Goldman Sachs Warns Stock Correction Poses Greatest Near-Term Risk to GDP

A 10% equity drop could shave 0.5 points off U.S. GDP growth, Goldman's Pierfrancesco Mei warned, calling stock correction the top near-term economic risk.

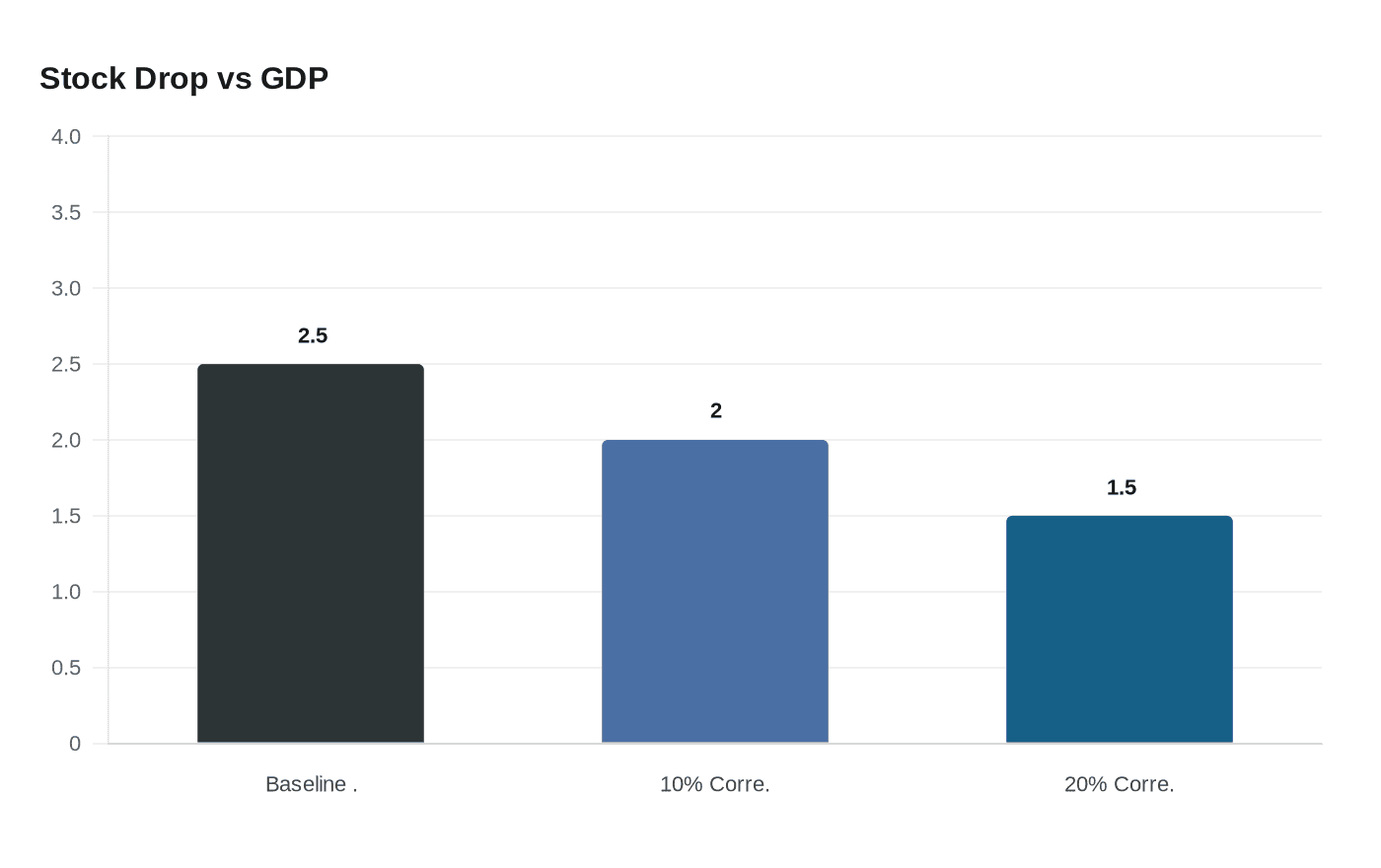

A sharp stock market correction is the single greatest near-term threat to U.S. economic growth in 2026, according to a 16-page Goldman Sachs note by U.S. economist Pierfrancesco Mei that landed Monday. The warning is precise: a sustained 10% equity decline through the second quarter of 2026 could subtract 0.5 percentage points from GDP growth, while a 20% drawdown could leave Goldman's baseline estimate short by nearly a full percentage point.

"Our analysis suggests that a sharp equity correction represents the most significant near-term risk," Mei wrote. The mechanism is the wealth effect. Higher-income households hold the bulk of U.S. equities, and a drop in asset values curbs their willingness to spend. That matters enormously because, according to Moody's Analytics data cited in the note, the top 10% of earners drive nearly half of all consumer spending, and consumer spending itself accounts for roughly two-thirds of the U.S. economy. As Mei put it: "A stock market correction would turn the boost from wealth effects we expect into a drag on consumption in the second half of 2026."

Goldman's baseline is not pessimistic. Mei projects Q4/Q4 GDP growth of 2.5% for 2026, above the 2.1% market consensus, supported by fiscal stimulus, Fed rate cuts and easing tariff headwinds. The firm also forecasts a 12% total return for the S&P 500 this year on 12% earnings-per-share growth. The correction warning is a conditional risk, not Goldman's central scenario.

Still, the conditions for a correction are not hypothetical. The S&P 500's forward price-to-earnings ratio sits near 22x, close to 2021 peaks, meaning elevated multiples could amplify any earnings disappointment. A separate Goldman strategy team led by Peter Oppenheimer flagged that geopolitical uncertainty and anxiety about AI capital expenditure and disruption were combining into "a significant headwind for risk assets to absorb in the short term." The Oppenheimer team also noted that the recent broadening of global equity gains has left all major regions trading above their own longer-term valuation histories, while a rotation from growth into value stocks has made index levels more sensitive to macro shocks such as energy supply disruptions.

Historical context adds weight to the concern. According to data from Aptus Capital Advisors cited in the Mei note, midterm election years have historically averaged intra-year S&P declines of 19% at their trough.

Goldman does not expect the worst. Oppenheimer's team wrote that "the depth and extent of any correction are likely to be limited, in our view, with relatively low risk that it morphs into a bear market." A 20% drawdown would technically qualify as a bear market by Wall Street convention, and Goldman's modeling suggests that scenario, particularly if compounded by AI-related labor disruptions, could create obstacles significant enough to override the firm's constructive baseline entirely.

The 0.5-percentage-point hit from a moderate correction may sound manageable against a 2.5% growth forecast. But it would knock Goldman's own projection down to 2.0%, essentially matching consensus, and erase the policy-driven cushion Mei identified as the year's primary growth engine.

Know something we missed? Have a correction or additional information?

Submit a Tip