KPMG survey shows CEOs accelerating AI, M&A and cyber investments

CEOs are still spending on AI, cyber and deals, and KPMG teams will feel it in transformation work, controls and talent planning.

AI is no longer a side bet

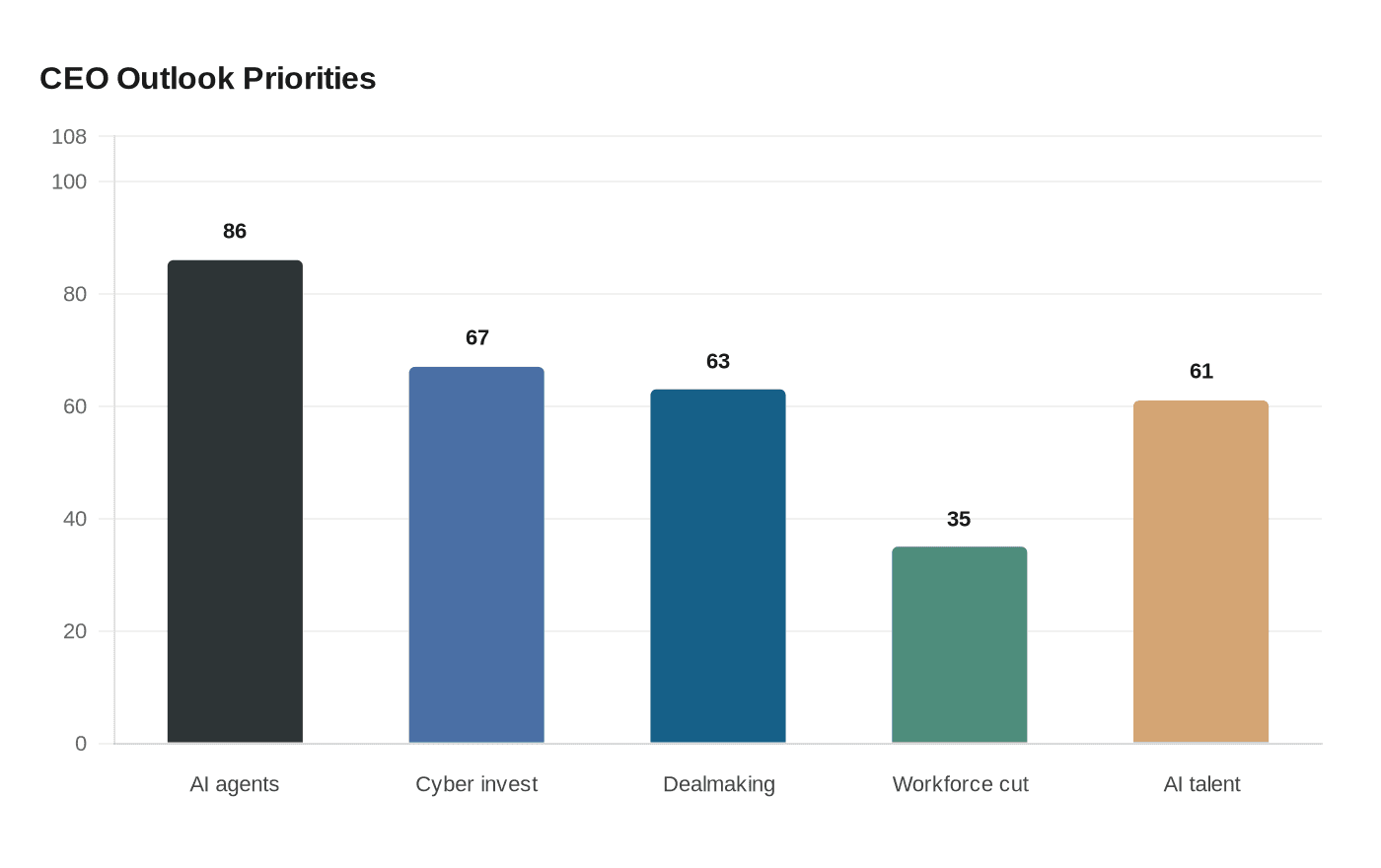

The clearest signal from KPMG U.S.’s 2026 CEO Outlook Pulse Survey is that large-company leaders are not pulling back. Among 100 U.S. CEOs at companies with more than $500 million in annual revenue, 63% say they will actively pursue dealmaking in 2026, 67% are increasing cybersecurity investment, and nearly 80% are putting at least 5% of capital budget into AI. More than one-third of the companies in the survey have annual revenue above $10 billion, so this is a view from budgets that can actually move markets, not from the sidelines.

