Goldman Sachs Rides $1.38 Trillion M&A Wave in Strong Q1 2026

Goldman captured outsized advisory fees from a $1.38 trillion Q1 M&A surge. For deal teams, that means fatter bonus pools and more late nights ahead.

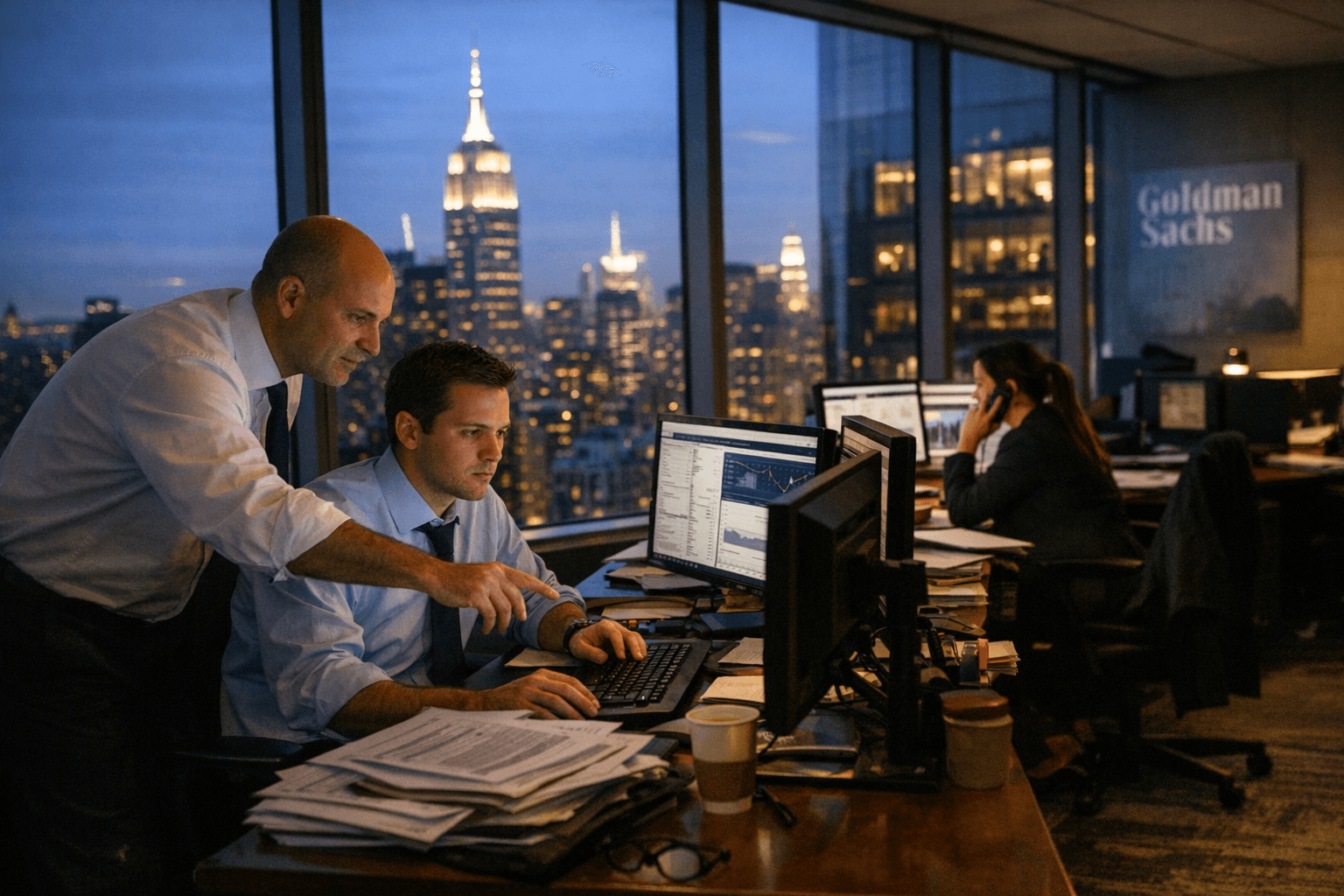

Global M&A volume hit $1.38 trillion in the first three months of 2026, and Goldman Sachs positioned itself among the clear winners of that surge alongside JPMorgan, capturing what analysts described as an "advisory windfall" as corporate boards pursued large-scale, transformational transactions at a pace not seen in recent years.

The driver behind the volume spike is structural. AI adoption, cloud buildout, and energy infrastructure investment have pushed companies toward strategic consolidation at scale, producing a pipeline of megadeals that disproportionately benefit banks with broad sector coverage, cross-border reach, and execution depth. Goldman historically ranks at the top across those dimensions, giving it an outsized claim on the fee wallet generated by first-quarter deal activity.

For analysts and associates on M&A and coverage teams, that translates directly into deal load. A $1.38 trillion quarterly volume doesn't flow through the system without material increases in modeling, documentation, client management, and execution work. Junior bankers should expect more live deals running simultaneously, compressed timelines when clients push for rapid closes, and extended on-call windows that characterize any active M&A cycle. The compensation upside is real; so is the near-term burn.

At the VP and managing director level, the Q1 surge sharpens the stakes around mandate capture. Winning a marquee deal in a high-volume quarter isn't just a revenue event: it's a promotion narrative and, for those on the partnership track, a meaningful data point in candidacy discussions. Senior bankers who convert the 2026 pipeline into closed mandates stand to see both direct bonus upside and longer-run franchise value from the relationships built around transformational deals.

The workload pressure extends well beyond revenue-generating desks. Compliance, legal, operations, and risk functions all absorb elevated transaction volumes, and their capacity becomes a gating factor for front-office deal closings. Teams that scale those functions effectively convert deal activity into durable revenue; those that don't face execution risk and reputational exposure that lingers past any bonus cycle. For control and compliance staff, the Q1 pickup means heightened documentation volume and regulatory scrutiny without a guaranteed direct lift to variable pay.

Coverage and execution teams should also expect accelerated hiring in deal execution and product functions, with potential contract support for modeling tasks serving as a near-term bridge. If the 2026 M&A rebound holds through Q2, it would represent a meaningful reweighting of the firm's annual revenue mix toward advisory, reinforcing precisely the desks and skill sets that have historically defined the Goldman partnership track.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?