KPMG survey finds tariffs driving price hikes and supply chain changes

Tariffs are now forcing KPMG clients into price hikes, supply chain redesigns, and delayed deals, turning trade work into an all-hands advisory issue.

Tariff pressure has moved from theory to client-side triage

KPMG’s latest tariff survey shows a sharp shift in how large U.S. companies are handling tariff costs: 34 percent were passing through 51 percent to 100 percent of those costs to customers in February 2026, up from 13 percent in May 2025. That is not a modest pricing adjustment. It signals that the work facing KPMG teams is now about how to defend margins, justify increases, and manage the knock-on effects when customers push back.

For consultants, auditors, and tax professionals inside the firm, that changes the shape of the assignment. Tariffs are no longer just a trade policy issue or an import cost line item. They are forcing client conversations about pricing architecture, revenue pressure, inventory positioning, sourcing strategy, disclosures, and scenario planning all at once.

The cost shock is showing up across the income statement

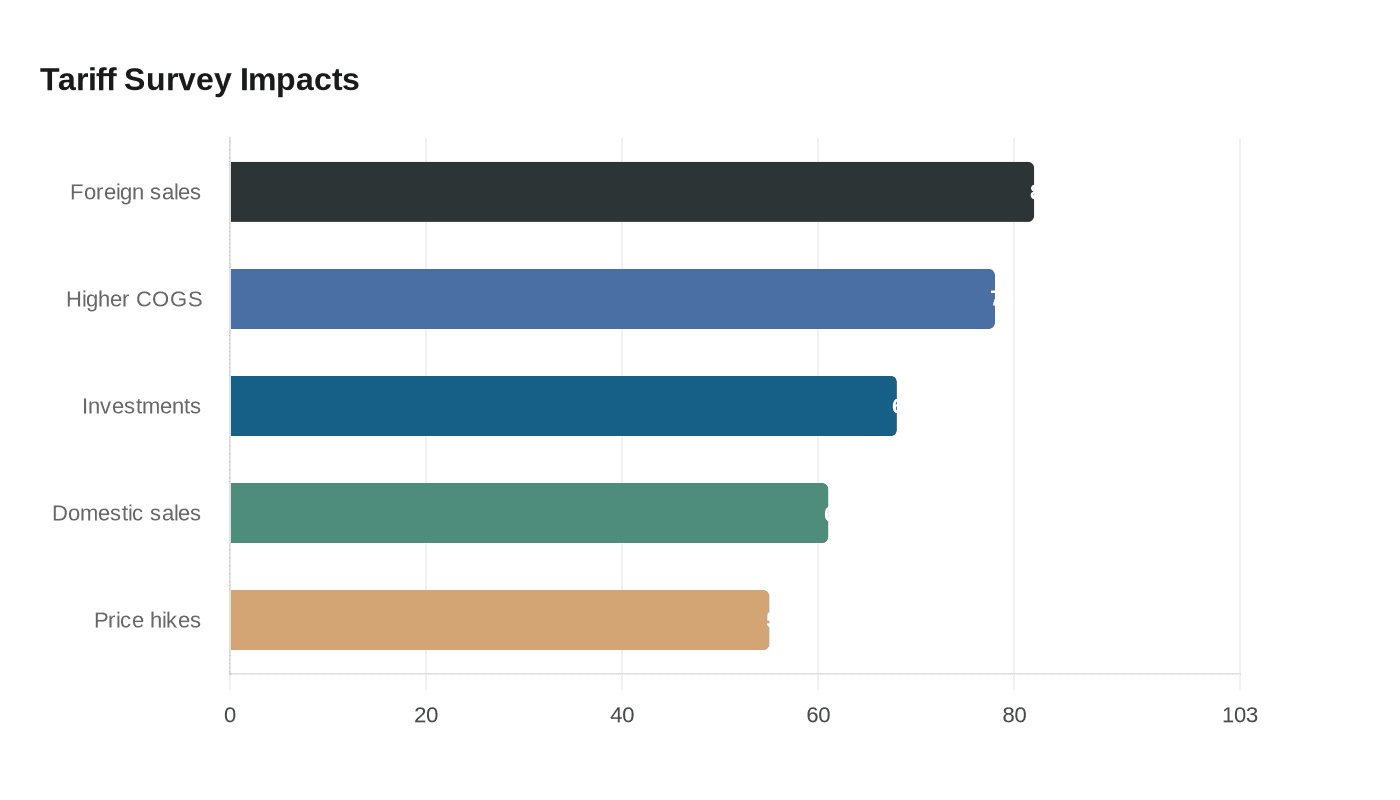

The survey, which KPMG fielded in February and March 2026 with 300 U.S. C-suite leaders at companies with at least $1 billion in annual revenue, found that 78 percent of organizations reported higher cost of goods sold in their most recent fiscal quarter. At the same time, 55 percent of executives said they plan additional price increases of up to 15 percent in the next six months.

