Taco Bell faces limited relief as $38 billion swipe-fee settlement advances

A $38 billion swipe-fee deal won court backing, but the relief is tiny: a 0.1-point cut that still leaves Taco Bell operators squeezed on labor and promotions.

Taco Bell’s card-heavy, app-driven business runs through a payments system that still takes a meaningful bite out of every sale. A federal judge in Brooklyn gave preliminary approval to a revised $38 billion Visa-Mastercard settlement on June 9, but the deal would lower interchange fees by only 0.1 percentage point for five years, a change restaurant groups say barely dents a cost that keeps pressing on margins.

The case has been moving for nearly 20 years, after merchants filed the underlying interchange-fee class action in 2005 in the Eastern District of New York. A smaller $30 billion proposal was rejected in 2024 before the parties returned with a revised pact that now covers more than 12 million merchants. Visa said the agreement would cut the U.S. combined average effective credit interchange rate by 10 basis points for five years and cap standard U.S. consumer credit rates at 1.25% for the term of the deal.

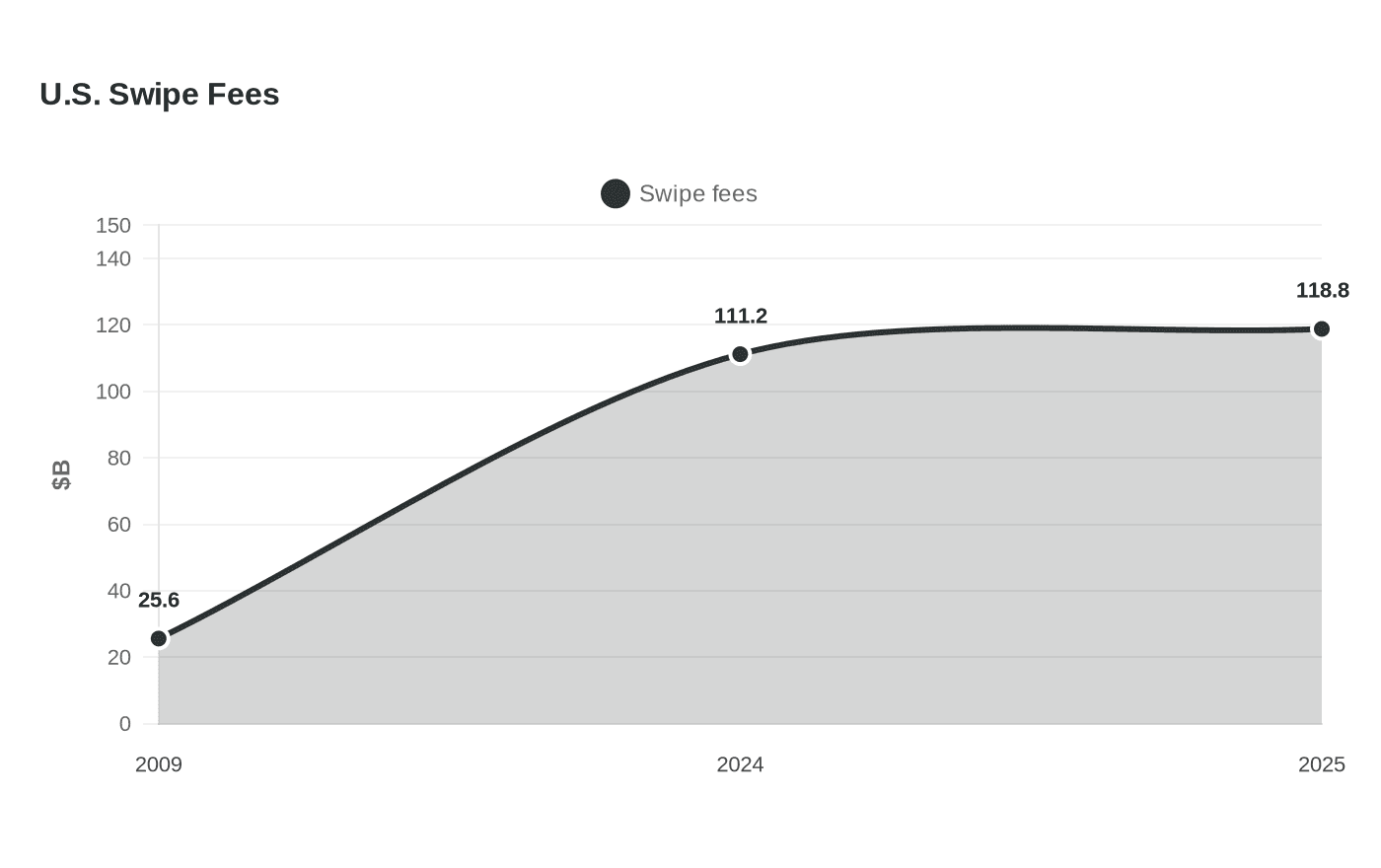

Restaurant operators are still arguing that the system remains too expensive. Industry reporting put U.S. swipe fees at $118.8 billion in 2025, up from $111.2 billion in 2024 and $25.6 billion in 2009, with an average fee of 2.36%. Reuters has reported that swipe fees typically run about 2% to 2.5%, which is why a 0.1-point reduction reads more like a trim than structural relief for chains trying to protect margins on low-ticket orders.

That matters at Taco Bell because the chain leans hard on promotions, rewards and app-based ordering, where every digital transaction compounds the cost pressure. Taco Bell said in March 2025 it projected 8% U.S. same-store sales growth and reported 8,757 restaurants across 25 countries. Its parent, Yum! Brands, said it operated 63,000-plus restaurants through about 1,500 franchisees across 155-plus countries and territories, showing how quickly payment costs can ripple through a system that depends on thousands of local operators making day-to-day labor and spending decisions.

For crew members and shift managers, the connection is not abstract. When card-processing costs keep climbing, franchisees often look for savings where they can find them: tighter labor budgets, leaner scheduling, stricter throughput targets, more pressure to move digital orders, and less room for error on food waste and service times. Taco Bell’s push into rewards, app offers and Voice AI at U.S. drive-thrus in 2024 makes those margins even more sensitive. The settlement may bring some certainty to the payments side, but for stores trying to hit sales goals, it leaves the basic economics largely intact.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip