monday.com employees can boost savings with 2026 401(k) limits

The 2026 401(k) cap rises to $24,500, but monday.com’s 3% employer contribution may matter more over time. Missed matches after raises or job changes still cost real money.

The IRS has lifted the 2026 401(k) employee limit to $24,500, but the bigger compensation story at monday.com is the money you can get from the company on top of your own paycheck. Public benefits listings say monday.com contributes 3% of an employee’s annual gross pay regardless of whether the worker contributes anything, which turns retirement savings into part of total comp instead of a nice-to-have perk. On a $150,000 salary, that is $4,500 a year from the employer alone, and invested for 20 years at 7% it grows to about $184,480 before a worker adds a single dollar of their own.

Why the 2026 limit matters, but only after the match

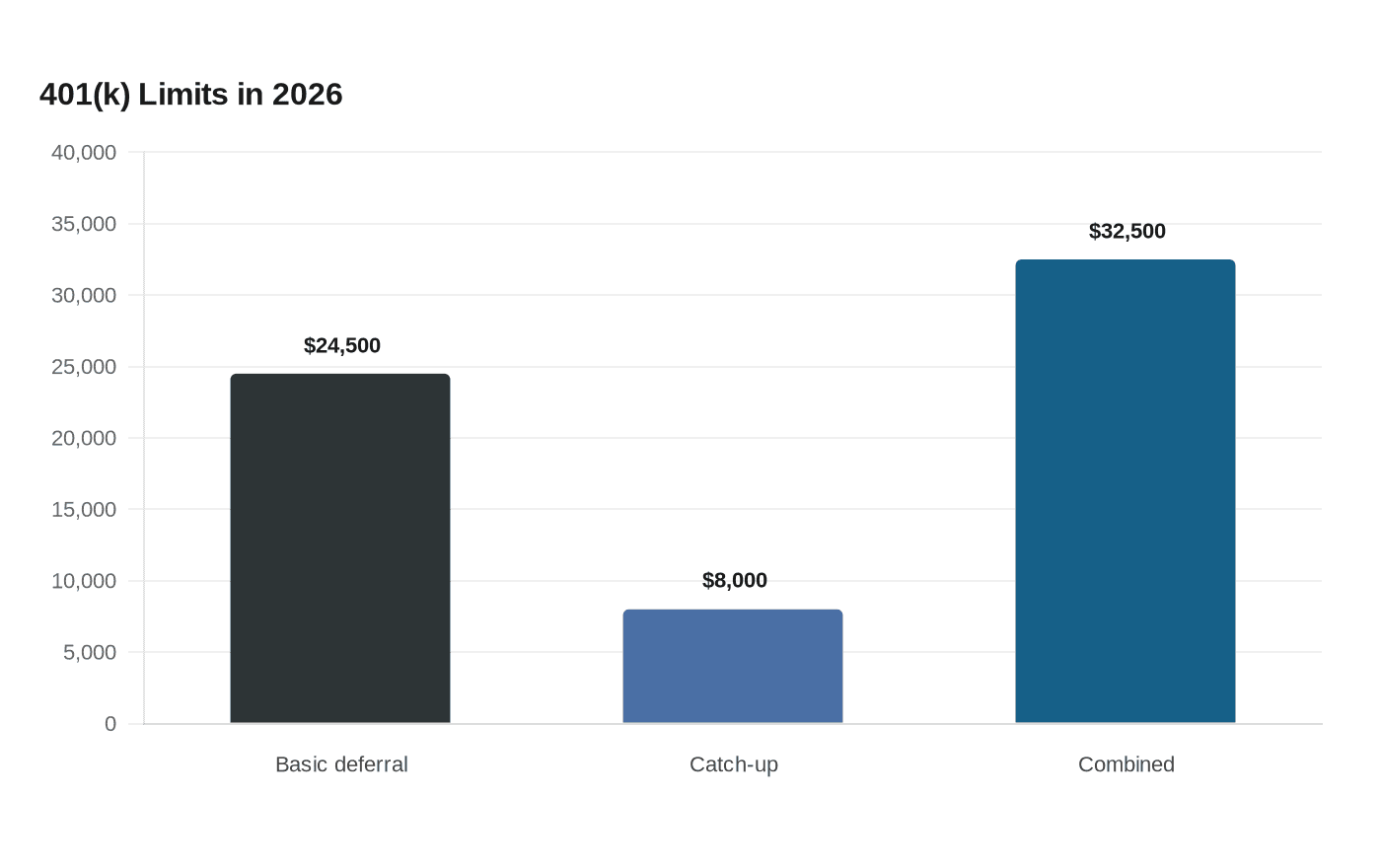

The IRS says the basic elective deferral limit is $24,500 in 2026, up from $23,500 in 2025, and workers age 50 and older can add a catch-up contribution of $8,000 for a combined $32,500 if their plan allows it. That is the ceiling on employee salary deferrals, not a target every monday.com employee should ignore or chase blindly. The Department of Labor says employers can match employee deferrals, contribute for all participants, do both, or do neither, which is why the structure of the plan matters just as much as the headline limit.

Traditional and Roth 401(k) contributions also change the tax timing, not just the retirement outcome. Traditional elective deferrals are generally pre-tax, which lowers current taxable income, while designated Roth contributions are made after tax and qualified distributions are generally tax-free. For employees deciding whether to lean Roth or traditional, the real question is whether they expect their tax rate to be higher later, lower later, or under pressure right now from rent, childcare, or a mortgage that already eats a big chunk of their paycheck.

monday.com’s market backdrop makes that tradeoff feel less abstract. The company’s investor relations page says more than 250,000 customers worldwide use its platform, and its stock has been volatile enough to remind employees that equity is not the same thing as guaranteed savings. MNDY closed at $67.09 on June 25 and was down 54.53% year to date, which is one reason the retirement benefit deserves more attention than it usually gets in onboarding decks.

What monday.com’s plan actually says

Public benefits listings say monday.com offers a 401(k) matching plan and contributes 3% of annual gross pay regardless of the employee contribution. Those same listings name ADP on one page and TriNet on another, which is a useful reminder that payroll and plan administration details are worth verifying in your own benefit materials instead of assuming every teammate is on the exact same setup. For a worker, the practical point is simple: this is not a symbolic perk. It is recurring retirement pay that shows up whether you are having a good month or a bad one.

That makes the vesting language especially important. The Department of Labor says employer contributions can be subject to a vesting schedule, and IRS guidance says qualified defined contribution plans can range from immediate vesting to full vesting after three years of service. In other words, the money may be posted to your account before it is fully yours. If you leave before vesting, some employer dollars can disappear, which is why the plan document matters just as much as the contribution rate.

The operational mistakes that quietly shrink your savings

The biggest mistake after a raise is staying on autopilot. A higher salary can make your savings look healthier without you changing anything, but that only helps if your contribution rate actually keeps pace with pay. If you never revisit your elections, it is easy to think you are saving aggressively while still sitting well below the 2026 cap and leaving part of the employer contribution pattern untapped.

Job changes are another place where money goes missing. A worker who leaves before employer contributions vest may forfeit some of the company dollars, and a new role can mean a different payroll rhythm, a different plan administrator, or a fresh enrollment window. That is especially relevant in a company like monday.com, where employees move between engineering, product, sales, and go-to-market teams and where benefit setup details can differ by source even when the headline benefit looks the same.

Enrollment season is where the most boring mistake can become the most expensive one. The DOL says a 401(k) plan exists in part because it lets participants decide how much to contribute, but that flexibility cuts both ways: if you do not actively set the rate, the default may be lower than you intended. For workers age 50 and older, the catch-up contribution is there to help close the gap, but only if you actually elect it and only if the plan supports it.

How to read the benefit like a compensation person, not a brochure reader

The comparison point worth keeping in mind is not another SaaS company’s pitch deck but a concrete large-employer benchmark. Target publicly says it matches dollar for dollar up to 5% of pay with immediate vesting. monday.com’s public listings point to a 3% employer contribution, but the impact depends on vesting, payroll setup, and whether you contribute enough to maximize the full annual opportunity under IRS limits. The gap between those designs is not abstract generosity versus stinginess. It is the difference between money that lands in your account and money that stays fully yours the minute it is contributed.

For monday.com employees, the smartest move is to treat the 401(k) as part of the same compensation stack as salary and equity. The stock can rise and fall, product cycles can change, and hiring markets can cool, but a well-used retirement plan turns a slice of every paycheck into durable savings before that cash gets absorbed by the rest of life. At a company selling AI work tools to more than 250,000 customers, the retirement tool inside your own benefits package is one of the few places where the defaults can still work in your favor.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip