Cheesecake Factory beats first-quarter expectations as traffic improves

Traffic at Cheesecake Factory improved to minus 1.4% as sales rose 1.6%, giving managers more room to protect hours than weaker casual chains.

A better-than-expected quarter at The Cheesecake Factory offered a rare sign of stability in casual dining, where dining rooms have been under pressure and every percentage point of traffic matters to staffing. The chain said comparable restaurant sales rose 1.6% in the quarter ended March 31, while traffic was still down 1.4%, a clear improvement from the 4% decline it posted in the prior quarter.

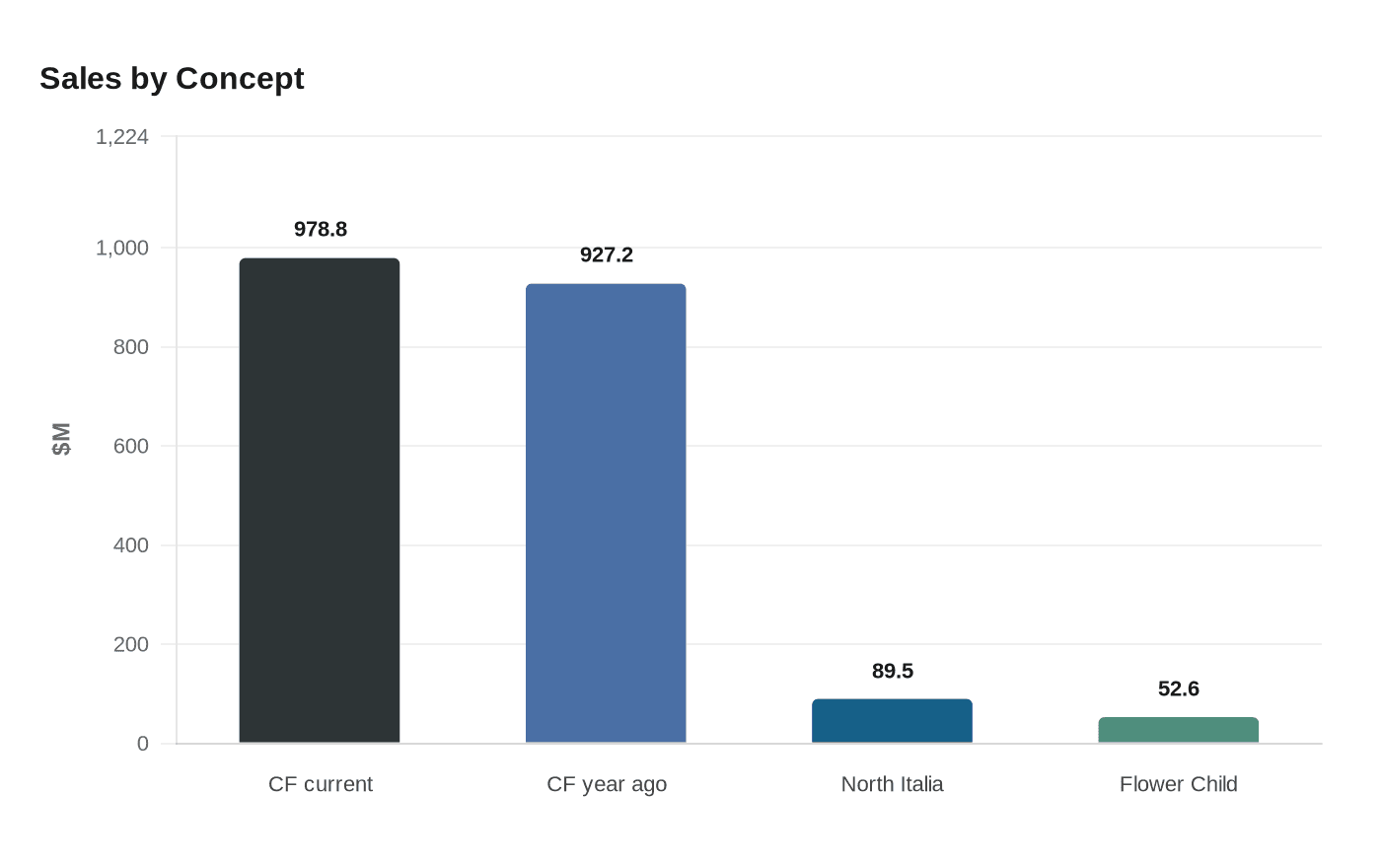

For restaurant workers, that combination matters more than the top-line headline. Cheesecake Factory said revenue reached $978.8 million, up from $927.2 million a year earlier, while adjusted diluted earnings per share came in at $1.05 and net income was $49.5 million. Chairman and CEO David Overton said the results were above expectations and reflected resilient demand, weather-related headwinds, and gains in labor productivity and food efficiency.

The traffic picture is the key operating signal. Same-store sales outpaced the Black Box casual-dining index by 40 basis points, helped by pricing that was up 3.3% even as mix slipped 0.3%. The company also said weather cut into results by 1.7%, which suggests some of the softness was external rather than purely a sign of weakening guest demand.

That matters inside the building. When traffic is falling, managers tend to trim labor more aggressively, compress schedules, and push harder on table turns and ticket times. A 1.4% traffic decline is still negative, but it is a much better place to be than a 4% slide. It gives operators more room to keep servers, hosts, bartenders, and line cooks on steadier shifts, especially when restaurant-level profit margin at the Cheesecake Factory brand held at 17.5%, up 10 basis points from a year earlier.

The brand’s scale also helps. Average annualized unit volume hit a record $12.8 million, and off-premise sales accounted for 22% of Cheesecake Factory sales, giving the chain a buffer beyond dine-in traffic. That mix can soften volatility for kitchen and service teams when in-house demand wobbles, though it also keeps pressure on execution as takeout and delivery compete with full-service dining room flow.

The quarter was also stronger than the same period last year, when comparable restaurant sales rose 1.0% and net income was $32.9 million. Other concepts helped, too: North Italia posted $89.5 million in sales, up 7%, while Flower Child sales rose 21% to $52.6 million, with comparable sales up 10%.

The company opened one North Italia, one Flower Child, one Fox Restaurant Concepts unit, and one Cheesecake Factory in Guadalajara, Mexico, during the quarter. It also repurchased about 332,000 shares for $19.2 million and ended with $601.6 million in available liquidity. For workers, the message is straightforward: Cheesecake Factory is not out of the woods, but it is moving in a direction that is likelier to support steadier schedules than the chains still stuck in deeper traffic losses.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?