NAHB guide spotlights financing barriers to missing middle housing

Financing, not zoning, is keeping many duplex and fourplex projects from becoming actual orders. That leaves Home Depot stores waiting on jobs that never make it past the lender.

An April 2026 Urban Institute analysis found construction financing for smaller, scattered-site homes remains a fundamental bottleneck even after zoning and land-use reforms open the door. NAHB’s new financing guide identifies the same problem as one of the biggest barriers to missing middle housing, the house-scale product that sits between detached single-family homes and large apartment buildings. For Home Depot associates and Pro teams, stalled duplexes, townhouses and other small infill jobs never turn into repeat pulls for lumber, drywall, millwork, electrical, plumbing, paint and installation work.

What counts as missing middle

NAHB defines missing middle housing as the kind of modest-density product that blends into existing neighborhoods instead of reshaping them all at once. The list includes duplexes, triplexes, fourplexes, courtyard and cottage court communities, and townhouses. NAHB also describes this housing as a way to widen price points and create “gentle density” in communities that already have streets, utilities and customers in place.

These are not giant tower jobs with one massive material order and a long lead time. They are smaller, repeatable projects that can feed steady demand into Pro desks and store replenishment if they actually get financed and started. When the funding clears, these homes need the same categories Home Depot sells every day: framing lumber, sheet goods, drywall, trim, cabinets, rough plumbing, electrical gear, paint, and installation support.

Why the money stops the build

Large builders that rely on capital markets are poorly suited to this niche, while community and regional bank construction lending has continued to pull back, the Urban Institute found.