That combination matters because it shows tariffs are not being absorbed quietly. They are moving through the business in two directions at once: up the cost base and out to the customer. For KPMG teams, that means more pressure on finance functions to explain margin erosion, more demand for pricing models that hold up under scrutiny, and more sensitivity around how fast a company can raise prices without losing volume.

Clients are feeling the demand hit as well as the cost hit

The survey also shows that tariff pressure is weakening demand, not just raising expenses. KPMG says 82 percent of organizations reported declining foreign sales, while 61 percent reported declining domestic sales. That suggests the issue goes beyond import exposure. Clients are seeing competitiveness strain across markets, which makes every pricing decision more delicate.

For KPMG employees advising operating teams, that means the work gets harder fast. A client that can pass on part of a tariff to customers still has to think about whether higher prices will erode domestic sales. A company that loses export demand has to reassess production, inventory, and market strategy. The result is a deeper set of trade-offs than “absorb or pass through.”

Supply chains are being redesigned, not just defended

KPMG says many organizations are moving from short-term tariff defense toward longer-term structural changes such as reshoring and supply-chain redesign, while still remaining cautious about the policy environment. That shift is important for advisory teams because it changes the client conversation from emergency response to operating model redesign.

The report also shows that sourcing and trade relationships have not fully reset. KPMG says China, Europe, and Mexico remain central import partners, while Europe, Canada, and Mexico remain central export partners. The trading map may look familiar, but the economics around it have changed, with sourcing costs rising and foreign demand dropping. That puts more pressure on teams helping clients decide whether to re-source, nearshore, dual-source, or redesign product flows altogether.

Investment, M&A, and strategy are slowing under tariff uncertainty

The survey found that 68 percent of organizations postponed major investments. Of those delays, 48 percent were by 1 to 12 months, and 20 percent were by 13 to 24-plus months. KPMG also says delays in M&A and strategic partnerships rose to 48 percent in February 2026 from 24 percent in May 2025.

That is one of the clearest signs that tariffs are affecting decision-making risk inside client organizations. Deals are not just being priced differently. They are being postponed because buyers and sellers cannot easily model future margins, imported input costs, or retaliatory trade effects. For KPMG professionals, this means more work in diligence, valuation, integration planning, and scenario analysis, with a premium on showing how tariff exposure flows into deal economics.

The legal backdrop is still part of the client conversation

KPMG says a recent U.S. Supreme Court ruling improved near-term sentiment, but most organizations remain cautious. The caution is understandable. In KPMG’s February 20, 2026 legal analysis, the Supreme Court held that the president cannot use the International Emergency Economic Powers Act to impose tariffs, while leaving the refund mechanics unresolved.

That unresolved piece matters to businesses because it keeps the policy environment from feeling settled, even if the legal direction appears clearer. The Supreme Court’s decision may have improved sentiment, but it did not eliminate the operational problem for companies that have already paid tariff-related costs or built pricing around them. KPMG teams advising on trade compliance, tax, and disputes will keep getting asked the same practical question: what happens next, and how much money is at stake if the rules shift again?

Why this survey matters inside KPMG

This is the kind of report that reaches far beyond the trade team. Tariffs are now touching pricing, revenue recognition, inventory strategy, sourcing, disclosures, and scenario planning in the same client conversation. That creates a broader coordination problem for KPMG professionals, especially when advisory, tax, and audit teams need to align on how a client explains margin pressure and operational change.

The biggest takeaway is that tariff work is no longer niche. It is business model work. For KPMG staff, that means the value comes not from reacting to headlines, but from helping clients redesign around sustained cost pressure, slower investment, and weaker demand. In that environment, the firms that can connect trade rules to pricing decisions and supply chain strategy will be the ones clients call first.

Know something we missed? Have a correction or additional information?

Submit a Tip