Goldman says AI rally looks stretched, but not a dot-com repeat

AI stocks have added $27 trillion since late 2022, but Goldman says profits, balance sheets and the current account still keep this from looking like a dot-com rerun.

Goldman Sachs Research’s July 10 valuation note gave employees a clean line for AI client calls: the rally looks stretched, but it does not read like a dot-com rerun. AI-related companies have added roughly $27 trillion in market value since late 2022, and US tech investment as a share of GDP has already moved past its 1990s peak, yet Goldman said corporate profits have climbed to new highs, balance sheets remain stable and the current account deficit has narrowed.

The firm’s own market framing was just as measured. As of April 24, Goldman said the S&P 500 traded at about 21 times forward earnings, close to its five-year average, and kept a year-end target of 7,600, implying 6% upside on expected 12% earnings growth in 2026 and 10% in 2027. On the spending side, Goldman lifted its 2026 hyperscaler AI capex estimate to $527 billion from $465 billion at the start of the prior earnings season, but said investment would need to reach about $700 billion to match the peak of the late-1990s telecom cycle.

That is the messaging gap Goldman bankers, sales teams and research analysts have to manage. The June 2 note by Jim Covello said the economics of AI looked more questionable than two years earlier because enterprise buyers, model makers and hyperscalers had not yet shown returns. A May 11 research note said most enterprises were still not generating returns from AI spending. At the same time, a July 9 note said enterprise deployment was accelerating and the top 5 percent of companies were consuming three times as many tokens as the median company, which means usage is real even if monetization is still uneven.

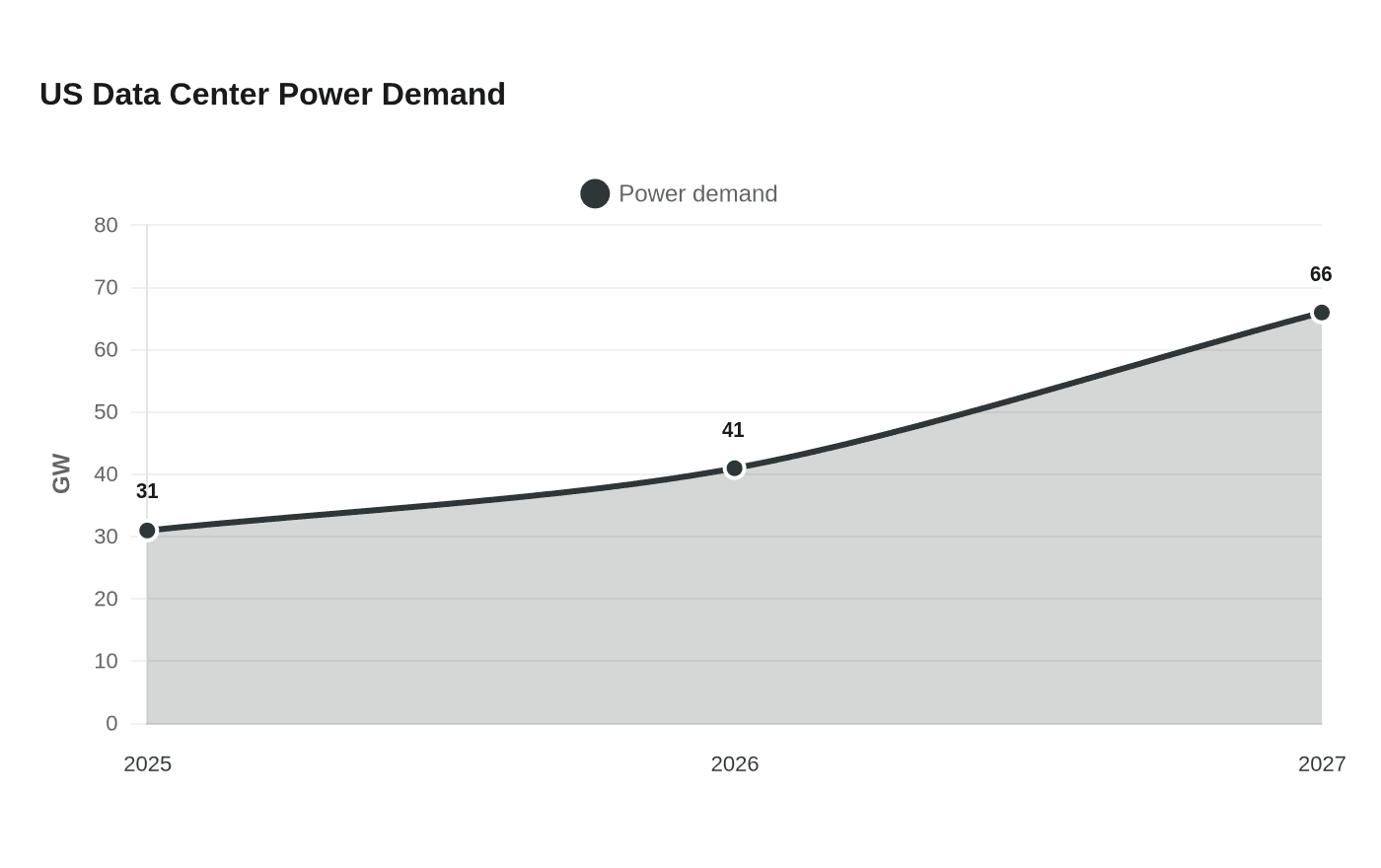

For traders, that mix argues for concentration risk and multiple expansion to stay front of mind. For ECM and bankers covering AI infrastructure vendors, the harder question is not whether capital will keep flowing, but who captures the profit pool when spending keeps rising. Goldman’s May 20 power-demand forecast pointed to that shift in hard numbers, with US data-center power demand rising from 31 GW in 2025 to 41 GW in 2026 and 66 GW in 2027. Goldman has already said late-2025 bubble fears were real but not yet at historical-bubble levels, and in September 2024 it said tech valuations were high but not necessarily irrational. That leaves financing, advisory and equity work alive even as clients demand more proof that AI profits can catch up with the capital being spent.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?