Goldman Sachs sells Petershill stake in ArcLight Capital Partners

Petershill sold its ArcLight stake at a premium, lifting realized proceeds to about $3.6 billion and reinforcing Goldman’s GP-stakes exit model.

Goldman Sachs Alternatives has turned another minority stake into cash at a premium, selling Petershill’s non-control interest in ArcLight Capital Partners and adding to a monetization streak that now matters as much as the marks on the book.

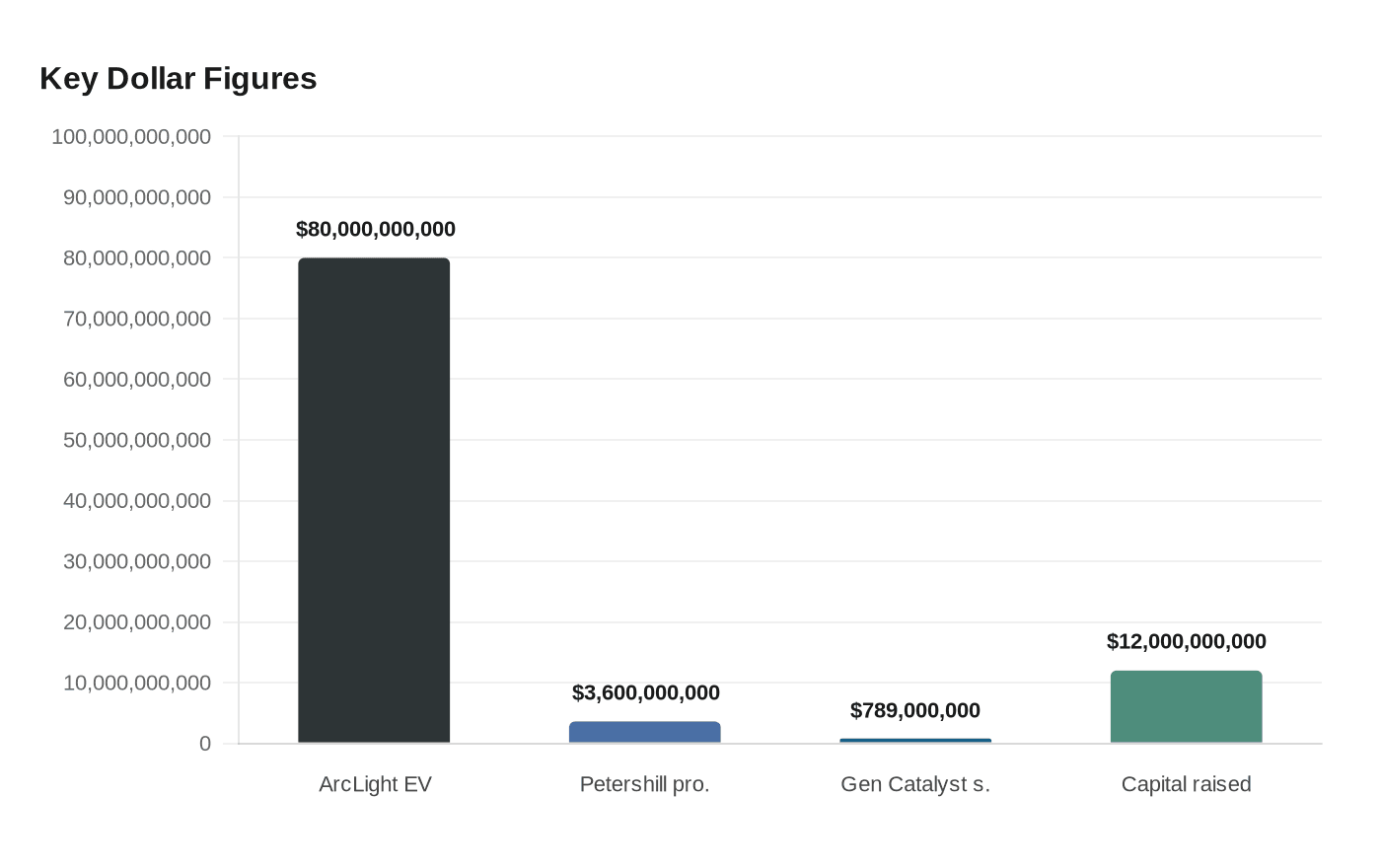

Goldman said the ArcLight realization was sold above Petershill’s net asset value and helped bring aggregate realized proceeds to about $3.6 billion across financing activity and nine realizations since the start of 2024. The deal followed the full realization of Arctos Partners in May 2026, extending a run that has shown Petershill can do more than warehouse stakes and wait for paper gains to show up. It can exit, lock in returns and recycle capital.

That is the signal employees and clients should care about. In an alternatives business built around GP stakes, value is proved not only when a firm takes a position, but when it sells at a premium and keeps the control relationships intact. Goldman’s GP-stakes strategy dates to 2007, and the platform says it has partnered with more than 49 firms, sourced more than 800 opportunities and raised more than $12 billion since inception. The ArcLight sale suggests that discipline around manager selection, entry timing and exit timing is translating into realized economics.

ArcLight gives the trade real weight. The firm was founded in 2001 and says it has owned, controlled or operated more than 65 gigawatts of assets and about 47,000 miles of electric and gas transmission and storage infrastructure, representing roughly $80 billion of enterprise value. Founder and managing partner Daniel Revers has built the platform around electrification infrastructure that sits at the center of long-cycle capital spending, including the power and transmission build-out tied to the digital economy.

For Goldman bankers covering power, utilities, transmission, storage and electrification, the sale reinforces a broader theme: infrastructure tied to AI and electrification is becoming one of the few places where physical assets, long-duration contracts and private-market ownership still intersect cleanly. For Goldman itself, the comparison with the January 2025 sale of the majority of its stake in General Catalyst for $789 million is hard to miss. Both exits were priced above net asset value, and both showed that minority GP stakes can be monetized without disturbing the operating firms behind them.

Petershill’s exit activity has also supported special dividends and other capital returns in 2024 and 2025, making monetization a core part of the platform’s economics, not an afterthought. The ArcLight sale pushes that logic further: in Goldman’s alternatives business, the win is no longer just owning the stake. It is proving the stake can be sold well.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip