Goldman Sachs warns US consumers face weaker spending amid oil shock

Goldman sees a tougher few months for US shoppers as gasoline costs surge, a warning that could hit lending, client risk appetite and bonus pools.

Goldman Sachs is seeing a split screen in US consumer data: headline spending has not collapsed, but the bank says the next few months look weaker as fuel costs bite harder and confidence sours. Ronnie Walker said consumer spending, which had looked solid earlier this year, “has quickly become more challenging,” and Goldman expects weak real consumption growth over the coming months.

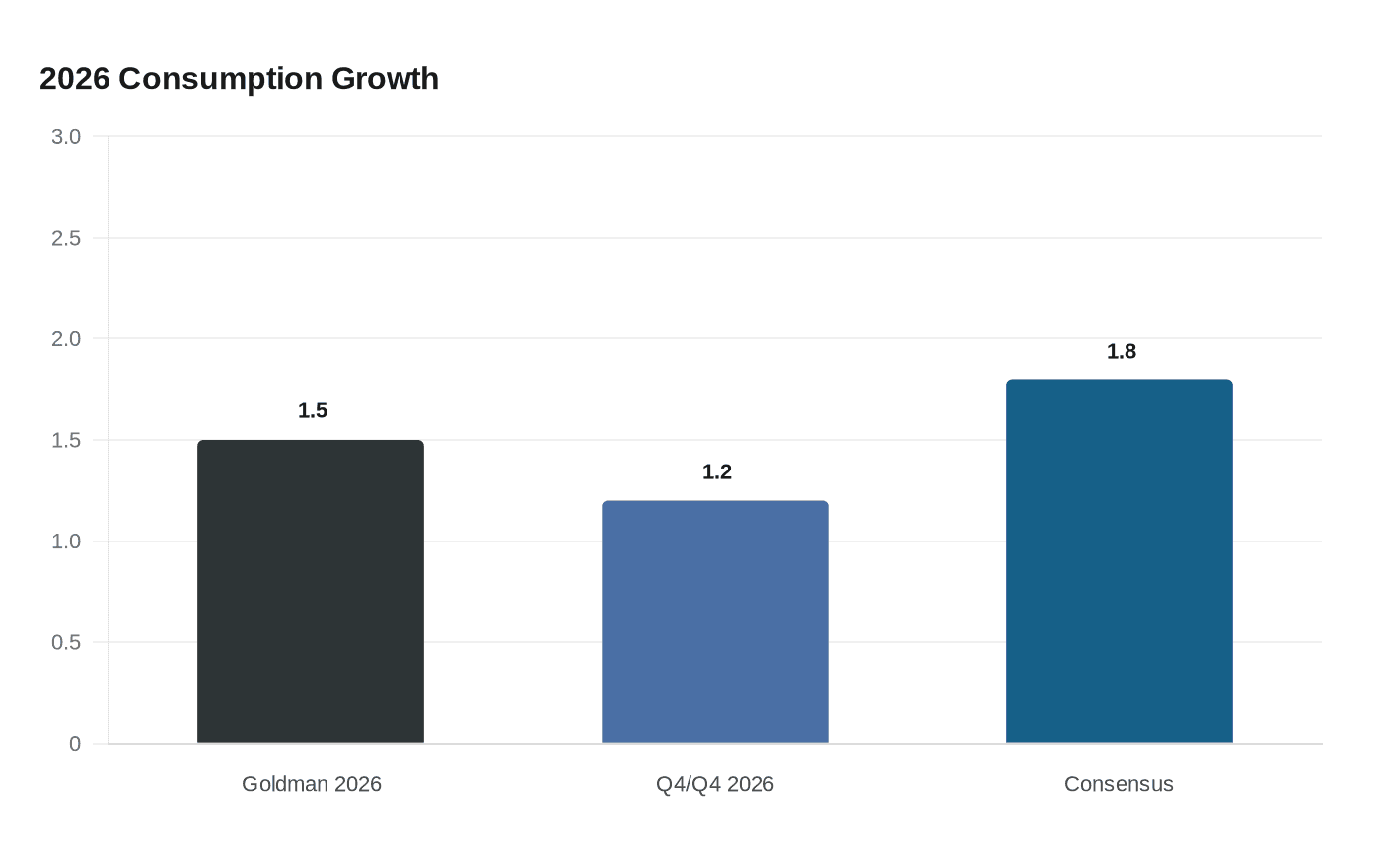

The pressure point is gasoline. Goldman said prices have risen by nearly 40% since the Iran conflict began, creating about a $140 billion annualized drag on household incomes at current levels. Even if Brent crude drops back to $80 a barrel by year-end, Goldman still sees a roughly $70 billion hit to 2026 income. The bank’s economists, including Alec Phillips and Joseph Briggs, now forecast 1.5% consumption growth for 2026, or 1.2% on a fourth-quarter-over-fourth-quarter basis, below the 1.8% consensus estimate.

That matters inside Goldman because the pain is uneven. Households in the lowest income quintile spend roughly four times as much on gasoline as a share of after-tax income as households in the top quintile, Goldman said, and that same group faces tepid job growth, cuts to Medicaid and SNAP benefits, and greater exposure to higher fuel costs. Investors are already watching that weakness seep into earnings expectations for McDonald’s, Dollar General and Dollar Tree, the kinds of names that often tell the market how lower-income shoppers are holding up.

The bank also sees only a limited offset from tax season. Tax refunds are running 17% higher than last year and are projected to be up about $50 billion by the end of May, but tax payments are expected to come in $40 billion to $55 billion higher than last year. In other words, the boost is likely to be swallowed by the fuel shock rather than power a fresh spending wave.

Goldman Sachs Research’s March Consumer Dashboard, published April 10, already pointed to a softer backdrop: real retail sales fell at a 1.3% three-month annualized rate through February, personal income slipped 0.1% in February, the saving rate rose to 4.5% in January and is expected to climb further, and 90-plus-day credit card and subprime auto delinquencies remain above pre-pandemic levels. The University of Michigan consumer sentiment index fell to 47.6 in the April preliminary reading, a record low if it holds. That is the kind of signal bankers, consumer lenders and wealth advisers will be watching next, because a weaker shopper can quickly become a weaker borrower, a more cautious client and, eventually, a softer revenue line. David Solomon has said recession odds are still relatively low, around 20%, but Goldman’s message is that consumer strain is already moving from a macro risk to a business risk.

Know something we missed? Have a correction or additional information?

Submit a Tip