Goldman Sachs says fear of missing out is fueling the rally

FOMO, not fundamentals, is now Goldman’s read on the rally, putting traders and strategists in the awkward job of explaining why clients keep buying.

Goldman Sachs is telling clients that the rally is being driven less by clean fundamentals than by fear of missing out, a message that lands hard inside the firm’s sales and trading floors. In practical terms, that means desks are spending more time explaining momentum, positioning and psychology to clients who are trying to decide whether to chase gains in the S&P 500 or lock them in.

The clearest example came in Goldman’s April 17 note, “Chase or Fade the Rally?: Bobby Molavi on the Equity Bounce.” Molavi, head of European Execution Services in Goldman Sachs Global Banking & Markets, said U.S. equities had rebounded from their late-March lows to all-time highs. The point was not just that stocks had recovered. It was that the market had gotten to a level where even bullish clients had to ask whether they were buying into strength or buying the last stretch of it.

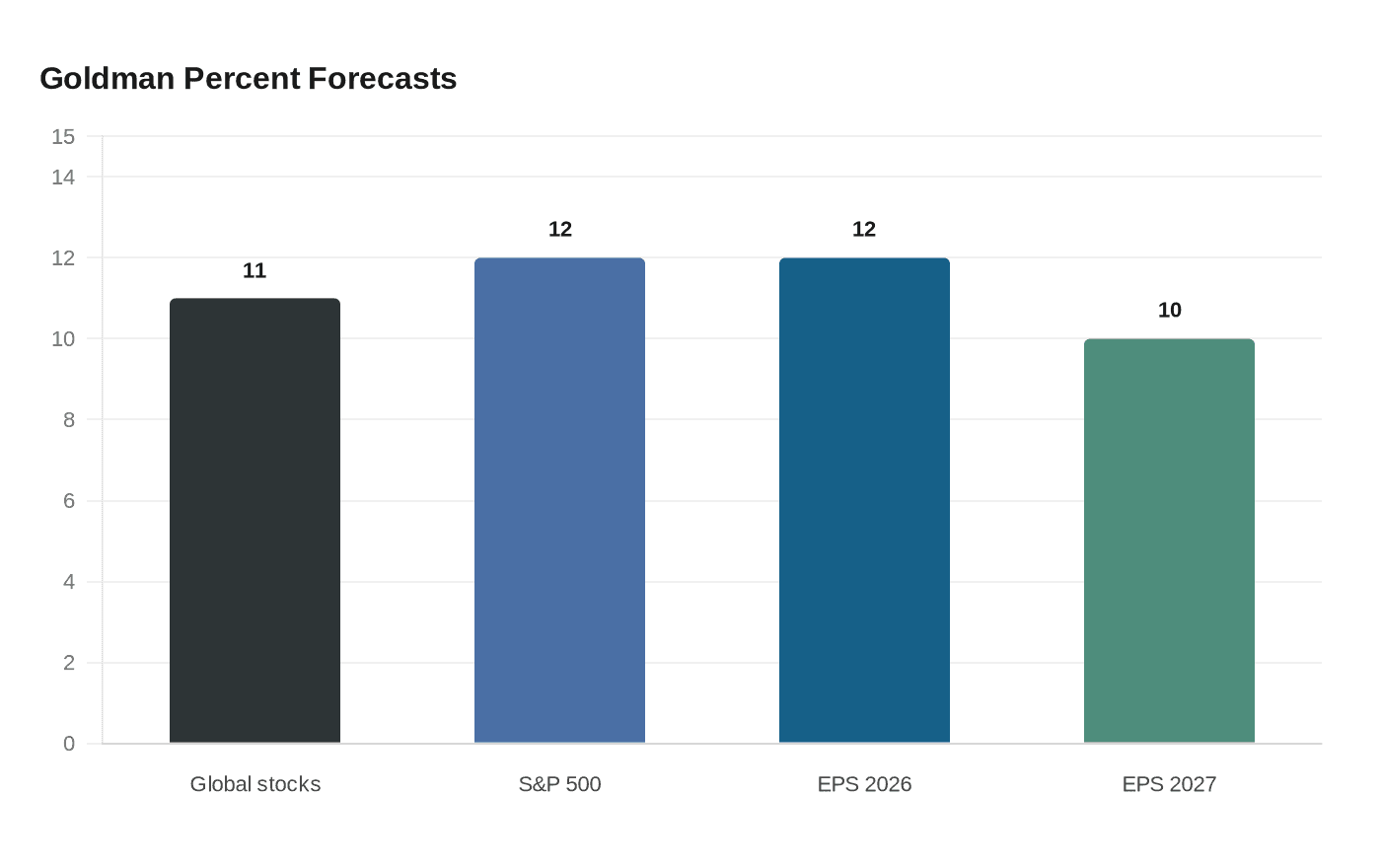

That tension matters on the trading desk because it changes the conversation with clients. When momentum outruns fundamentals, salespeople have to field the same question in different forms: is this still a market to add risk to, or one to fade into strength? Goldman’s own research suggests the firm is not dismissing the rally. Its 2026 outlook page says global stocks are projected to return 11% over the next 12 months and the S&P 500 is expected to rally 12% this year. But that bullish baseline sits alongside a more cautious read of how markets are behaving in real time.

On April 24, chief U.S. equity strategist Ben Snider projected the S&P 500 would rise 6% to a year-end target of 7,600, citing expected earnings-per-share growth of 12% in 2026 and 10% in 2027. That gives the research team a clean fundamental case. It also gives bankers and traders a harder job, because they still have to justify why a market that has already ripped back to records can keep running without making clients feel like they are late.

Goldman has been warning about that risk for more than a year. In January 2025, the firm said the S&P 500’s two-year rally had left equities “priced for perfection,” a line that now reads less like a market call than a warning about crowded positioning. That backdrop helps explain why the current debate at Goldman is not only about where stocks go next, but about how aggressively the firm should encourage clients to stay with a rally that everyone can see.

The irony is that Goldman’s own numbers are strong. The firm reported first-quarter 2026 earnings per common share of $17.55 and annualized return on common equity of 19.8% on April 13, and its investor-relations page listed the stock at $971.64 as of May 14. Inside the firm, that combination of strong company performance and a psychology-driven market is exactly the kind of setup that keeps sales, trading and research under pressure: clients want conviction, but the house view says conviction itself may be part of the trade.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?