Monday.com employees face 2026 IRS limits on HSAs, FSAs, and carryovers

Monday.com employees now have a sharper open-enrollment choice: HSAs can compound, while health FSAs cap at $3,400 with only $680 of carryover.

The numbers that actually change the decision

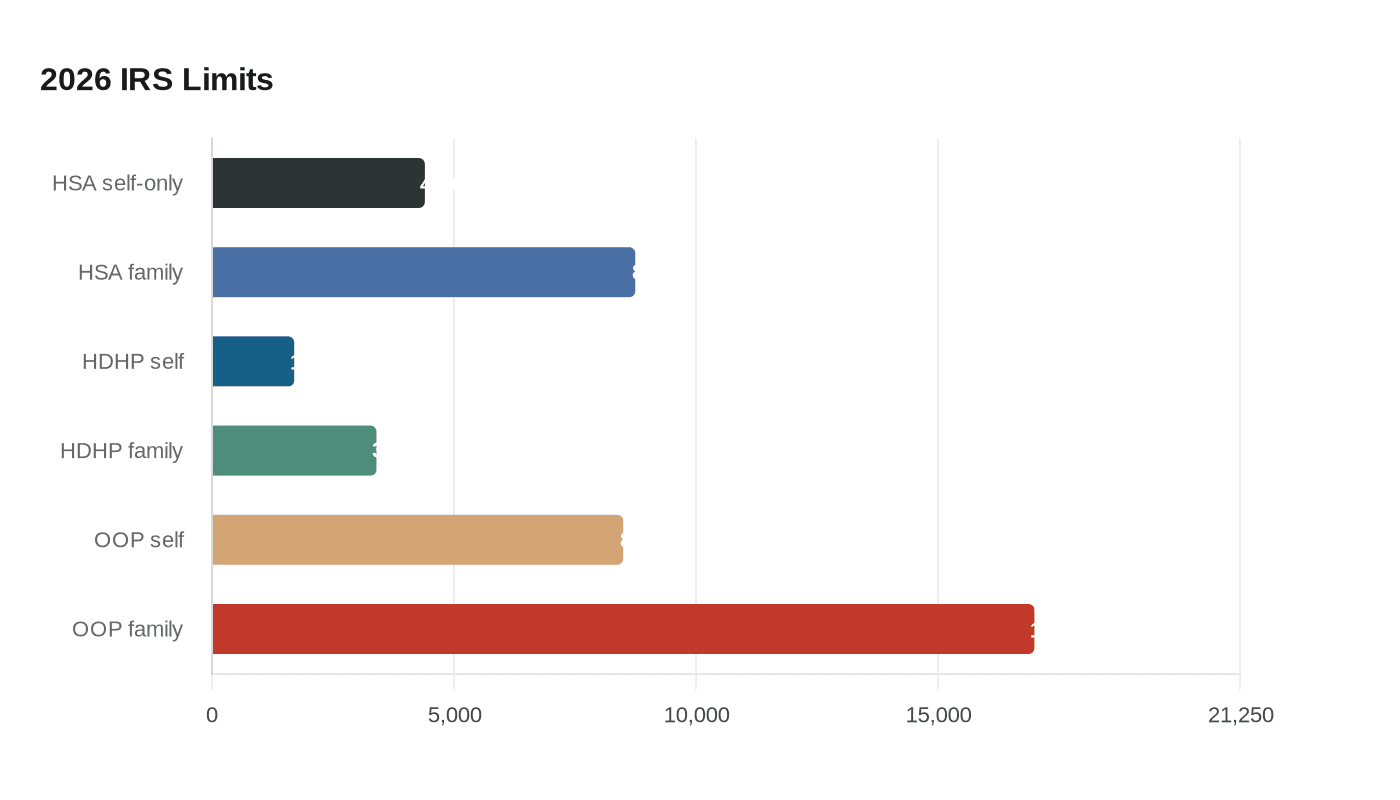

The 2026 IRS limits turn open enrollment from a paperwork exercise into a real budgeting choice. Publication 969, the IRS’s consolidated guide to HSAs, MSAs, FSAs and HRAs, now sits alongside 2026 guidance that sets the HSA contribution limit at $4,400 for self-only coverage and $8,750 for family coverage, with minimum HDHP deductibles of $1,700 and $3,400 and out-of-pocket maximums of $8,500 and $17,000.

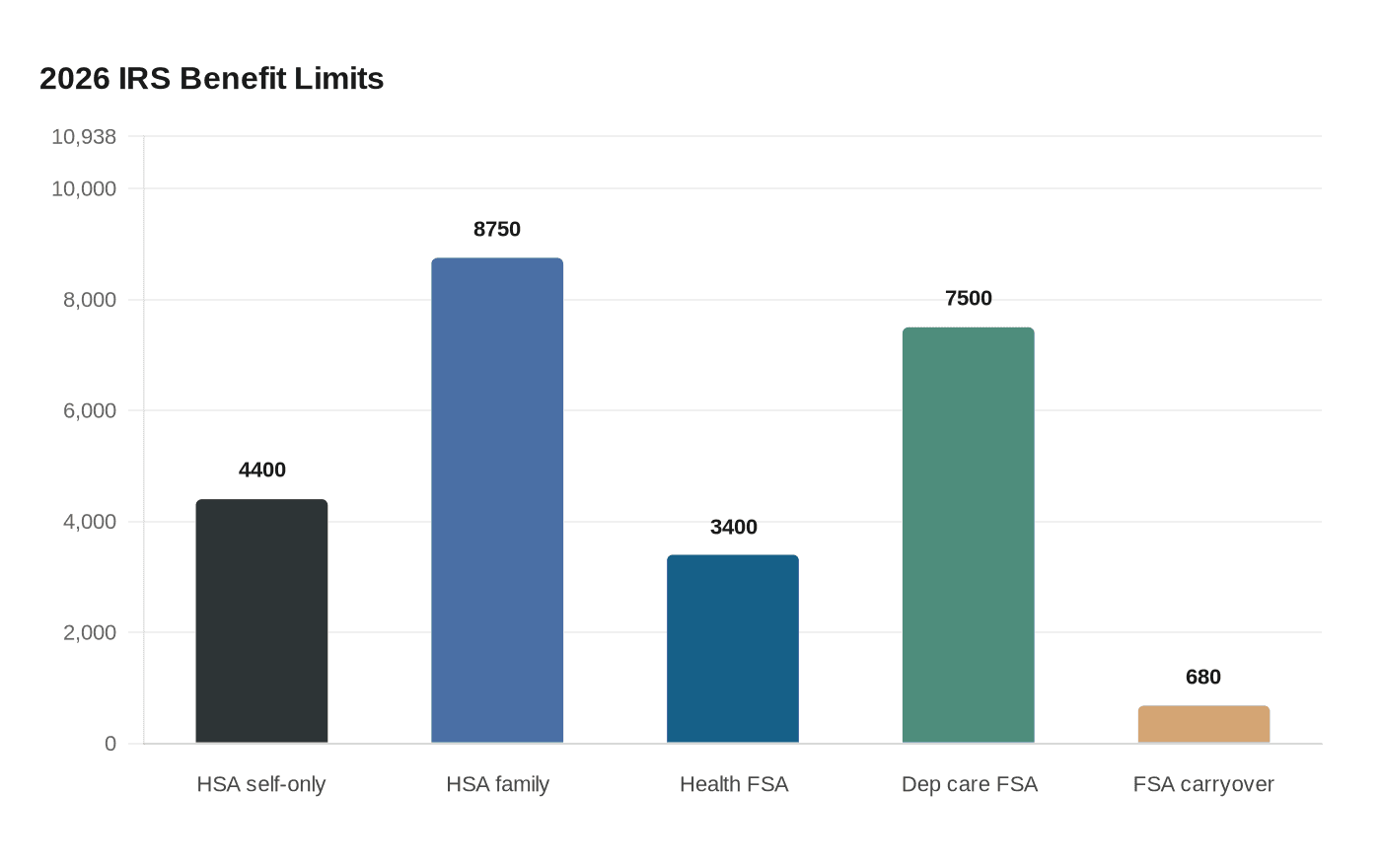

That matters because the health FSA rules move in a different direction. For plan years beginning in 2026, salary-reduction contributions to a health FSA cannot exceed $3,400, and if the cafeteria plan allows carryovers, the maximum unused amount you can bring into the next year is $680, up from $660 in 2025. The IRS also raised the dependent care FSA limit to $7,500, or $3,750 if you file married filing separately. Publication 969 was last reviewed or updated on March 30, 2026, which makes it the cleanest place to think through how all of these moving parts fit together.

HSA versus FSA is really a time-horizon question

For most monday.com employees, the practical decision is less about which account is “better” in the abstract and more about when you expect to spend the money. An HSA is built for people who want tax-advantaged savings that can sit there and grow over time for future medical costs. Contributions are deductible, growth is tax-deferred, and qualified medical withdrawals are tax-free, which is why the HSA’s appeal is so durable for people who can afford to leave the money untouched.

A health FSA works differently. It is usually the better tool if you expect predictable expenses during the plan year and want to pay them with pre-tax dollars as they come up. The tradeoff is that the account is tied much more tightly to the plan year, so you have to pay closer attention to how much you elect and whether your employer allows a carryover. That makes the FSA less of a long-term savings vehicle and more of a short-term spending plan with tax benefits.

The cleanest rule of thumb is simple: use the HSA if you want portability and a growing medical cushion, and use the FSA if you know you will have recurring expenses and want to reduce this year’s taxable pay. If you are trying to decide based on which one leaves less money stranded, portability and rollover rules are the first things to check.

Why monday.com employees should care more than most

That choice lands differently inside a fast-growing SaaS company like monday.com, which says more than 250,000 customers worldwide use its platform. The company filed its 2025 annual report on Form 20-F with the U.S. Securities and Exchange Commission on March 13, 2026, underscoring how public and global the business has become. Its public job postings also show that benefits can vary by role and geography, with some listings advertising fully covered individual health insurance and others mentioning private healthcare insurance.

The upshot is that employees should not assume they all see the same benefits menu. What matters is the actual U.S. open-enrollment package in front of you, whether the health plan is HSA-qualified, and whether the cafeteria plan allows a health FSA carryover. In a company with a distributed workforce and different regional benefits setups, the biggest mistake is assuming your colleague’s election fits your situation too.

For employees in the United States, the key test is whether the plan gives you enough room to use the HSA as a real savings account or whether the FSA is the more efficient place to park expected spending. At a company this size, the difference can show up in a few hundred dollars over a year, or in thousands if you consistently fund the HSA and keep the money invested for future care.

Three common employee scenarios

If you are healthy and want to build savings

If you rarely use medical care and can afford to cover current bills out of pocket, the HSA usually wins. The 2026 self-only contribution cap of $4,400 and family cap of $8,750 give you meaningful room to save, and the money stays with you if you change jobs or leave the company. That portability is the real advantage: the account is yours, not monday.com’s, and it does not reset just because your employment does.

This is especially compelling if your plan is HSA-qualified and your deductible fits your cash flow. For self-only coverage, that means the deductible has to be at least $1,700; for family coverage, at least $3,400. If you can handle that risk, the HSA can function as a health fund, an emergency buffer, and a tax shelter all at once.

If you know your costs will be predictable

If you expect regular prescriptions, ongoing treatment, therapy, or a cluster of medical bills you can already see coming, the health FSA may be the better fit. The 2026 cap of $3,400 is lower than the HSA limit, but it can still shave meaningful tax costs off a year in which you know you will spend the money anyway.

The catch is discipline. Elect too little and you leave tax savings unused. Elect too much and you may be relying on the $680 carryover, if your plan allows it, to avoid losing funds. That makes the FSA best for people who can estimate their expenses with some confidence and want the tax break without treating the account like a long-term reserve.

If you have child care expenses

The dependent care FSA is a separate lever, and for some employees it matters more than the health FSA. The 2026 limit rises to $7,500, or $3,750 for married filing separately, which can be a meaningful benefit for parents balancing child care costs with work. That account does not replace a health FSA, but it can relieve pressure in a different part of the household budget.

For employees at monday.com who are comparing total family benefits rather than just medical spending, this is the number that can quietly decide the year. A household with child care costs may find the dependent care FSA more valuable than squeezing a few extra dollars into a medical FSA election.

The decision that protects your paycheck

The smartest move is not to chase the biggest tax shelter. It is to match the account to the rhythm of your life. If you want money that rolls forward with you, the HSA is the sturdier choice. If you want to pre-fund expected bills and use them during the plan year, the FSA can be the cleaner fit, as long as you respect the $3,400 cap and the $680 carryover ceiling.

For monday.com employees, that means open enrollment is less about picking a benefit and more about choosing where your medical dollars should live for the next 12 months. Get the time horizon wrong, and you leave value on the table. Get it right, and the account starts working like part of your compensation, not just another checkbox.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?