Goldman Sachs warns AI is reshaping valuation math for U.S. stocks

Goldman says profits more than 10 years out drive 75% of the S&P 500’s value, and AI could punish the priciest software names first.

Goldman Sachs is warning clients that AI is changing the valuation math behind U.S. stocks, and the biggest pressure point is the same corner of the market that has long looked safest to growth investors: software and other long-duration businesses. The bank says profits expected more than 10 years out now make up about 75% of the S&P 500’s equity value, close to a 25-year high, which leaves prices highly sensitive to even small changes in long-term growth assumptions.

That sensitivity is extreme. Goldman estimates that a 1 percentage point drop in assumed long-term growth would cut the combined enterprise value of S&P 500 companies by about 15%, with high-growth stocks taking a much harder hit than low-growth names. For Goldman employees covering technology, that is not an abstract model. It changes how clients talk about durability, not just adoption. The question is no longer whether a company has an AI strategy, but whether AI strengthens pricing power, keeps customers locked in, and protects cash flows far enough into the future to justify a premium multiple.

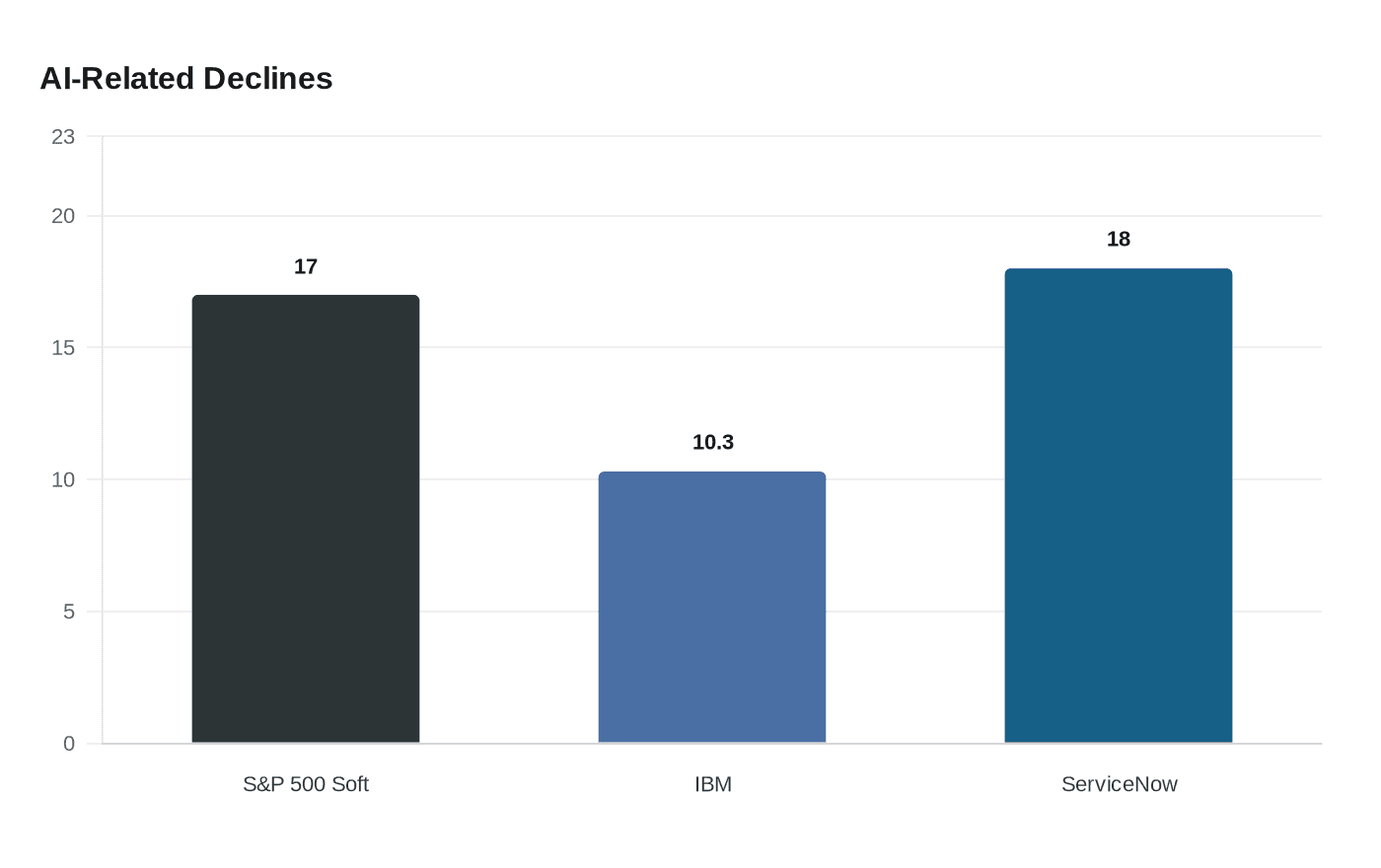

The market has already started to answer. The S&P 500 software and services index is down about 17% so far this year, as investors have grown more worried that new AI tools could pressure future revenue growth and margins for software providers. Goldman’s own software research found that at a recent peak, valuations implied medium-term 2028 revenue growth of 15% to 20%, while current lower multiples imply just 5% to 10% growth. In other words, the market has moved from pricing software like a category with durable expansion to pricing it like a business that has to prove it can still grow fast in an AI-saturated world.

That re-rating has been reinforced by earnings. IBM shares fell 10.3% on April 23 after slower first-quarter revenue growth, with weakness in the software business, including Red Hat, under pressure. ServiceNow dropped about 18% the same day, its worst session on record, after results revived broader AI-disruption fears across the sector.

Goldman is not arguing that software is finished. The firm has also said AI could expand the market by improving productivity and lowering the cost of code, while projecting cloud sales could reach $2 trillion by 2030 and the application software market could grow to $780 billion by then. But for bankers, traders and portfolio managers inside Goldman, the message is clear: AI is not just a theme to sell. It is becoming a filter for which business models deserve the highest multiples, the richest deals and the longest runway.

Know something we missed? Have a correction or additional information?

Submit a Tip