Goldman Sachs says India’s BoP outlook supports stronger rupee than recent weakness suggests

Goldman says India’s external accounts are stronger than the rupee’s slide suggests, and it now sees a 2026 BoP surplus after two deficit years.

Goldman Sachs is leaning against the market’s latest India pessimism. In a new note, the bank said the rupee’s recent weakness looks larger than balance-of-payments fundamentals justify, and it now expects India to post a BoP surplus in calendar year 2026 after two straight years of deficits.

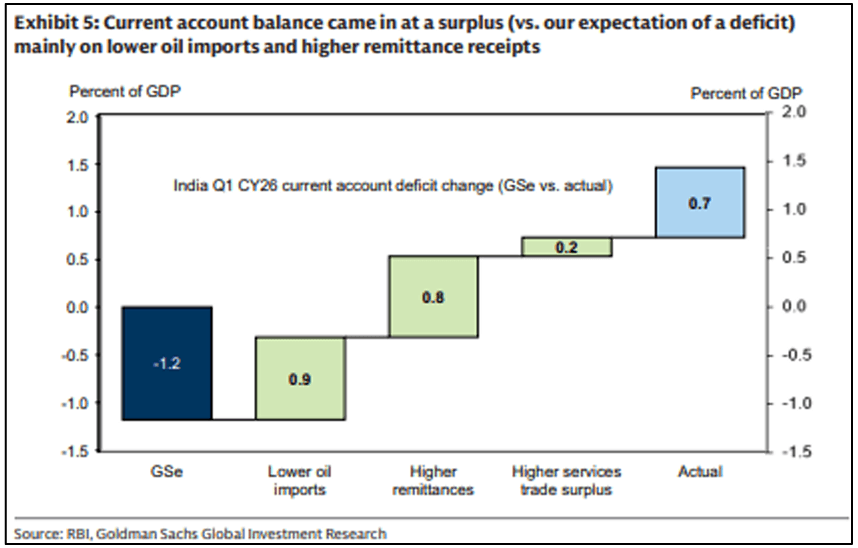

The argument rests on a cleaner external picture. Goldman cut its 2026 current-account-deficit forecast to 1.3% of GDP from 2.0%, implying a gap of about $46 billion rather than $78 billion. The bank’s economists, Arjun Varma, Santanu Sengupta and Andrew Tilton, pointed to India’s Q1 CY26 BoP surplus of $7.2 billion and a current-account surplus of about $7.0 billion, helped by lower-than-expected oil imports, stronger remittances and robust services exports.

That matters for traders because the rupee is often treated as a shorthand for India risk, even when the drivers are more complicated. Goldman said the currency’s slide reflected heightened geopolitical uncertainty and precautionary dollar demand more than a deterioration in India’s external accounts. In other words, the market has been pricing a weaker story than the data support.

The Reserve Bank of India’s own numbers back up part of that view. India’s current-account deficit narrowed to 0.2% of GDP in Q1 FY26, with the deficit at $2.4 billion versus $8.6 billion a year earlier. The services trade surplus climbed to $47.9 billion from $39.7 billion, while remittances remained a key cushion. That is not the profile of an economy losing control of its external balances.

Still, capital flows remain the swing factor. India’s BoP was in deficit in April 2026 after foreign portfolio outflows, even as the current account stayed in surplus. Goldman’s more constructive call suggests that the underlying trade and remittance engine is improving fast enough to absorb that volatility, and market reporting on the note said RBI measures could help pull in as much as $60 billion in inflows.

For Goldman staff, the practical read-through is simple. Markets teams will need to watch whether currency desks shift toward a stronger rupee bias, research teams will have to explain why a BoP surplus can coexist with choppy capital flows, and India-facing client teams may find the conversation moving from defensive positioning to selective growth. If Goldman’s call is right, India becomes less of a stress point and more of a franchise opportunity, with the rupee debate shaping client flow, internal coverage priorities and how hard the region is pitched inside the firm.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip