Supreme Court tariff refund ruling triggers complex KPMG tax workload

The Supreme Court opened the door to tariff refunds, but KPMG says the real lift is tracing entries, fixing filings and managing accounting before cash arrives.

A Supreme Court win over IEEPA tariffs has quickly become a new workflow problem for KPMG tax teams, because the ruling opened the door to refunds without explaining how those refunds will actually be issued.

KPMG said the U.S. Supreme Court held 6-3 on Feb. 20, 2026, that the International Emergency Economic Powers Act does not authorize tariffs, but the opinion did not spell out whether or how companies would get their money back. Justice Brett Kavanaugh warned in dissent that the refund process is “likely to be a mess,” and that warning now looks less like rhetoric and more like a project plan.

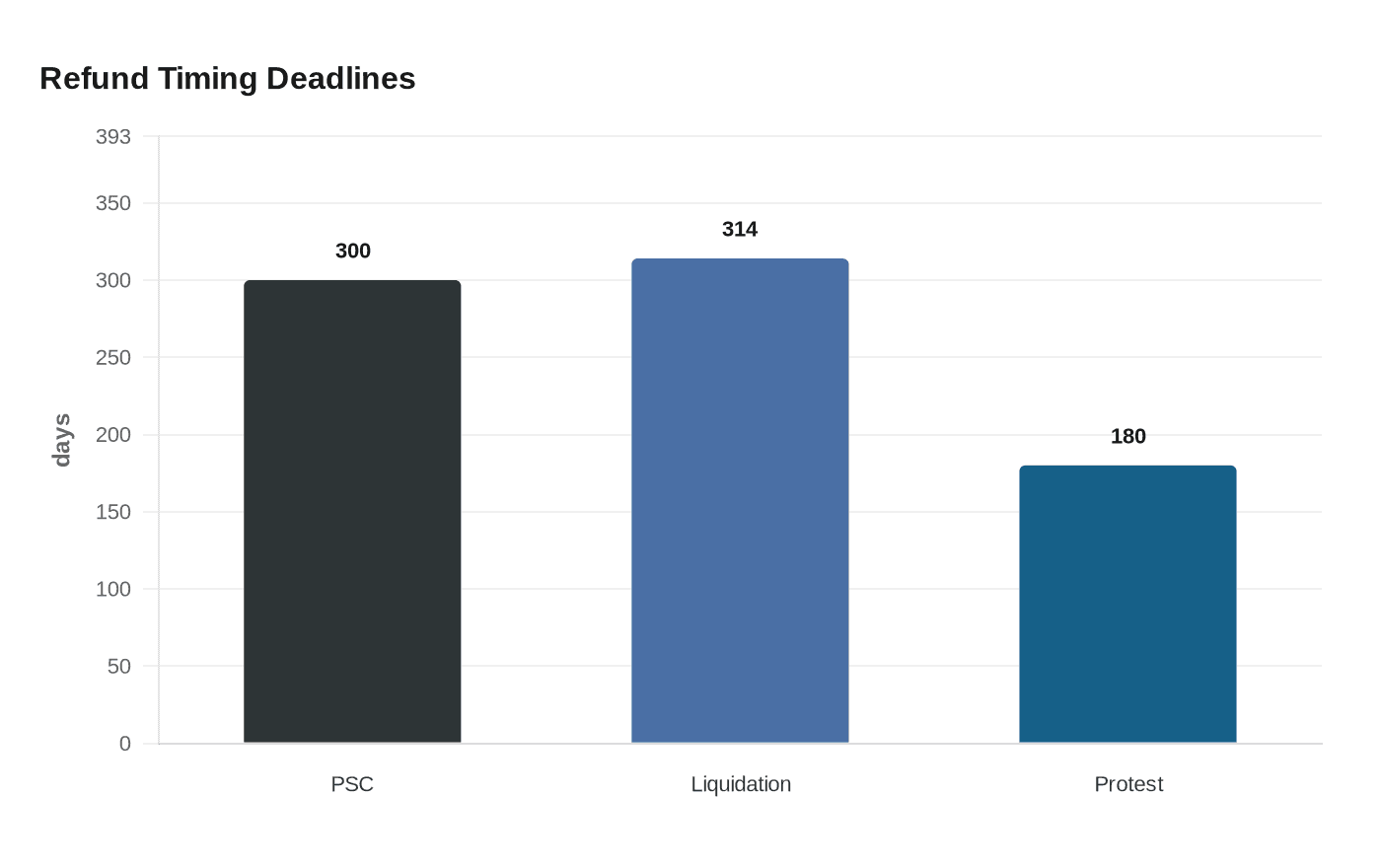

For firms advising importers, the first job is not refund math. It is record work. KPMG said importer of record rules, U.S. Customs and Border Protection entry documentation, post-summary corrections, liquidation, and protests are central to the process. Post-summary corrections are generally available within 300 days of entry, liquidation generally occurs after 314 days, and protests can be filed within 180 days after liquidation. That puts immediate pressure on teams trying to decide which entries are still open, which filings need to be amended, and which claims may already be locked into a narrower procedural lane.

The scale is large enough to strain client teams as well as advisers. Skadden has said more than 330,000 importers paid IEEPA duties across more than 53 million entries, with about $165 billion in unlawfully collected duties at issue. That is the kind of number that pushes work across tax, customs, treasury, finance and legal, with each group owning a different piece of the file. A tax lawyer may focus on claim eligibility, a customs specialist on entry data, an accounting team on recognition and presentation, and a finance transformation group on workflow and controls.

KPMG’s April 2026 financial-reporting note said the ruling raised subsequent-events disclosure questions under ASC 855. It also pointed to the Court of International Trade’s March 4, 2026 order directing the Trump administration to begin refunding IEEPA tariffs, while noting that an appeal could still change the path forward. That uncertainty matters because even a valid refund right can take time to prove, quantify and collect, leaving companies to model timing, reserve impacts and disclosures before any cash comes back.

The ruling did not end all tariff work either. Thomson Reuters noted that other regimes, including Sections 232, 301 and 122, remain in force, which means tax teams are juggling refund claims from one legal channel while broader trade exposure continues elsewhere. For KPMG professionals, that turns a headline court decision into the kind of multi-disciplinary surge assignment that can swallow a filing season fast.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

.pdf%2F_jcr_content%2Frenditions%2Fcq5dam.thumbnail.319.319.png&w=1920&q=75)