Goldman Sachs says global aging is less dire, reshaping long-term investing

Goldman’s aging thesis is a growth story, not a doom loop: longer lives could lift spending, reshape client demand, and redraw sector winners.

Longer lives can be an economic growth story

Longer lives are not automatically a drag on growth. Goldman Sachs Research argues that the more important shift is not simply that populations are getting older, but that many people are staying healthier, working longer, and remaining economically active well past the old retirement script.

That matters inside Goldman because aging is not just a demographic chart. It is a client problem, a portfolio problem, a healthcare-demand problem, and a workforce-planning problem all at once. The firm’s message is that aging can pressure the economy in some places, but it can also expand the pool of productive workers, increase participation, and create new capital-allocation opportunities.

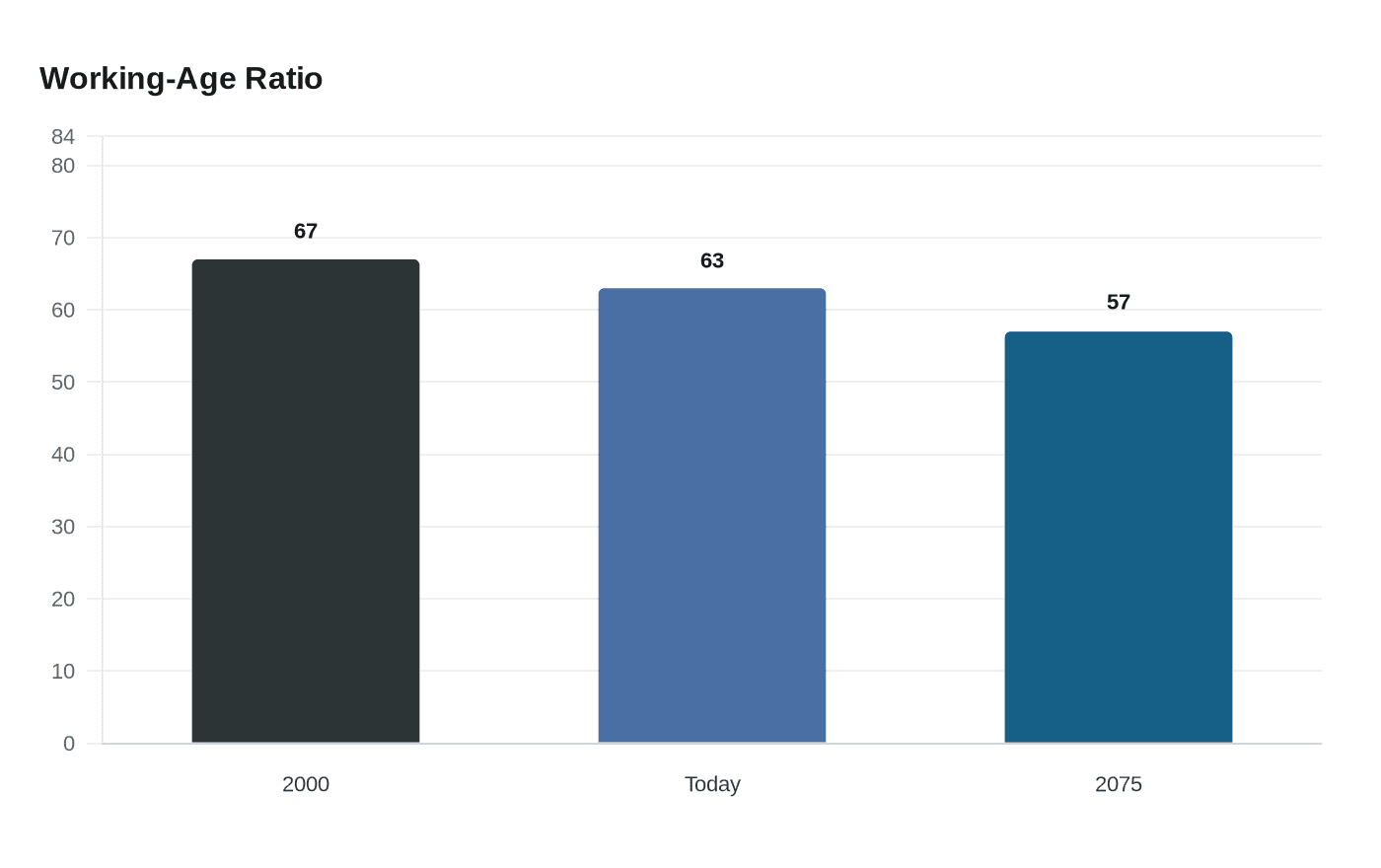

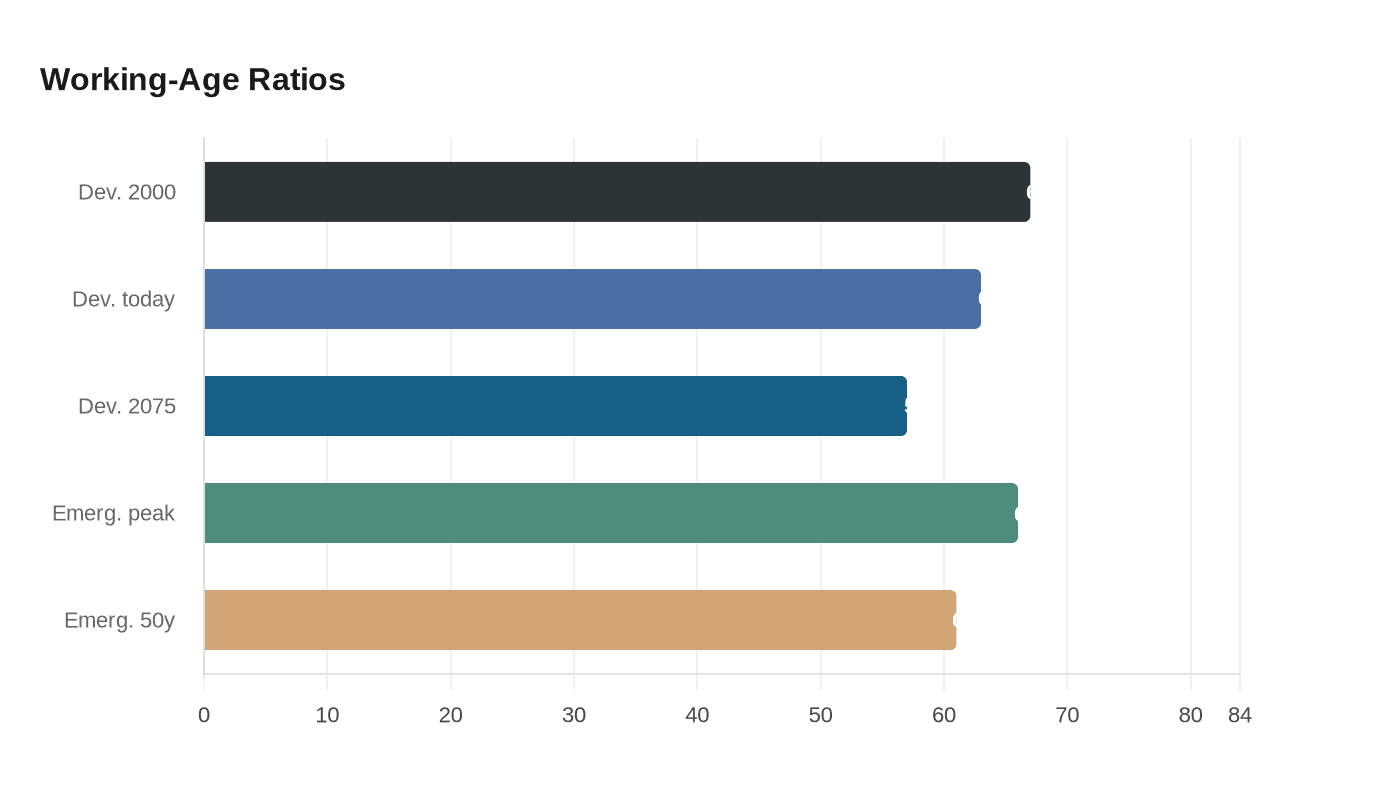

The numbers show a slower, but not collapsing, labor base

Goldman Sachs Research puts hard numbers around the shift. In developed economies, the working-age ratio has already fallen from about 67 percent in 2000 to roughly 63 percent today, and it is projected to slip to around 57 percent by 2075. In emerging economies, the share of people aged 15 to 64 is also expected to decline, from close to a peak of about 66 percent to around 61 percent over the next 50 years.

