Goldman Sachs says AI is pushing up prices for gadgets and power

Goldman says AI is hitting budgets first through pricier devices, software renewals and power bills. For bankers and clients, the squeeze is here before the productivity payoff.

The first AI bill shows up in procurement, not in a headline inflation print

Goldman Sachs’ read on AI cost pressure starts with three concrete channels that matter inside offices and on client budgets: higher electronics input prices, AI-linked software pricing, and rising electricity demand from data centers. That is the part worth watching for analysts building expense models, associates renewing vendor contracts, and managing directors advising clients on where the next round of cost pressure lands first.

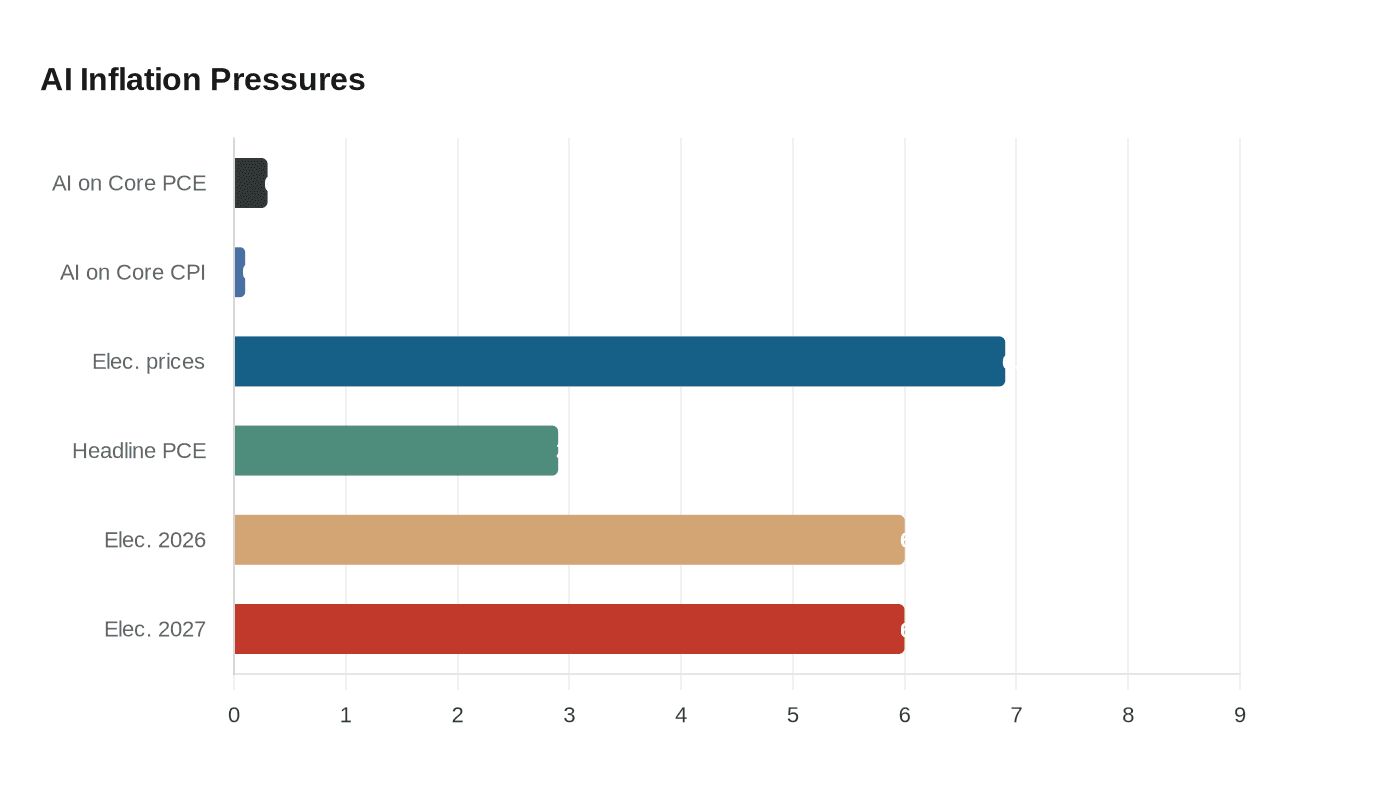

The bank’s point is not that AI has become a pure inflation story. It is that the costs are arriving before the savings. Goldman estimates AI-related price pressures have added about 0.3 percentage points to annual core PCE inflation and about 0.1 percentage point to core CPI over the past year, with a similar impact likely over the next year. Longer term, Goldman still expects AI to become disinflationary as productivity gains spread and lower production costs. Right now, though, the line items showing up in budgets are the ones tied to hardware, software, and power.

