KPMG says OECD’s new global minimum tax toolkit leaves key gaps unanswered

OECD's new Pillar Two toolkit gave tax teams more detail, but KPMG said it also exposed how differently countries are applying the same rules before June 30 filings.

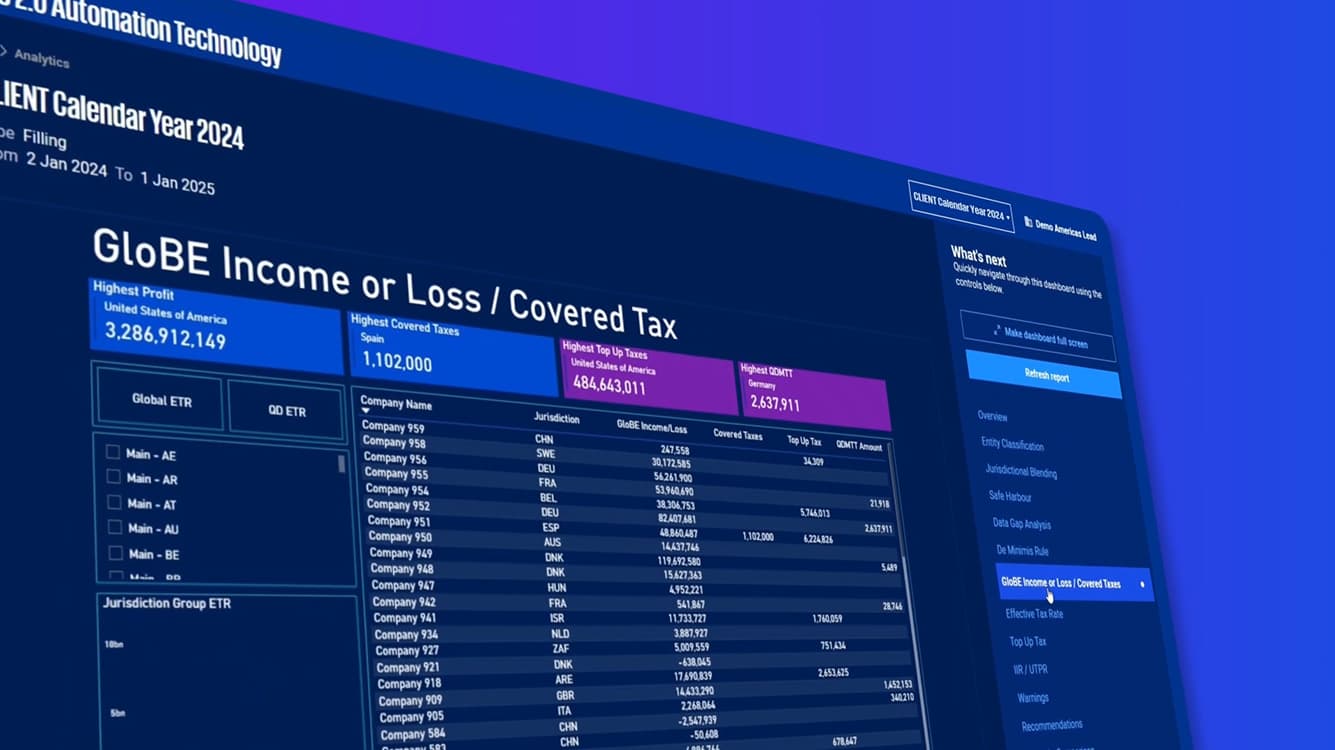

The OECD's latest Pillar Two toolkit landed just as international tax teams are bracing for the first big filing crunch: June 30, 2026 top-up tax information returns for calendar-year groups. KPMG said the April 30 release, its first update since the January side-by-side package, did not close the gap between a global minimum tax on paper and the patchwork of local interpretations firms now have to manage.

KPMG's read is that the toolkit is aimed mainly at tax administrations, but that is exactly why it matters inside firms. The OECD said the package was built to help authorities apply the Global Minimum Tax consistently and cut administrative and compliance burdens, using input from jurisdictions further along in implementation and from business and wider stakeholder groups. KPMG's analysis said the practical effect for clients is different: the toolkit makes visible how much variation still exists in local rule interpretation and application across jurisdictions.

That variation is where the workload multiplies. KPMG said the toolkit called for grace periods for return correction, penalty relief and filing extensions where warranted, but it remains unclear whether tax authorities will adopt those approaches. For KPMG teams, that means more cross-border coordination, more review of country-by-country filing mechanics and more judgment calls when one administration moves differently from another. It also means more client questions about timing, documentation and whether a position taken in one market will hold up elsewhere.

The pressure is already shifting from policy design to execution. The European Commission said in-scope multinationals are expected to file their first top-up tax information return by June 30, 2026, with tax authorities exchanging the information by December 31, 2026 at the latest. Luxembourg has already published registration and filing forms for calendar-year 2024 in-scope groups with the same June 30 deadline, while EY said that date is the first major filing deadline for 2024-tax-year Pillar Two compliance. Australia has also been adding administrative guidance, including relief for certain first-year filings, underscoring how differently the same regime is being implemented.

KPMG's EU Tax Centre said the toolkit was developed through the Amsterdam Dialogue involving the OECD-led Forum on Tax Administration and business representatives. That is a sign the OECD is still trying to smooth implementation across the OECD/G20 Inclusive Framework, which said more than 145 countries and jurisdictions agreed on key elements of the global minimum tax package in late 2025. But for the people doing the work, more alignment on the margins does not erase the central problem: Pillar Two remains a country-by-country reconciliation exercise, and every new guidance document can add another layer of review before the filing clock runs out.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)