Goldman Sachs sees resilient growth, AI momentum, and oil-driven risks ahead

A $7.6 trillion AI build-out and Brent near $90 are reshaping Goldman client calls, from macro hedging to equity positioning.

Goldman Sachs Asset Management’s May Market Pulse gives Goldman teams a tighter client script: Middle East risk is easing, global growth has stayed resilient, and the market is still being pulled between oil volatility and AI-led earnings momentum. The useful takeaway for anyone speaking to clients is not just that the backdrop is complicated, but that three questions now dominate the conversation: how long oil stays elevated, whether AI spending keeps broadening, and how much resilience remains in the US and global economy.

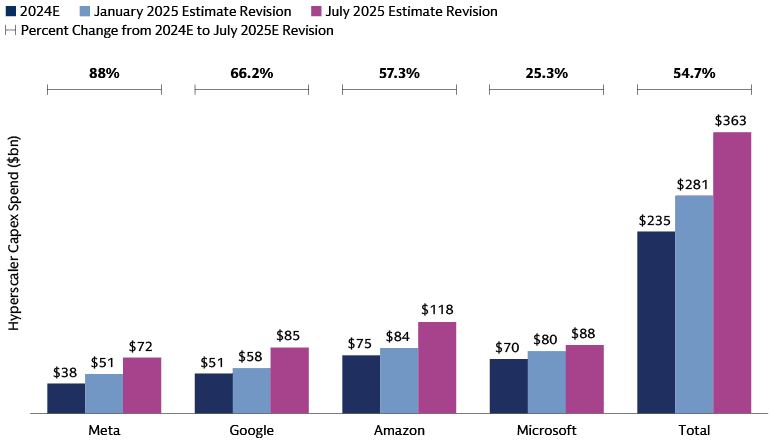

The share hook is in the numbers. Goldman Sachs Research now estimates roughly $7.6 trillion of aggregate AI capex between 2026 and 2031 across compute, data centers, and power, while Wall Street analysts’ consensus for hyperscaler AI capital spending in 2026 has climbed to $527 billion from $465 billion at the start of the third-quarter earnings season. That scale is why this is no longer just a tech trade. It is a capital-allocation story that reaches into power markets, industrials, financing needs, and the earnings outlook that portfolio managers keep pressing Goldman for.

Middle East risk: oil is still the main transmission channel

Goldman’s May 4, 2026 pulse says conflict in the Middle East is moving toward resolution, but the market impact has not disappeared. The bank’s March brief made the key point plainly: oil is the primary transmission channel from the conflict into markets, and sustained price increases could heighten volatility and pressure crowded consensus trades. That framing matters for client conversations because it turns a geopolitical story into a practical market map, with oil, inflation, consumer demand, and positioning all tied together.

The latest commodity view is more specific. Goldman’s April 26 oil forecast upgrade reportedly lifted Q4 2026 Brent to $90 and WTI to $83, and the Market Pulse says Brent around $90 looks more likely if flows normalize in June. If disruption lasts longer, the upside risk gets larger. For Goldman employees on client calls, that means the message should be disciplined: oil is not just a headline risk, it is the channel that can still unsettle inflation expectations, margins, and crowded trades.

The US is somewhat insulated because it remains a net energy exporter, but even that resilience has limits. Goldman warns that higher-for-longer oil prices could weigh on consumer demand in the coming months. That is the real day-to-day impact for clients and households alike: fuel costs, shipping costs, and input prices can bleed into margins long before a macro dashboard shows stress. Europe is the more vulnerable region, because energy disruption is more painful for the euro area than for the US, which makes regional positioning a bigger part of the conversation than simple risk-on or risk-off language.

AI spending: keep the discussion on capex, earnings, and power

AI remains the cleanest growth narrative in Goldman’s 2026 outlook. Goldman Sachs Asset Management’s November 18, 2025 outlook was titled Seeking Catalysts Amid Complexity, and that phrase still captures the firm’s message: AI-powered innovation is sustaining investor optimism even as trade, fiscal, and geopolitical risks complicate the backdrop. The market pulse reinforces that view by treating AI capital spending as a durable engine, not a narrow theme that only matters to a handful of large-cap technology names.

That is why the $7.6 trillion estimate matters so much. It suggests the build-out is big enough to affect macro assumptions, not just stock selection. For client-facing teams, the practical implication is to move the discussion from abstract enthusiasm to concrete winners and bottlenecks: who captures the spend, who finances it, who supplies the power, and how long earnings momentum can keep stretching beyond the obvious hyperscalers.

Goldman’s message also helps explain why emerging market equities stand out in the pulse. The bank says they are supported by strong AI-driven earnings momentum, which is a useful reminder that the AI trade is not confined to US mega-cap names. For bankers, traders, and asset managers, this creates a more nuanced talking point: AI is now part of the broader earnings machine, and clients want to know where that momentum is broadening rather than whether the theme still exists at all.

Growth and rates: resilient enough for risk, soft enough for cuts

Goldman’s view of growth is constructive but not exuberant. In the May pulse, researchers see 2026 US growth at 2.3%, core inflation ending the year at 2.5%, and room for the Federal Reserve to cut later in the year. That is a narrower, more tactical message than the broader Goldman macro outlook, which still points to sturdy global growth of 2.8% in 2026 and 50 basis points of Fed cuts.

For Goldman employees, the practical read-through is that clients are likely to keep asking how to reconcile sticky oil with eventual policy easing. The answer is not to choose one narrative over the other. It is to explain that inflation pressure from energy can delay the path, but it does not necessarily erase the case for cuts later in the year if growth stays resilient and price pressures fade. That framing matters for rates positioning, duration conversations, and the way teams talk about rate-sensitive sectors.

The broad market tone is still constructive because equity markets can focus on earnings and longer-term growth if the Middle East backdrop keeps improving. That gives Goldman a useful client-ready distinction: the market is not pricing a collapse, it is balancing resilient growth against the risk that energy shocks keep filtering into consumer behavior and inflation.

What Goldman teams should emphasize in client conversations

Across Goldman Sachs Asset Management, Goldman Sachs Research and the Goldman Sachs Global Institute, the 2026 message has stayed consistent: AI-powered innovation, central-bank policy, geopolitical shifts and a more complex investment environment are all colliding at once. The Market Pulse translates that into something frontline teams can actually use.

- Lead with oil when clients ask about Middle East risk, because that is still the cleanest market transmission channel.

- Keep the AI conversation on capital spending, power demand and earnings breadth, not just on the largest technology names.

- Draw a clear line between US resilience and Europe’s greater exposure to energy shocks.

- Use the 2.3% US growth view, 2.5% core inflation estimate and room for Fed cuts to frame rates discussions without overselling certainty.

- Treat emerging market equities as part of the AI earnings story, not as a separate, unrelated allocation idea.

That is the practical value of the pulse for Goldman employees. It trims the market noise and leaves a usable playbook for the next round of client calls: watch oil flows, keep pressure on the AI numbers, and explain why a resilient economy can still coexist with volatility in energy, inflation and rates.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip