KPMG says Argentina M&A surged 63% to US$8.5 billion in 2025

Argentina’s deal value jumped to US$8.5 billion, and KPMG deal teams now face heavier cross-border advisory, tax and risk workloads as first-time investors pile in.

KPMG’s latest Argentina M&A readout shows a market that was busier to execute than the headline number suggests. Deal value climbed 63% to US$8.5 billion in 2025, while transaction count still topped 100, up 1% from 2024. For KPMG deal teams, that combination matters more than the percentage gain alone: more than 100 transactions, three headline-grabbing billion-dollar deals and a wave of new foreign entrants point to a heavier workload across transaction advisory, tax structuring and risk review.

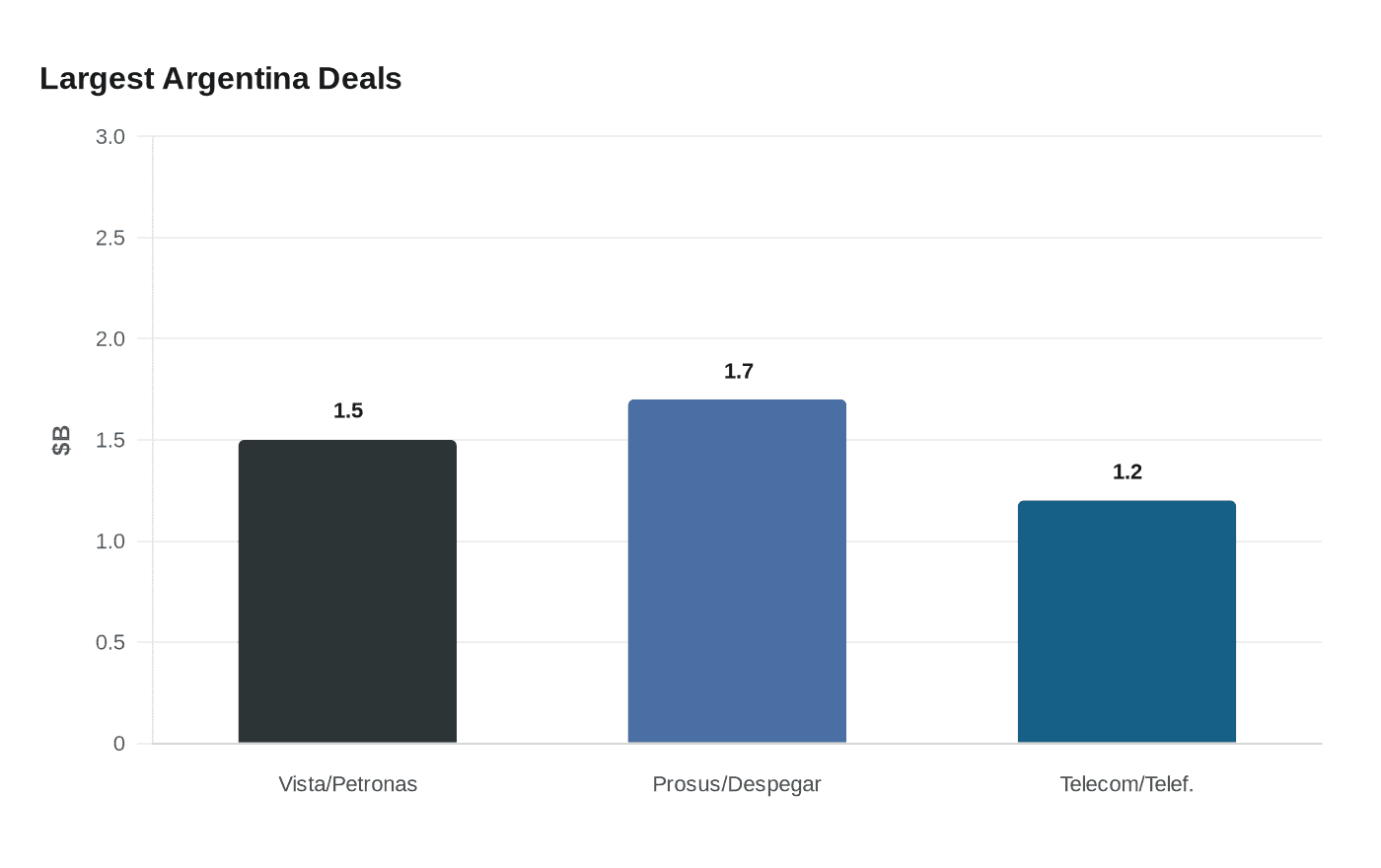

The biggest deals were concentrated in the sectors that tend to demand the most cross-border coordination. Energy and Natural Resources and Technology, Media and Telecommunications led the market, with strategic buyers driving activity while private equity stayed cautious. Vista bought Petronas assets for US$1.5 billion, Prosus acquired Despegar.com for US$1.7 billion, and Telecom paid US$1.2 billion for Telefónica’s Argentine operation. Those transactions are the kind that stretch diligence teams, especially when financing, regulatory approvals and local operating issues all have to line up at once.

That workload is likely to be sharper because the investor base is changing. KPMG said local buyers regained a larger role in the second half of 2025, while almost half of the international investors were entering Argentina for the first time. For practitioners inside KPMG, that means more time spent explaining Argentina-specific tax, customs, foreign-exchange and legal issues to groups that are still learning the market, particularly as new mandates bring in clients from the United States and Brazil.

The rebound did not happen in a vacuum. KPMG said 2025 activity was still shaped by political uncertainty and financial volatility, but sentiment improved in the final quarter after election results favored the current government and strengthened expectations for a more predictable medium-term outlook. The backdrop already had improved in 2024, when M&A returned toward 2017-2019 deal-count levels as inflation eased, foreign-exchange controls loosened and President Javier Milei’s pro-investment framework, including the Bases Law and the RIGI regime, took hold.

That policy mix mattered because RIGI is designed to give large investments stability and legal protections, with tax, customs, legal and foreign-exchange benefits for projects above US$200 million. Chambers and Partners said oil and gas and energy accounted for about 30% of deals and 60% to 70% of value, with RIGI-linked work flowing into lithium, copper, renewable energy and Vaca Muerta projects. It also noted a privatization push involving more than 50 publicly owned firms. Add that pipeline to the US$8.5 billion already booked in 2025, and 2026 looks less like a simple rebound than a staffing test for the firms handling the work.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)