Those are meaningful changes, but they are not a straight line to economic stagnation. Goldman’s key counterpoint is that developed-market dependency ratios have actually fallen even as working-age ratios dropped, which suggests later retirement and better health can offset part of the demographic drag. The big watchout is still public finance: rising public-sector pension costs remain a concern in some economies, especially where governments are already stretched.

What it means for clients, sectors, and product strategy

For wealth management, the report is a reminder that clients think in multi-decade horizons. Retirement planning is becoming more complicated because people are funding longer retirements, dealing with intergenerational transfers, and increasingly investing around healthcare and longevity themes rather than assuming a short post-career life.

That has direct implications for the teams selling products and ideas. Demographics can support steady demand in healthcare, financial services, consumer staples, and asset management, while also creating pockets of risk for businesses that rely on younger cohorts or fast population growth. For bankers and investors, aging is less a generic warning than a lens for spotting where revenue may compound and where capital may need to move.

The practical takeaway is that longer lives change portfolio construction. If clients expect to draw income over more years, they are likely to care more about resilience, cash flow, and protection against healthcare costs, not just upside. That kind of demand can reshape everything from asset allocation discussions to the pitch book language used with family offices and retirement-focused investors.

Why this matters inside Goldman’s own talent machine

The demographic story is also a workplace story. If people work longer across the broader economy, then the firms serving them have to think differently about retirement timing, succession, and the pace at which senior talent turns over. In a place like Goldman, where career trajectory is often judged by promotion speed, bonus cycles, and the long grind toward the next seat, that can subtly change the shape of the organization.

Aging workforces can mean more experienced clients and more experienced colleagues at the same time. That is relevant for managing directors planning staffing, for bankers trying to build durable client coverage, and for younger employees weighing exit opportunities against the reality that older professionals may stay in the game longer. In other words, the labor-market story outside the firm may end up affecting the internal ladder inside it.

There is also a work-life angle that employees cannot ignore. If healthier aging expands the number of years people remain productive, then the usual assumptions about when a career peaks, when a person exits, and when someone can finally step out of long hours start to move. That has implications not only for compensation planning, but for how teams are staffed across decades rather than quarters.

The policy backdrop is mixed, not fatalistic

Goldman’s view sits in the middle of a broader policy debate. The International Monetary Fund’s April 2025 World Economic Outlook chapter on the silver economy makes a similar point: population aging can slow growth and add fiscal pressure, but healthy aging can boost labor-force participation, extend working lives, and improve productivity.

The OECD is more cautious in tone, warning in its 2025 Employment Outlook that population aging is one of the major forces reshaping labor markets and that old-age dependency ratios are projected to reach unprecedented highs in many OECD countries over the next 35 years. Put together, the picture is not one of easy optimism or straight-line decline. It is a race between demographics and adaptation.

That is why Goldman’s framing matters. The firm is not saying aging is harmless. It is saying aging is manageable if labor markets, policy, and capital markets adjust fast enough, and if longer, healthier lives are treated as an economic asset instead of only a fiscal burden.

The real lesson for Goldman employees

For employees in research, banking, and wealth management, the point is to stop treating aging as a background statistic. It will influence who your clients are, what they worry about, how long they stay invested, and which sectors can grow steadily over time.

The most useful mindset is not to ask whether aging is good or bad. It is to ask where it changes behavior first: in retirement products, in healthcare spending, in pension policy, in consumer demand, and in the way financial firms plan their own talent pipelines. Goldman’s message is that the demographic shift is real, but the winners will be the firms that recognize it early and translate it into strategy before the market fully prices it in.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?