Nearly All Restaurant Operators Struggling With Elevated Food Costs, Report Finds

95% of full-service operators cite food costs as their top challenge, with beef prices at multi-decade highs and egg supplies still recovering from the loss of 144 million birds.

Chad Moutray, chief economist for the National Restaurant Association, put it plainly in the association's 2026 State of the Restaurant Industry report: "Success for operators this year will hinge on their ability to get the math right in a still-challenging economic environment." The math, for most operators right now, is brutal.

Ninety-five percent of full-service restaurant operators and 94 percent of limited-service operators identified elevated food costs as their primary challenge, according to the report. Food costs industrywide have climbed 34 percent above pre-pandemic levels, a cumulative pressure that six years of price adjustments have not fully absorbed. Tariffs compounded the damage, with 68 percent of all operators reporting they contributed directly to higher food and beverage expenses; many of those costs stuck even after some reciprocal tariffs were rolled back.

The protein situation alone is enough to rewrite a menu. U.S. cattle inventories sit at multi-decade lows, and the NRA projects herd expansion will be slow enough to keep beef prices elevated through at least 2027. Pork offers little relief either, with any meaningful supply increase unlikely before 2027 due to a contracting breeding herd. Eggs are still recovering from the loss of more than 144 million birds to avian influenza since 2022, leaving supply below balanced levels. The late-2024 and early-2025 HPAI outbreak re-aggravated those losses just as the industry hoped for stabilization.

