McDonald's shares slip as investors weigh stable cash flow model

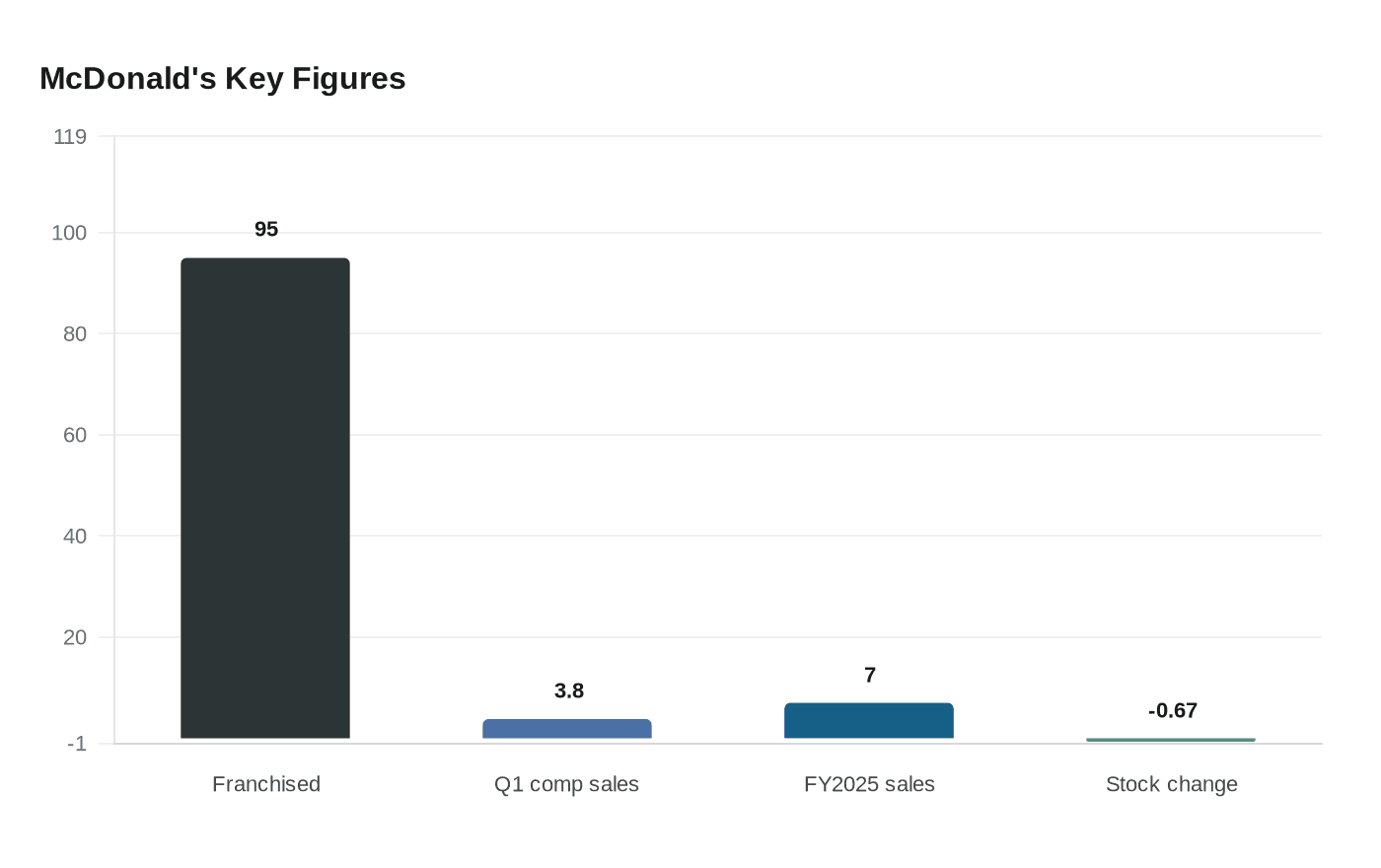

McDonald’s shares fell 0.67%, but the real workplace story is how Wall Street’s faith in the company’s cash machine can shape staffing, tech spending and labor pressure.

McDonald’s ended the day at $282.27 a share, down 0.67%, a move that says less about one trading session than about the way investors still value the company’s steady cash engine. For restaurant workers, that matters because a business built to please Wall Street often turns first to the same levers on the floor: tighter labor controls, faster service standards, and more pressure to keep every shift running cleanly.

The company’s own filing shows why investors stay interested. McDonald’s said its heavily franchised model is designed to produce stable and predictable revenue and cash flow, and franchised restaurants made up about 95% of its worldwide locations at December 31, 2025. That structure gives corporate leadership flexibility to fund development, technology upgrades and brand spending, but it also pushes operating risk down into the restaurants, where franchisees have to make the numbers work day after day.

The market page itself showed the scale of that confidence. McDonald’s traded between 280.40 and 283.73 on May 22, with volume of about 3.06 million shares and a 52-week range of 271.98 to 341.75. The company’s board also declared a quarterly cash dividend of $1.86 per share on May 20, payable June 16 to shareholders of record June 2, another signal that cash returns remain central to the story.

That shareholder emphasis does not automatically translate into better shifts, higher pay or easier staffing. It does, however, shape the operating climate in which crew members and managers work. When investors pay up for predictability, McDonald’s has more room to invest, but it also faces pressure to protect margins and traffic. On the floor, that often means a sharper focus on speed, consistency and labor efficiency, the same tensions that have long fueled fights over staffing levels, Fight for $15 campaigns and minimum wage laws.

The latest operating results help explain why the model still draws capital. McDonald’s said first-quarter 2026 global comparable sales rose 3.8%, global systemwide sales increased 11% to more than $34 billion, and sales to loyalty members across 70 loyalty markets topped $38 billion over the trailing 12 months. In full-year 2025, systemwide sales topped $139 billion, up 7%. For workers, the signal is plain: strong corporate cash flow can support restaurant investment, but it can just as easily reinforce the discipline that keeps labor, equipment spending and training decisions under constant scrutiny.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?