Goldman Sachs sees $1.6 billion outflow risk from MSCI Indonesia changes

Goldman sees $1.6 billion leaving Indonesia as MSCI cuts six stocks and keeps its free-float squeeze in place, hitting tightly held names first.

Goldman Sachs estimated that MSCI’s latest Indonesia reshuffle would trigger about $1.6 billion in passive outflows, the biggest hit for any Asian market. The selloff followed MSCI’s removal of six Indonesian companies from its Global Standard Index and underscored how benchmark changes can move a market even when company fundamentals have not changed.

The pressure comes from the mechanics of index investing. MSCI left in place a freeze on increases to foreign inclusion factors and the number of shares used in index calculations for Indonesian securities, while also ruling out new additions to its investable market indexes and any upward migration across size segments. That means passive funds tracking MSCI have to sell names that are cut, while low-free-float stocks and tightly held companies absorb the first wave of pressure.

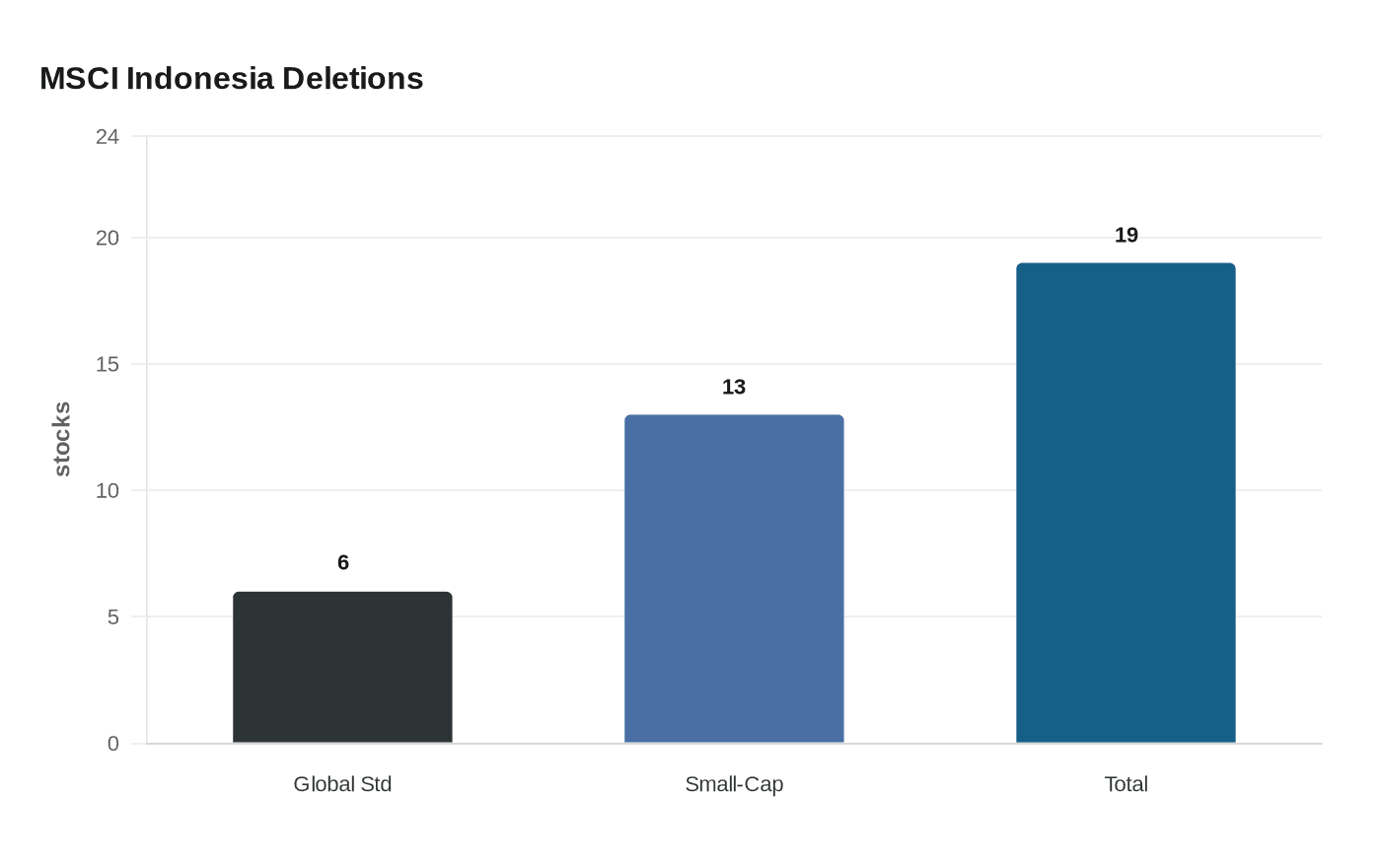

The six companies removed from the Global Standard Index were Amman Mineral International, Chandra Asri Pacific, Dian Swastika Sentosa, Barito Renewables Energy, Petrindo Jaya Kreasi and Sumber Alfaria Trijaya. Sumber Alfaria was shifted into the MSCI small-cap index rather than simply dropped. MSCI also removed 13 Indonesian stocks from its Global Small-Cap Index, bringing the total number of deletions in the May review to 19. Shares in most of the excluded names fell more than 10%, and the selling was concentrated in stocks with low free floats and heavy ownership concentration.

Indonesia’s benchmark Jakarta Composite Index fell 1.9% to 6,723.32 on May 13, its lowest level since late April 2025, while the rupiah weakened to a record low of 17,535 per dollar before recovering slightly. Foreign investors had already sold about $2.2 billion of Indonesian stocks so far in 2026, and the MSCI move added another layer of pressure heading into the May 29 rebalance and into early June, when passive funds are expected to keep adjusting positions.

The broader backdrop is a fight over market access and transparency. On April 20, MSCI acknowledged reforms from Otoritas Jasa Keuangan, the Indonesia Stock Exchange and PT Kustodian Sentral Efek Indonesia, including disclosure of shareholders above 1% ownership, more detailed investor classification data, a High Shareholding Concentration framework and a roadmap to raise the minimum free-float requirement to 15%. MSCI said it was still evaluating the consistency and reliability of those data sources and measures, and it said it would provide further clarity in its June 2026 Market Accessibility Review.

The stakes go beyond one rebalance. MSCI had already warned in January that Indonesia could be downgraded to frontier-market status, and the latest cuts hit stocks tied to major business groups, including names linked to Prajogo Pangestu and the Widjaja family’s Sinar Mas Group. FTSE Russell has also said it will delete Indonesian shares with high shareholding concentration effective June 22, suggesting the benchmark penalty for Indonesia may not end with MSCI’s move.

Know something we missed? Have a correction or additional information?

Submit a Tip