Goldman says hedge funds are taking profits on semiconductors, not fleeing AI

Goldman says hedge funds are locking in gains on semis while staying in AI, forcing traders and researchers to thread the needle on crowding risk.

Goldman Sachs is telling clients that the semiconductor pullback is a position-sizing exercise, not an AI retreat. For the firm’s prime brokerage, sales and research teams, that distinction matters because semis remain one of the cleanest ways investors express exposure to AI infrastructure.

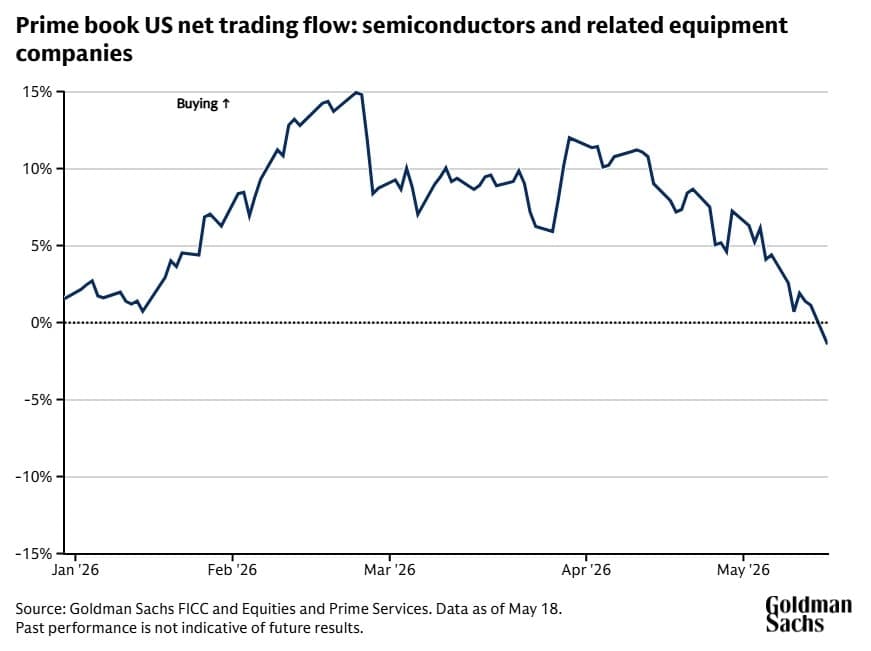

In a May 22 note, Goldman said hedge fund clients had been taking profits on semiconductor and equipment makers even as technology shares pushed to record highs. Semiconductors and related equipment were the most net-sold US subsector over the prior month, and they were modestly net sold year to date, even though they still ranked among the most net-bought US subsectors cumulatively since the start of last year. Vincent Lin, co-head of Prime Insights and Analytics at Goldman Sachs, said funds were selling into a powerful rally, but the firm read that as risk management and portfolio rebalancing rather than a regime shift away from AI.

That nuance shapes the workaday conversations on the desk. Prime services teams now have to explain crowded positioning, entry points and hedging without sounding like they are calling the top. Goldman said hedge funds also increased short wagers on US equity macro products, index funds and exchange-traded funds used to hedge broader market risk, with those short positions at a 10-year high. At the same time, overall hedge fund exposure to US artificial intelligence stocks in Goldman’s TMT AI basket remained near record highs, suggesting managers are trimming winners while staying attached to the trade.

The leverage data points to a market that is busy, not euphoric. Goldman said gross leverage climbed to a fresh five-year high, while net leverage sat in the 58th percentile on a three-year lookback. Hedge funds were also hedging beta exposure again because of higher inflation prints and rising bond yields. For Goldman’s traders, that means more work in hedges and index products; for sales teams, it means more client questions about how much of the AI move is still about fundamentals and how much is about crowded momentum.

Goldman’s own research has kept the AI case constructive. On May 20, Goldman Research said agentic AI could drive a 24-fold increase in token consumption to 120 quadrillion tokens per month between 2026 and 2030, while the firm also said chipmakers may face a shortage for the next 12 to 18 months as they build new plants. Shawn Tuteja said on May 13 that semis were up about 70% from their March 30 lows, and Goldman said on April 10 that global technology had one of its weakest stretches of relative returns in the last 50 years versus global stocks. Against that backdrop, Goldman’s message is clear: the AI trade still has legs, but the easy-money phase is giving way to more disciplined positioning.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?