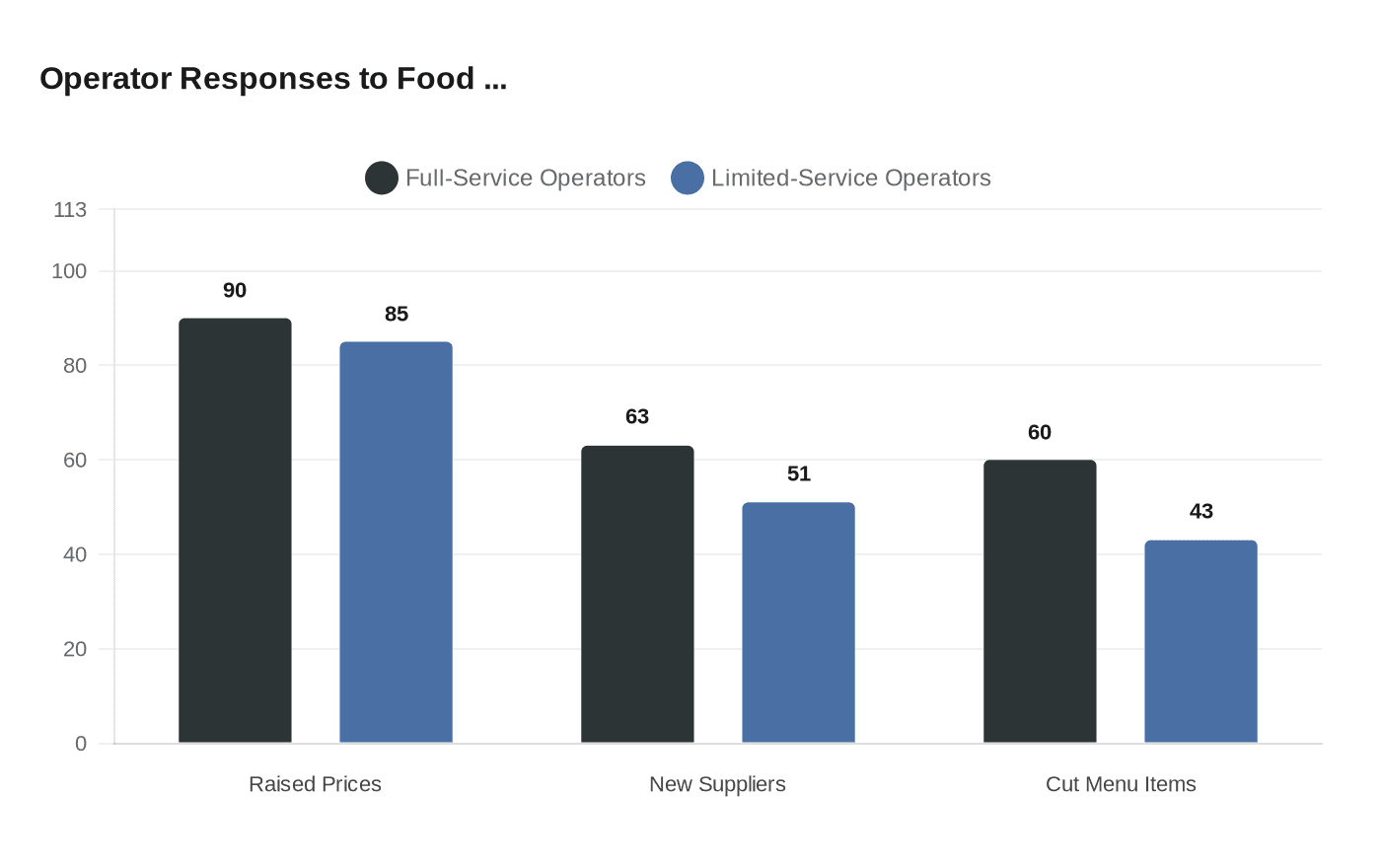

In response, operators have leaned hard on three levers. Among full-service operators, 90 percent raised menu prices, 63 percent switched to alternative suppliers, and 60 percent cut items from their menus entirely. Limited-service operators moved similarly: 85 percent increased prices, 51 percent sourced new vendors, and 43 percent reduced their offerings. A shorter menu is no longer just a design choice; it is a cost-control mechanism, eliminating the SKUs most exposed to volatile commodity prices and reducing the number of supplier relationships a kitchen has to manage.

The warning in the report is that many operators are nearing the ceiling on those adjustments. Raising prices further risks accelerating the traffic declines that already hit 60 percent of operators in 2025. That year, 42 percent of operators reported their restaurants were not profitable, a figure that points to how quickly squeezed margins translate to closed doors.

For any general manager walking staff through a cost conversation right now, the clearest framing is this: the beef, eggs, and pork on your line are likely to cost more, not less, through the end of 2027. The operators absorbing that most successfully are the ones who already shortened their menus, locked longer-term contracts where possible, and substituted toward proteins with better supply outlooks, like broiler chicken, where production is projected to increase modestly in 2026.

SUMMARY: 95% of full-service operators cite food costs as their top challenge, with beef at multi-decade supply lows and egg supplies still recovering from the loss of 144 million birds.

CONTENT:

Chad Moutray, chief economist for the National Restaurant Association, framed the year directly: "Success in 2026 will hinge on the ability of operators to get the math right in a still-challenging economic environment." For most operators right now, that math is brutal.

Ninety-five percent of full-service restaurant operators and 94 percent of limited-service operators identified elevated food costs as their primary challenge, according to the NRA's 2026 State of the Restaurant Industry report. Food costs alone have risen dramatically, currently sitting 34 percent above pre-pandemic levels. Tariffs compounded the damage, with 68 percent of all operators reporting they contributed directly to higher food and beverage expenses. Many businesses had already absorbed the added costs even after some reciprocal tariffs were lifted.

Beef is the most constrained protein category. U.S. cattle inventories are at multi-decade lows, and while 2026 may mark the bottom of the cattle cycle, herd expansion is expected to be slow, keeping prices elevated through at least 2027. Pork production is also limited by a contracting breeding herd, with any meaningful supply increases unlikely before 2027. Eggs remain below balanced supply levels, still recovering from losses exceeding 144 million birds to avian influenza since 2022. The late-2024 and early-2025 HPAI outbreak re-aggravated those losses just as the industry hoped for stabilization. Poultry offers the most optimism of the major proteins, with broiler production projected to increase modestly, though capacity constraints and the ongoing threat of avian flu could limit gains.

In response, operators have leaned hard on three levers. Among full-service operators, 90 percent raised menu prices, 63 percent switched to alternative suppliers, and 60 percent removed items from their menus entirely. Limited-service operators moved similarly: 85 percent increased prices, 51 percent sourced new vendors, and 43 percent reduced their offerings. A shorter menu is no longer just a design choice; it is a cost-control mechanism, eliminating the SKUs most exposed to volatile commodity prices and reducing the number of supplier relationships a kitchen has to actively manage.

Despite those efforts, many operators say they are limited in their ability to fully offset rising costs without risking customer traffic. More than 60 percent of operators reported traffic declines in 2025, with only 15 percent experiencing an increase, and 42 percent of all operators reported their restaurants were not profitable that year.

For any general manager walking staff through a cost conversation, the clearest framing is this: beef, eggs, and pork on your line are likely to cost more, not less, through the end of 2027. The operators absorbing that best are the ones who have already trimmed their menus, locked longer contracts where procurement allows, and shifted toward proteins with stronger supply outlooks. The window to get that math right is not widening.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?