For KPMG employees, the practical message is simpler than the headline suggests: client demand is moving toward execution, not experimentation. CEOs are choosing a smaller set of priorities, but they are funding them more aggressively, which should translate into more work in transformation, operating model redesign, controls, and change management.

AI is becoming part of the workforce

The most telling number may be the one about labor, not technology. KPMG says 86% of CEOs expect AI agents to be embedded team members next year, while 35% are planning workforce reductions in some areas over the next 2 to 5 years because of AI. At the same time, 61% are worried about whether they can hire the technical AI talent they need. That combination points to a client conversation many KPMG teams are already having: companies want productivity gains, but they also need a credible plan for reskilling, role redesign, and governance.

Tim Walsh, KPMG U.S. Chair and CEO, said AI agents are already informing supply chain strategy, defending against cyberattacks, and enhancing workforces, and that the “real benefits” come when organizations embed AI into entirely new business models and ways of working. That is the part to watch. The money is not just going into pilots or copilots anymore; it is going into the plumbing of how work gets done. For consultants, that means more demand for process redesign and adoption work. For auditors and risk teams, it means more scrutiny around model governance, data quality, access controls, and the way management proves that automation is doing what it says it is doing.

Dealmaking is still on, but only where the thesis survives

The survey also says 52% of CEOs view policy uncertainty, including tariffs, interest rates and regulation, as the top pressure on short-term decisions. That helps explain why 63% still plan to pursue deals: growth is not dead, but CEOs want transactions that can survive a tougher policy and cost environment. The likely result is more selective M&A, with stronger emphasis on diligence, integration, carve-outs, and scenario planning.

That is where KPMG’s advisory teams should expect more traction. When companies are weighing acquisitions against supply chain changes, tariff exposure, or automation savings, they need more than a standard deal model. They need a story that connects the acquisition to resilience, margin, and speed. The 2025 KPMG U.S. CEO Outlook found that 89% of CEOs said tariffs would significantly affect business performance and operations over the next three years, which shows how persistent that pressure has been. The 2026 survey suggests CEOs are still working through that problem, but they are doing it while keeping dealmaking on the table.

Cyber and supply chain are converging

Cyber is another area where the budget signal is unmistakable. KPMG says 67% of CEOs are increasing cybersecurity investment, and the survey specifically tracks supply chain strategy, AI strategy, talent and workforce strategy, and cyber and technology risk. That matters because AI is not only creating new efficiency opportunities, it is also adding new attack surfaces and new dependencies on data, vendors and automation.

For KPMG teams, this is where the client conversation shifts from abstract risk to operating reality. If AI agents are helping route decisions, inform supply chains, or assist employees, then cyber controls, segregation of duties, incident response, and third-party risk all become part of the same discussion. Audit teams will feel that in board agendas and in the depth of questions around internal controls, while advisory teams will see more demand for cyber transformation, resilience planning and technology risk work.

What this means for hiring, workload and the partner track

The workforce implications are as important as the tech spend. With 61% of CEOs worried about hiring the technical AI talent they need, firms that can combine technical fluency with business judgment will have an edge. At KPMG, that should favor people who can bridge domains: AI strategy and controls, cyber and operations, deal work and supply chain, transformation and compliance.

It also changes what good performance looks like inside a Big 4 environment. The work that tends to get noticed in client accounts is the work that turns a strategy into measurable outcomes, whether that means faster deployment, cleaner controls, stronger cyber posture, or a more credible workforce transition. In practical terms, that can affect staffing decisions, workload mix during busy periods, and the kinds of projects that build visibility on the path to manager, senior manager and eventually partner.

Why this survey matters now

KPMG’s earlier CEO surveys show the arc. In 2024, the firm framed the operating environment as “compound volatility” and said 87% of CEOs were confident in U.S. economic growth over the next year. In 2025, tariffs became the dominant pressure point. In 2026, the story is more specific: uncertainty is still there, but it is no longer stopping investment in AI, cyber and deals. It is pushing CEOs to be choosier about where they spend.

That is the real takeaway for KPMG employees. Clients are not asking whether AI matters anymore. They are asking how fast they can embed it, how they protect it, who they need to hire, and what it means for growth, controls and risk. The firms that can answer those questions in business terms, not just technology terms, will be the ones that stay closest to the work.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)