Hardware costs are moving first, and that is where employees will notice it

Goldman strategist Manuel Abecasis says strong demand for AI infrastructure has raised prices for key electronic components, which has already pushed up the cost of computer accessories and is likely to lift smartphone and computer prices in the coming months. That matters inside Goldman because device refresh cycles are not optional. Every extra dollar spent on laptops, monitors, peripherals, and mobile hardware is one more dollar that has to be justified in the annual planning process.

For a bank with a culture that prizes responsiveness, speed, and polished client service, this is not a trivial squeeze. Internal IT teams and business managers can absorb higher hardware costs only by cutting somewhere else, whether that means slower refresh schedules, tighter headcount growth, or less room for discretionary spend. The effect is small on any single desk, but in a platform where compensation, bonus pools, and operating budgets are all under constant review, it compounds fast.

Software vendors are using AI features to reprice the same old workflow

The second transmission channel is more subtle but often more painful. Goldman says software firms have been lifting prices as they add AI features. That means the cost of using the tools Goldman employees rely on every day can rise even when the underlying workflow looks unchanged.

For finance teams, that creates a familiar problem: separating genuine productivity gains from forced upgrades. If a vendor bundles AI into a license renewal, the question is not whether the feature sounds useful. The question is whether the firm is paying more for a capability it actually needs, or simply funding the vendor’s pricing power. That distinction matters for procurement, for budget planning, and for client advice, especially when Goldman bankers are helping companies model operating expenses in a slower-growth environment.

It also changes how leaders inside the firm think about vendor negotiations. A software line item that looked stable a year ago can turn into a moving target if the supplier decides AI is now a premium feature. That is the sort of cost inflation that gets discussed quietly in internal reviews long before it reaches any macroeconomic debate.

Power demand is the biggest structural pressure, and it is already regional

The third channel is electricity. Goldman says higher electricity demand from data centers is increasing power prices in some U.S. regions, and that is where the AI story starts to feel less like a technology trend and more like an infrastructure constraint. Goldman’s February note said U.S. electricity prices rose 6.9% year over year through December 2025, well above headline PCE inflation of 2.9%. The bank now expects consumer electricity inflation to run around 6% in 2026 and 2027 before easing to about 3% in 2028.

Goldman also says data centers will account for about 40% of total power demand growth over the next five years. That is a huge number for utilities, real estate teams, and any client deciding where to build, expand, or locate operations. The pressure is already showing up in tighter regional power markets in the Midwest, California, and the Mid-Atlantic if supply growth stays slow.

For households, the burden is not evenly shared. Goldman estimates higher electricity prices could trim consumer spending growth by roughly 0.2 percentage points in 2026 and 2027, with lower-income households hit harder because power takes up a bigger share of their budgets. For Goldman clients, that is not just a consumer angle. It is a demand-side warning: if utilities and regulators let electricity costs drift higher, you eventually feel it in sales, margins, and regional business planning.

