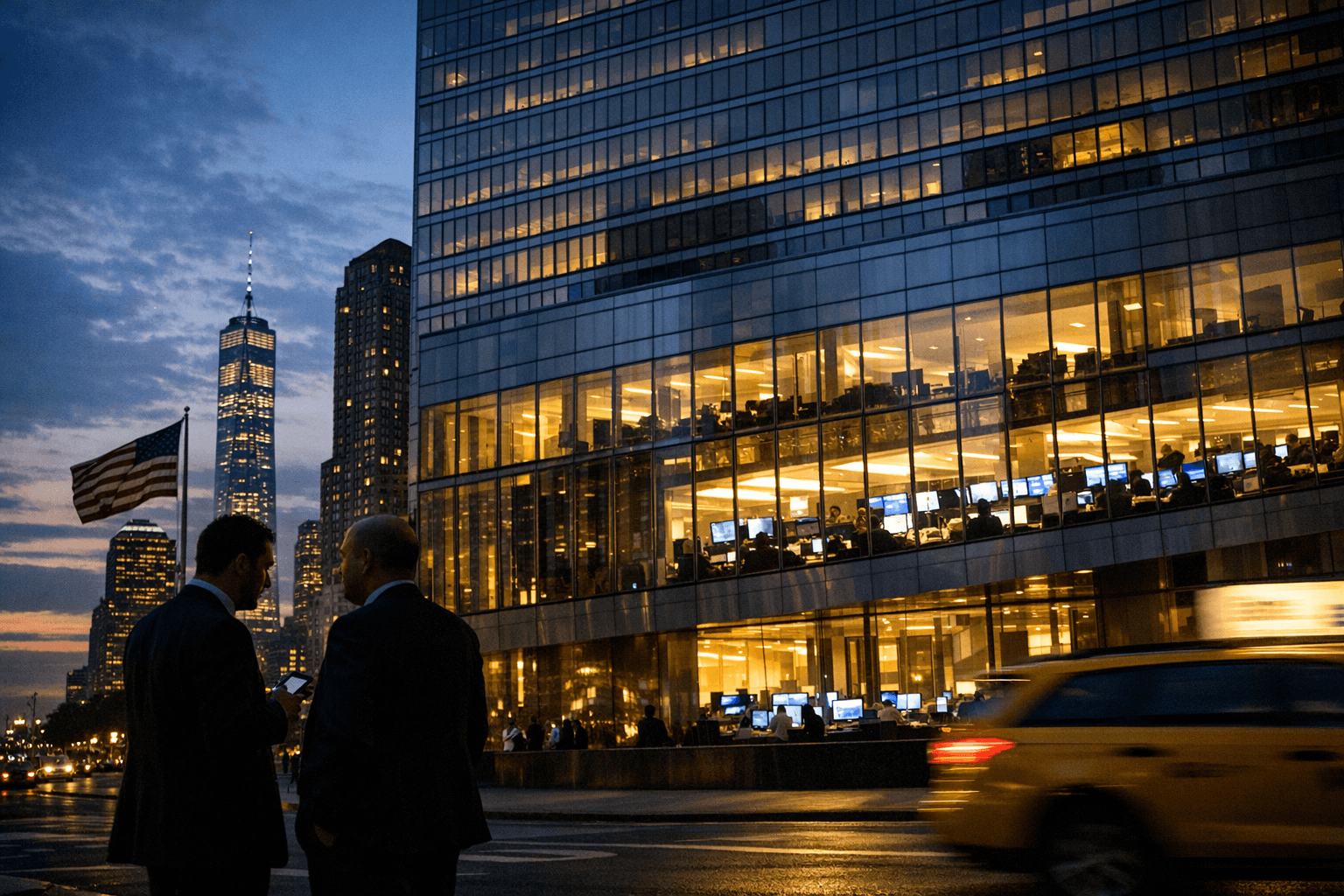

Goldman Sachs returns to investment-grade debt market with three-tranche sale

Goldman went back to the debt market after a $5.63 billion quarter, signaling it wants to lock in funding before volatility pushes borrowing costs higher.

Goldman Sachs went back to the U.S. investment-grade debt market just after posting a $5.63 billion first-quarter profit, a move that shows the bank is still using balance-sheet timing as an active part of its playbook even when business is strong. The new offering spans three tranches with maturities from four to eight years, and the longest piece was being discussed at about 1.25 percentage points over Treasuries.

The sale followed a quarter in which Goldman reported $17.23 billion in net revenues, $17.55 in diluted earnings per share and a 19.8% return on equity. Global Banking & Markets generated $12.74 billion, up 19% from a year earlier, while investment-banking fees jumped 48% to $2.84 billion. Equity trading set a record at $5.33 billion, but fixed income, currencies and commodities revenue slipped 10% to $4.01 billion, underscoring how uneven the quarter was beneath the headline profit.

For employees across trading, financing and treasury functions, the message is straightforward: Goldman is using a strong earnings window to secure funding before market conditions move against it. The bank had already raised $16 billion in January in the largest investment-grade bond sale ever by a Wall Street bank, a six-tranche deal that stretched from three to 21 years and eventually priced the longest tranche at 0.8 percentage point over Treasuries. This latest borrowing suggests management still sees value in staying ahead of the funding curve rather than waiting for tighter spreads.

The timing also lines up with a broader burst of bank issuance after first-quarter results. Lenders have been trying to front-load borrowing before volatility makes debt more expensive, and banks were expected to dominate about $40 billion of investment-grade issuance in the same week Goldman returned to market. Bloomberg Intelligence has pointed to AI disruption and the war in Iran as forces that have unsettled risk markets and kept bank bonds sensitive. That backdrop matters inside Goldman, where higher borrowing costs can filter into everything from financing desks to risk appetite and capital planning.

Goldman’s own balance-sheet metrics help explain why it can move opportunistically rather than defensively. At the end of 2025, the firm reported a 14.3% standardized CET1 ratio, a 126% average daily liquidity coverage ratio and $501 billion in total deposits. It also said 2026 included about $4.2 billion of contractual maturities and about $26.7 billion of debt that had been called or was eligible to be par-called as of Dec. 31, 2025. In a quarter when dealmaking and trading both strengthened, management appears to be using the debt market to preserve flexibility, not to plug a hole.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?