Goldman Sachs sees 2026 M&A driven by tech, capital and ambition

Goldman sees M&A humming without a classic boom: AI, private equity exits and flexible capital could keep 2026 near record levels.

Why the deal machine can keep running

Goldman Sachs is signaling that M&A does not need a euphoric bull market to stay busy. Its 2026 outlook points to technology, globalization and ambition as the forces that can keep boards talking, bankers pitching and deals moving even if the broader market never feels especially frothy.

That matters inside Goldman because deal flow drives more than headlines. It shapes pitch frequency, execution speed, bonus outcomes and the kind of complex work that builds careers in coverage, financing and advisory. When the market is open, the hours are still long, but the pipeline gets richer, the mandates get bigger and the exit opportunities for analysts and associates widen.

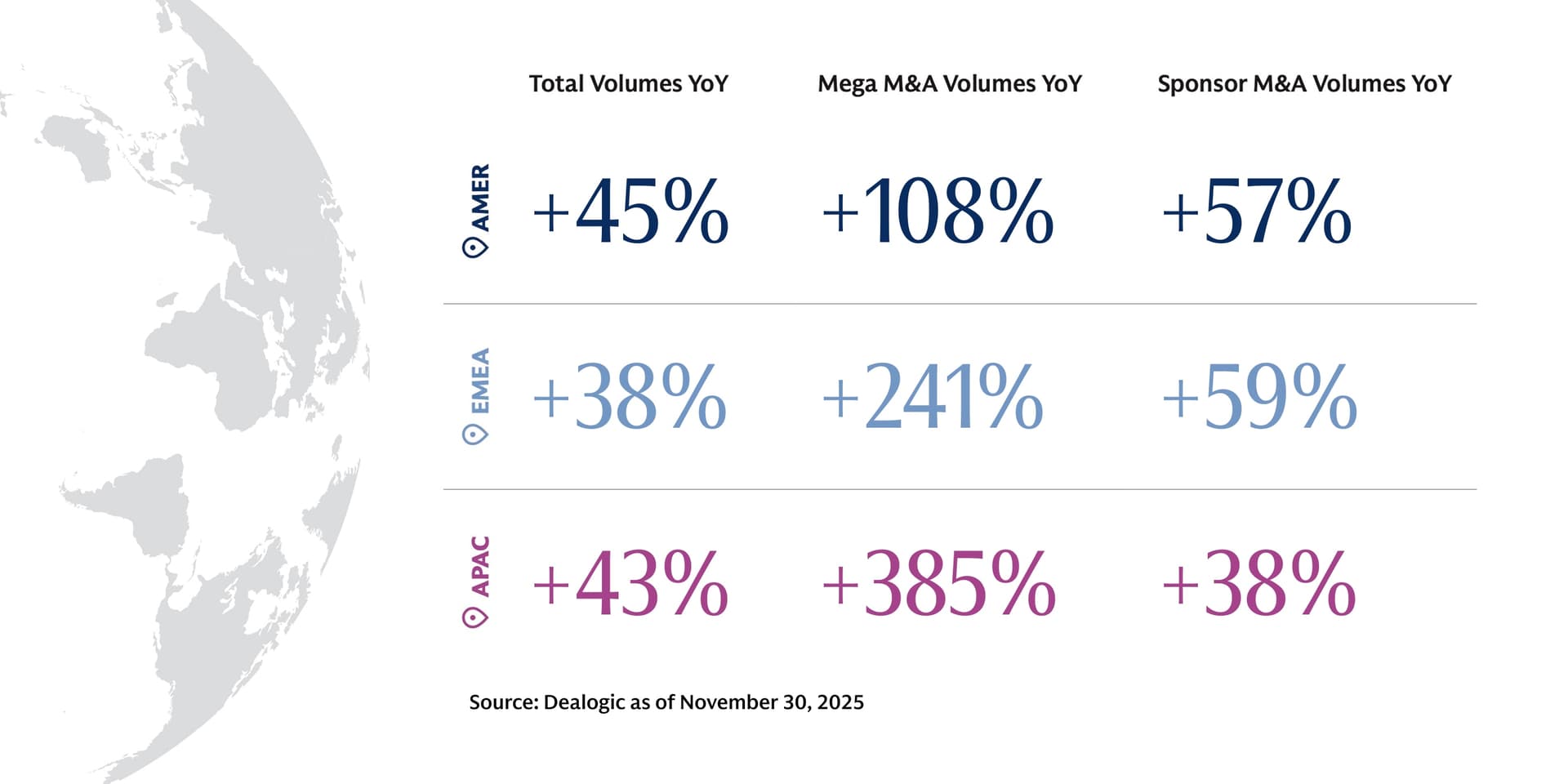

What Goldman thinks is changing

The bank’s message is that 2026 will be defined by strategic transformation, private markets and flexible capital solutions. In plain English, companies are not just buying growth anymore. They are using M&A to reshape portfolios, rework supply chains, reposition around AI and reset business models that no longer fit the market they are selling into.

Goldman’s broader 2026 outlook also points to a "sturdy" global growth backdrop, with its economists expecting global GDP growth of 2.8% in 2026. That does not sound like a manic boom, but it is enough macro support to make boards more willing to act, especially when capital is available and competitors are moving.

The firm’s own investment banking materials also frame AI as a driver of an "innovation supercycle" that is widening the aperture for strategic deals. That is an important shift for bankers. The conversation is no longer limited to traditional consolidation. It now includes who needs to buy capability fast, who needs to defend a franchise and who cannot afford to wait for internal investment alone.

The numbers behind the call

Goldman says the back half of 2025 created an exceptional M&A year that rivaled the record volumes of 2021. It points to open financing markets, strategic activity, elevated private-equity participation and abundant capital as the forces that kept dealmaking alive.

The scale matters. Bloomberg reported in September 2025 that Tim Ingrassia thought 2026 could be a record year, with global deal flow rising to as much as $3.9 trillion. That would clear the $3.6 trillion 2021 record cited by Dealogic, excluding SPACs. Reuters later reported that Goldman finance chief Denis Coleman said 2025 was on track to become the second-biggest year in history for announced M&A industrywide, which tells you the bank was not treating the market as a one-year spike.

Goldman reinforced that view again on April 24, 2026, when its Global Banking & Markets team said it expected "pure M&A volume" to reach $3.8 trillion in 2026. The bank said AI and increased selling of portfolio companies by private-equity firms were among the main drivers. That combination is telling: technology creates the strategic need, while private markets supply the assets and the exit pressure.

Where the mandates should hold up best

The mandates most likely to stay active are the ones tied to transformation, capital recycling and complexity. Private markets sit at the epicenter of that work, because sponsors are deploying capital at scale while also managing the timing and execution of exits. That creates a steady flow of processes, even when public markets are choppy.

For Goldman teams, the most resilient categories are likely to include:

- Strategic acquisitions, where companies buy capability rather than just size.

- Portfolio reshaping and carve-outs, where management teams prune businesses that no longer fit.

- Sponsor-led exits and recapitalizations, where private-equity owners look for liquidity without waiting for a perfect IPO window.

- Cross-border deals, where globalization creates both pressure and opportunity across New York and London coverage teams.

- Flexible-capital situations, where financing structures, minority investments or alternative funding sources make a transaction workable when a plain-vanilla cash bid would not.

The common thread is that these are not simple merger stories. They require valuation judgment, financing creativity, regulatory awareness and the ability to move quickly when the window opens.

What this means for bankers inside Goldman

For analysts and associates, a stronger M&A tape usually means more live work and less time spent polishing stale pitch books. It also means more sensitivity to the parts of the process that actually determine whether a mandate closes: diligence, financing certainty, sponsor dynamics, and whether the client is solving a real strategic problem.

That can be good for training and for exit opportunities, especially in a market where the best banking reps still translate directly into private equity, corporate development and strategy roles. It also comes with the familiar tradeoff: more live deals usually mean later nights, more models and a heavier pressure load on teams already built around 80 hour weeks.

For VPs and managing directors, the message is different but just as practical. If capital stays available and private markets keep churning, the real advantage goes to bankers who can connect strategy to execution, not just market sentiment to a pitch. The strongest coverage teams will be the ones that can explain why a buyer needs the asset now, why a sponsor wants out now and why a financing package can still work now.

Where the playbook matters most

Goldman’s outlook points most clearly toward sectors where technology is changing the business model, not just the product line. That includes tech itself, but also adjacent areas where AI adoption, supply-chain redesign or data intensity are forcing executives to buy capability instead of build it slowly.

It also matters in sponsor-heavy sectors, where private equity owns a deep bench of portfolio companies and needs routes to exit or reconfigure ownership. The more capital is sitting in private markets, the more pressure there is for bankers to find the next transaction, even if public sentiment never looks fully euphoric.

That is the core of Goldman’s 2026 view. M&A does not need a classic bull-market boom to stay active. It needs strategic urgency, money that can move and boards that believe standing still is the riskier choice.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?