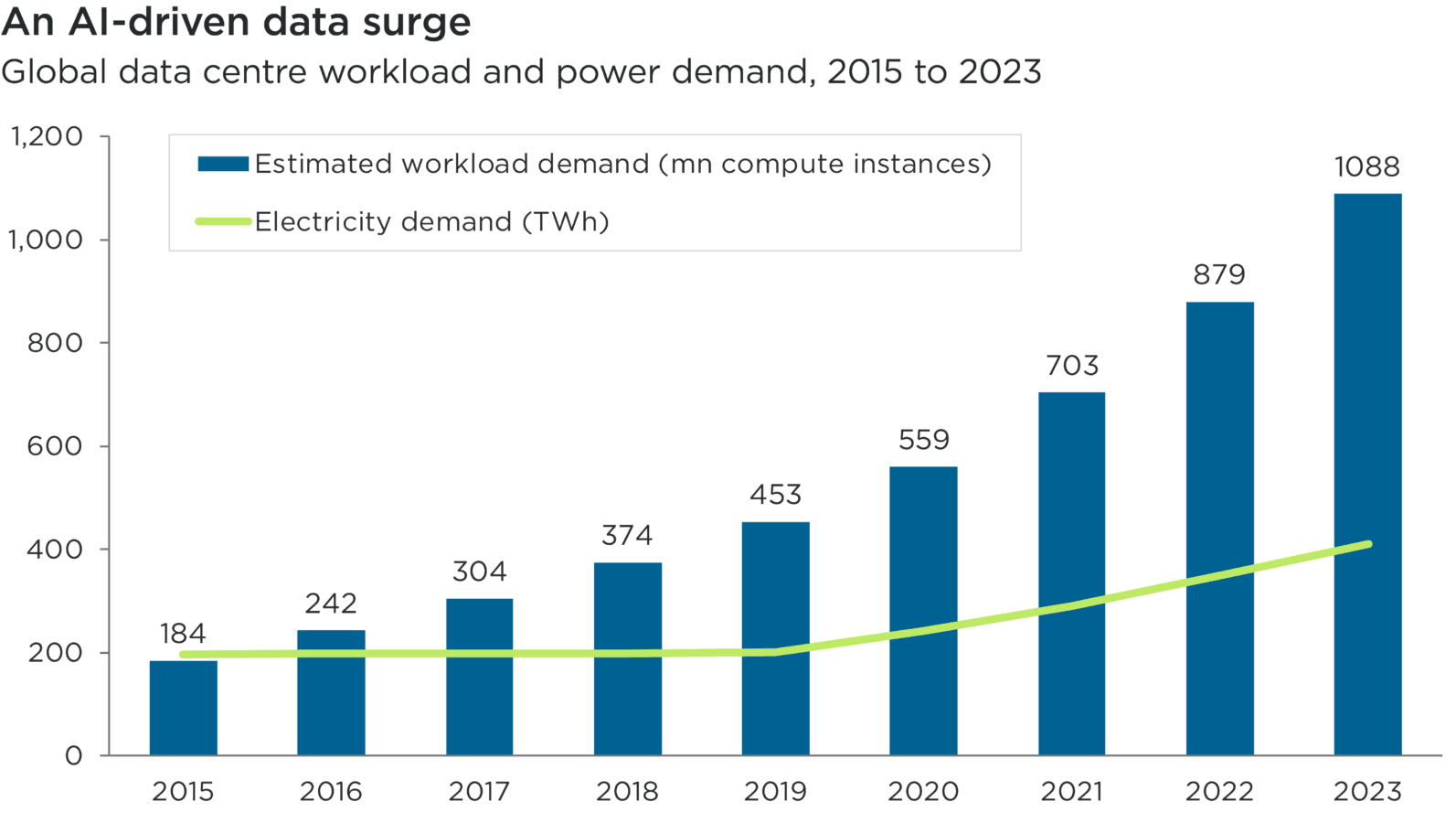

The infrastructure boom behind AI is much larger than most people realize

Goldman’s broader infrastructure work shows how large the spending wave already is. The bank expects global data-center power demand to rise 50% by 2027 and as much as 165% by 2030 versus 2023. In its baseline case, AI would account for 27% of data-center power demand by 2027. Big tech companies are expected to invest $1 trillion in AI by 2027, and Goldman says about $5 trillion in funding may be needed for digital infrastructure and power.

That scale matters for Goldman Sachs Investment Banking and for the clients it advises. About 60% of data-center demand growth by 2027 will need to be met with new power capacity, and Goldman notes the aging U.S. grid is not yet ready for AI-driven growth. Utilities are already dealing with regulatory, permitting, supply-chain, and transmission constraints. In practical terms, that means the limiting factor is no longer just chips or software demand. It is whether the grid, the permits, and the wires can catch up.

For bankers, that creates a very different operating environment from the usual AI hype cycle. The opportunity is not only in financing the next wave of servers. It is also in the slower, messier businesses of power generation, transmission, and siting, where timing and regulation can matter as much as technology.

The politics are shifting from admiration to resistance

The first signs of backlash are already visible. Florida Gov. Ron DeSantis says he wants legislation to block utility companies from raising consumer rates when they strike deals with data centers, arguing that households should not subsidize the growth of big AI loads. That kind of reaction is likely to spread if electricity bills keep climbing while data-center investment keeps accelerating.

For Goldman employees and clients, this is the point to watch: AI cost pressure is no longer an abstract macro theme. It is changing procurement decisions, utility negotiations, regional expansion plans, and the advice bankers give to companies trying to protect margins. Goldman still thinks the end state could be lower inflation and better productivity. Before that arrives, the near-term winners are the vendors who can charge more, and the businesses left figuring out how to pay for the upgrade.

Know something we missed? Have a correction or additional information?

Submit a Tip

.png&w=1920&q=75)