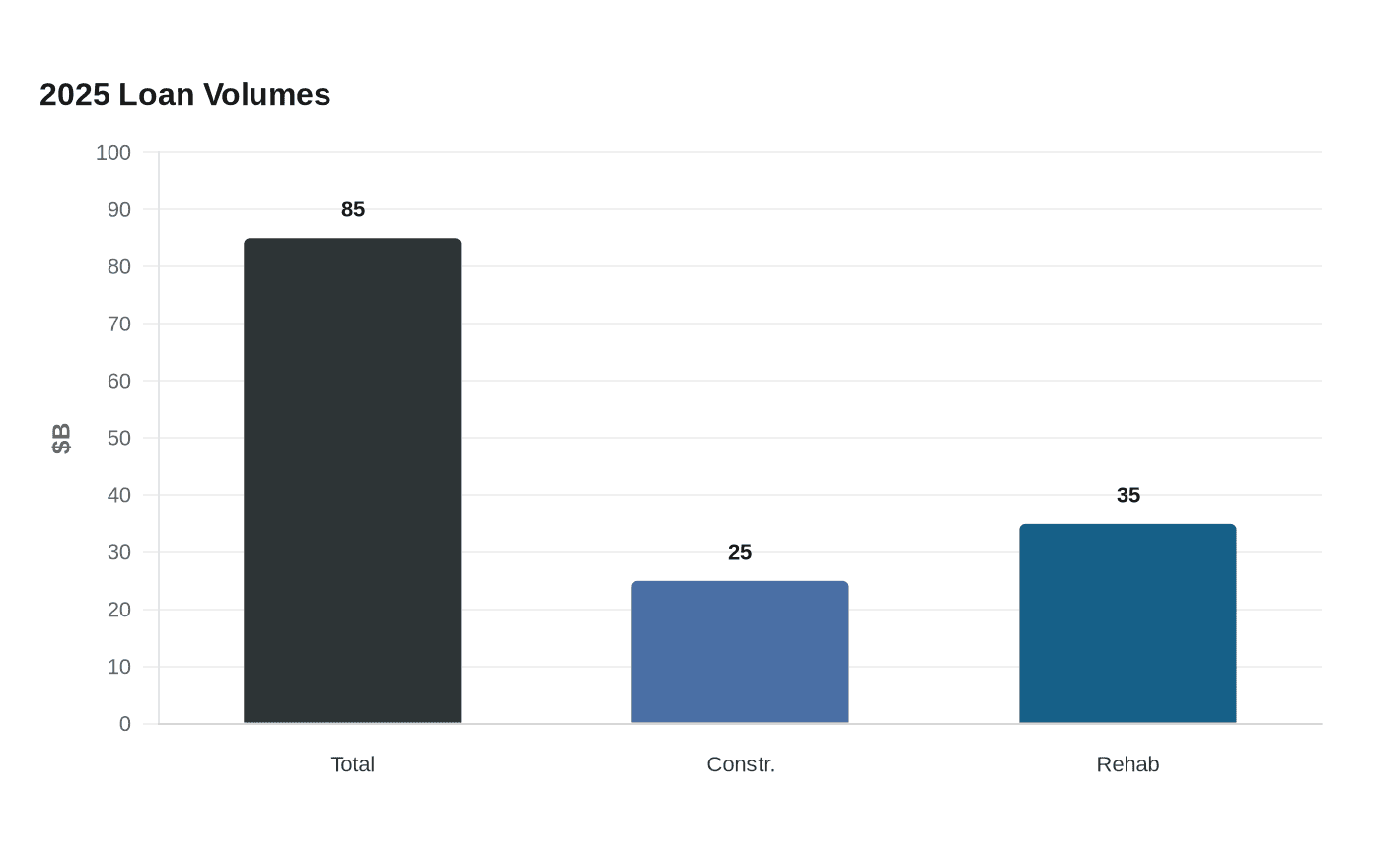

Urban Institute identified residential transition lending as the main workaround. In 2025, more than $85 billion in those loans were originated, including more than $25 billion for ground-up construction and more than $35 billion for rehabilitation. That financing is supporting tens of thousands of new homes each year, often through small local builders who can move on projects that do not fit the traditional big-developer model.

The demand curve for missing middle housing is not blocked only by permits or neighborhood politics. It is blocked earlier, at the point where a builder has to prove the project can be funded, insured and carried long enough to become a real job order.

Which projects look promising but stall

The projects that look easiest to add on paper are often the ones that struggle hardest to pencil out. A June 2024 Terner Center analysis found that many missing middle housing types were not financially feasible in case studies across four California markets. The hardest product to build was the four-unit ownership building, even though it sits squarely in the middle of the missing middle spectrum.

Terner’s analysis also points to the local rules that can sink a project before the first truck arrives. Lot-size regulations, parking requirements and insurance requirements all raised the cost stack enough to push some projects out of reach. That helps explain why a duplex, a small fourplex or a courtyard-style infill project can look like a sensible neighborhood addition and still never become a material order.

- Duplexes and triplexes can fit the market need for smaller ownership or rental options, but they still need construction loans that are comfortable with smaller balance sheets and scattered sites.

- Fourplexes look efficient on a drawing board, yet Terner found four-unit ownership buildings were the hardest missing-middle form to build.

- Courtyard and cottage court communities offer the “gentle density” NAHB favors, but they still face the same financing tests as any other small project.

- Townhouses often appear straightforward, but the funding has to survive land costs, local requirements and the builder’s limited scale.

The wider housing shortage keeps the pressure on

NAHB estimated in February 2026 that about 1.2 million additional housing units were needed to close the gap and restore historical vacancy norms. The National Low Income Housing Coalition estimated in March 2026 that the country faced a shortage of 7.2 million homes affordable and available to extremely low-income renters.

Harvard’s Joint Center for Housing Studies found household growth slowed to 1.1 million in 2025, existing-home sales were at three-decade lows, and affordability remained under pressure. At the same time, rents fell and multifamily vacancies rose, showing a housing market that is still strained even where some segments have softened.

Harvard’s Graduate School of Design has pointed to Boston’s triple-deckers as a historical precedent. These housing forms were once common and often built by local owner-operators.

What this means for Home Depot stores

For Home Depot, the sales signal is not just whether a city has upzoned a corridor or allowed accessory units. The real signal is whether a project gets financed far enough to place orders with a Pro desk and keep coming back as the job moves from foundation to finish. Home Depot’s Pro business serves contractors with more than 3 million SKUs, more than 2,000 store locations, dedicated support, project tools, volume pricing, financial services and job-site delivery.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip