monday.com highlights SaaS growth playbook for sustainable expansion

monday.com’s growth playbook shows how retention, activation, and expansion now shape product, sales, and support decisions across the company.

By December 31, 2025, monday.com had more than 250,000 customers worldwide, and by March 31, 2026, 4,547 customers above $50,000 in annual recurring revenue. Once revenue comes from subscriptions, every team starts carrying part of the retention burden, from the first product click to the last renewal conversation.

Why SaaS changes the job across the company

Traditional software can celebrate the sale and move on. Subscription software has to win the sale, activate the customer quickly, keep usage sticky, and expand the account before churn erases the initial win. At monday.com, that system is built around low-cost acquisition, fast activation, retention, and coordinated growth motions across content, paid channels, product-led growth, and customer success.

Inside monday.com, the business is now much larger than a single work-management app. The company positions itself as an AI work platform, and that framing reflects how it sells across SMB, mid-market, and enterprise accounts. Engineers affect whether a new user understands the product in minutes or bounces before onboarding clicks. Product managers shape whether the workflow fits the job well enough to earn expansion. Sales teams depend on a clear ideal customer profile and message discipline to avoid wasting cycles on accounts that will never compound.

The metrics that actually govern the machine

Lifetime value, customer acquisition cost, activation, churn, net revenue retention, and expansion revenue are the metrics that govern whether growth is durable. If acquisition is cheap but activation is weak, the business leaks. If churn is high, growth becomes a treadmill. If expansion revenue is healthy, the company can grow even when new-logo sales slow.

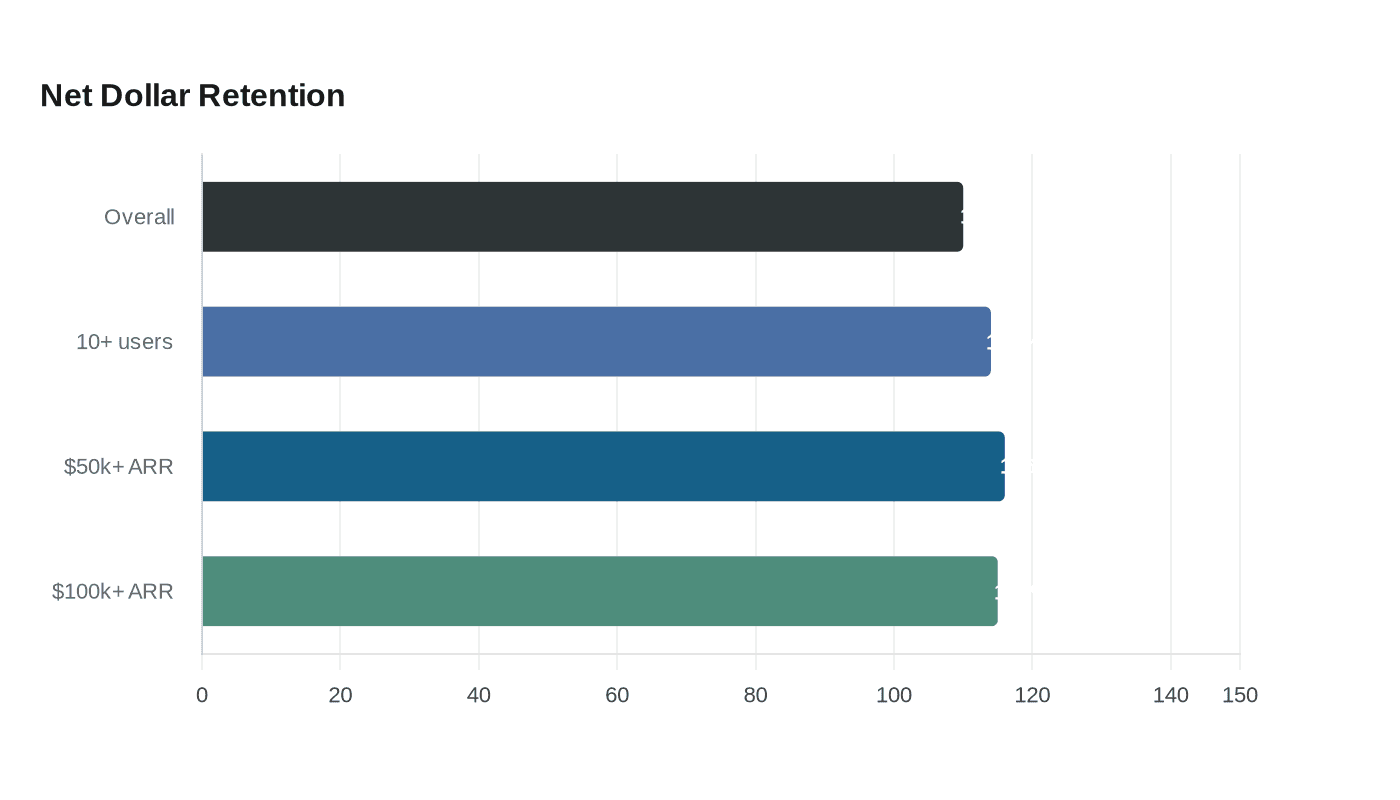

monday.com’s recent results put those mechanics in plain view. In the fourth quarter of 2025, the company reported revenue of $333.9 million, up 25% year over year. For the full year, revenue grew 27%, and non-GAAP operating margin reached 14%. In the first quarter of 2026, revenue rose to $351.3 million, up 24% year over year, while the company reported a 110% net dollar retention rate overall.

Retention was stronger in larger accounts. Net dollar retention reached 114% for customers with more than 10 users, 116% for customers with more than $50,000 in annual recurring revenue, and 115% for customers with more than $100,000 in annual recurring revenue.

What the customer base says about the platform shift

The company’s customer mix has also moved upmarket. monday.com had 65,016 paid customers with more than 10 users in Q1 2026, up 7% from 60,566 a year earlier. In its 2024 annual report, enterprise customers, defined as customers with more than $50,000 in annual recurring revenue, increased 39% from 2,295 at the end of 2023 to 3,201 at the end of 2024.

Larger customers tend to demand better onboarding, cleaner admin controls, stronger integrations, and more reliable workflows. They also create more room for expansion across teams.

From work management into multiple software categories

monday.com has spent the last few years widening that relationship. It launched monday dev in 2023, then monday service in 2025, pushing beyond work management into adjacent software categories. In 2025, it also introduced monday campaigns inside monday CRM, an AI-powered product meant to help marketers create, launch, and optimize campaigns tied directly to revenue.

By 2026, monday.com had moved to consumption-based pricing, and management tied AI growth to customer usage. For workers inside the company, that changes the internal math: more usage can create more revenue without relying solely on new seats, but it also raises the bar on product quality, usage measurement, and customer education.

If a customer can start in work management and then adopt CRM, service, or dev, the company gets more than a one-off transaction. It gets a system of interlocking workflows that can raise lifetime value and lower churn.

The company’s history helps explain the strategy

monday.com was founded in 2012 by Roy Mann, Eran Zinman, and Eran Kampf, began as an internal tool at Wix, launched commercially in 2014, rebranded from dapulse to monday.com in November 2017, and went public on Nasdaq in June 2021.

The same company that started with very small-budget social media ads bought Super Bowl advertising in 2022.

Why workers inside monday.com should care now

monday.com lists 3,211 employees on its investor relations page. These strategy shifts shape how engineers prioritize reliability and onboarding, how product managers think about workflow fit and retention, and how sales teams qualify accounts that can actually expand.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?