Goldman Sachs sees AI boosting U.S. productivity and growth

Goldman says AI could help keep U.S. growth above 2%, giving Wall Street more room for deals, hiring confidence, and client risk-taking than skeptics expect.

Goldman Sachs Research is making a distinctly bullish macro argument: the U.S. economy’s potential growth rate looks to be above 2 percent over the next few years, and it could accelerate further in the next decade. For anyone inside Goldman, that matters because it changes the backdrop for everything from M&A and capital markets to bonus pools, staffing confidence, and the durability of client demand.

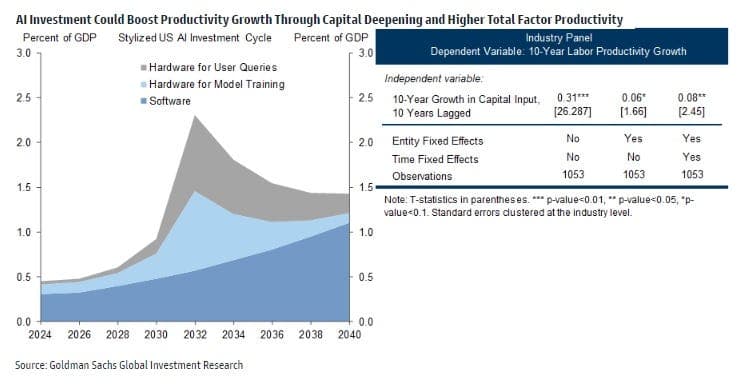

The key wrinkle is that this growth story is not being powered by a surge in labor supply. Goldman says labor-force growth is likely to add only about 0.3 percentage point to potential GDP in the coming years. That leaves productivity as the main engine, which is why the firm sees artificial intelligence not just as a valuation theme, but as a force that could lift output per worker and keep the economy expanding even as headcount growth slows.

Why the 2 percent-plus backdrop matters on the desk

For bankers, a higher potential growth rate is not a trading signal so much as a pipeline signal. If the economy can grow faster without immediately colliding with the same capacity limits that worried investors in earlier cycles, companies have more room to make long-term plans, issue debt, pursue acquisitions, and spend on expansion rather than simply defending margins. That creates a healthier setting for transaction activity over time, even if the path is still uneven quarter to quarter.

The same logic matters for total compensation and staffing dynamics inside Goldman. When corporate earnings have more room to grow, deal teams tend to see more confidence from clients, more willingness to fund strategic moves, and less paralysis around big-ticket decisions. That does not guarantee a banner year in every division, but it can keep the franchise from relying too heavily on a single burst of market volatility or one hot product cycle.

AI as a productivity story, not just a market story

Goldman’s framing is especially useful because it pushes AI beyond the usual conversation about stock multiples and toward the deeper question of how the economy actually grows. If workforce expansion is slowing, the firm argues, then companies will lean harder on software, automation, and process redesign. That is the part that should matter to Goldman employees across banking, investing, and wealth management, because it opens up advisory, financing, and investment themes that are broader than any one sector’s share-price rerating.

That shift also changes how internal teams may think about where opportunity shows up. In banking, it means clients may keep asking for help funding AI-related capital spending, reorganizing operations, and buying technology rather than only cutting costs. In investing, it means the real question is whether productivity gains can spread beyond the obvious leaders and support a wider set of earnings winners.

The labor-force test behind the optimism

The bullish case is not that the U.S. has escaped cyclical risk. Goldman is explicit that a higher potential growth rate does not remove the possibility of slower patches, tighter financial conditions, or sector-specific stress. The case is narrower and more interesting: if labor-force growth contributes only about 0.3 percentage point to potential GDP, then the economy is being asked to do more with less labor growth, and productivity has to carry the load.

That is where the thesis becomes consequential for a workplace audience. If productivity rises enough, firms can sustain hiring in selective areas, support stronger earnings, and avoid the kind of capacity crunch that can freeze decision-making. If it does not, the AI narrative starts to look more like a concentration trade, with gains confined to a small group of firms while the broader economy still feels stuck.

What this means for deal flow and hiring confidence

A more productive economy can support healthier nominal growth, and that tends to matter for both corporate behavior and Wall Street staffing. Stronger nominal growth usually means companies have more confidence to invest, refinance, acquire, or raise capital. It also tends to help the kind of client conversations that keep junior bankers busy and give managing directors more conviction when they approve headcount or defend a hiring plan.

That is why this macro view is more than an abstract economics discussion. If clients believe growth is durable, they are less likely to sit on the sidelines and more likely to ask for advice on M&A, equity, debt, and strategic repositioning. For Goldman employees, that can translate into a steadier runway for work, stronger exit opportunities, and a compensation environment that is less hostage to one-off market swings.

How wealth management should read the same signal

For wealth managers, the issue is not just whether GDP can stay above 2 percent. It is whether the gains from AI will be broad enough to support risk assets, or whether they will be concentrated in a handful of companies and leave the rest of the market lagging. That distinction matters when clients are deciding how much risk to take, how to position for the next cycle, and whether the current growth story is durable or merely narrow.

Goldman’s view gives advisers a language for that conversation. AI is being cast as one of the key reasons productivity can improve, not simply as a theme that inflates the value of a few winners. That makes the message more persuasive internally as well: the same forces that are lifting a few balance sheets today could end up broadening earnings power across industries tomorrow.

The internal takeaway for Goldman employees

The most practical read is that slower labor growth does not automatically mean a weaker economy. If productivity keeps improving, the machine can keep running, and the macro backdrop may stay constructive for longer than many expect. That is the kind of environment where banking teams, investment teams, and advisers can all find reasons to stay busy.

For Goldman, the real implication is strategic: AI is not only changing which companies spend, borrow, or buy. It is also changing the assumptions behind how long the cycle can stay favorable, which is exactly the kind of shift that affects compensation, hiring confidence, and the tempo of the entire franchise.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?