KPMG Named Auditor for Quantum Tech Firm Infleqtion, Replacing Withum

Just five weeks after its NYSE debut, Infleqtion tapped KPMG to audit the first publicly listed neutral-atom quantum company, a $550M SPAC-born issuer.

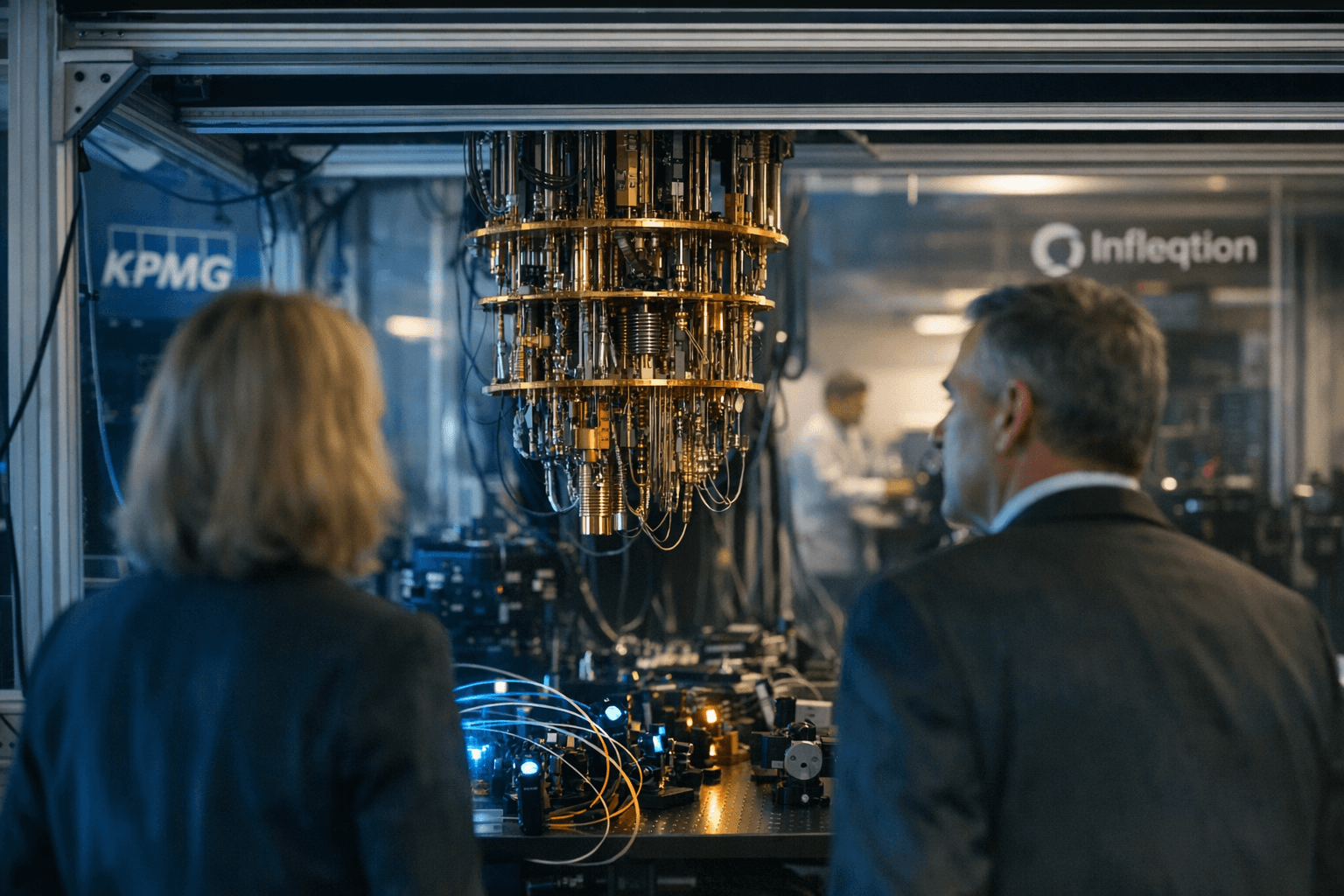

Just five weeks after Infleqtion, Inc. began trading on the New York Stock Exchange as the first publicly listed neutral-atom quantum technology company, its audit committee voted to bring in KPMG LLP. The March 20, 2026 decision, disclosed in a Form 8-K filed with the SEC on March 26, hands KPMG its inaugural audit of a company that raised more than $550 million through its SPAC merger with Churchill Capital Corp X and carries a balance sheet shaped almost entirely by R&D investment and advanced physics IP.

The appointment replaces WithumSmith+Brown, which was dismissed effective upon completion of its then-ongoing audit. The 8-K, filed under Item 4.01 of SEC reporting rules governing changes in certifying accountants, recorded no disagreements and no reportable events between Infleqtion and Withum during the periods covered. The handoff is procedurally clean; the audit work ahead is anything but.

For KPMG's technology-sector audit practice, a first-year engagement at a freshly listed issuer is always intensive. At Infleqtion, the complexity compounds: neutral-atom quantum technology sits at the outer boundary of what most accounting standards-setters have contemplated, which means auditors will need to make defensible judgments on R&D capitalization, stock-based compensation, going-concern evaluation, and technical disclosures without the benefit of comparable-company precedent. Staffing the engagement will likely require pulling in technical accounting specialists, IT auditors, and valuation support alongside the core audit team.

The workload will land unevenly across experience levels. Associates and seniors will absorb the bulk of onboarding activity: scoping sessions, evidence inventories, control walkthroughs, and internal control testing. Managers and directors carry the weight of technical review and PCAOB inspection-readiness documentation, which on a first-year engagement requires building the audit file largely from scratch. Partners and directors also carry governance and client-committee oversight responsibilities that accompany any newly acquired public-company client.

Infleqtion's SPAC pathway adds a layer of scrutiny that KPMG will need to account for explicitly. Companies that complete SPAC mergers often arrive at their first full year as SEC reporting issuers with internal control environments still maturing, which shifts more of the audit burden toward evaluating control design rather than relying on operating effectiveness. That foundational work tends to extend audit timelines and generate exactly the kind of documentation that PCAOB inspectors examine closely when reviewing new engagements.

The engagement arrives at a moment when quantum computing is attracting serious capital market attention. Infleqtion's $550 million raise and NYSE debut under ticker INFQ, which began trading February 17, 2026, place it squarely in the category of high-profile, high-scrutiny clients that strengthen KPMG's positioning in the deep-technology sector. For audit professionals building toward partner, landing early on engagements with this kind of market visibility tends to carry real weight in promotion cycles. The first KPMG year-end at Infleqtion will be demanding; it will also be noticed.

Know something we missed? Have a correction or additional information?

Submit a Tip