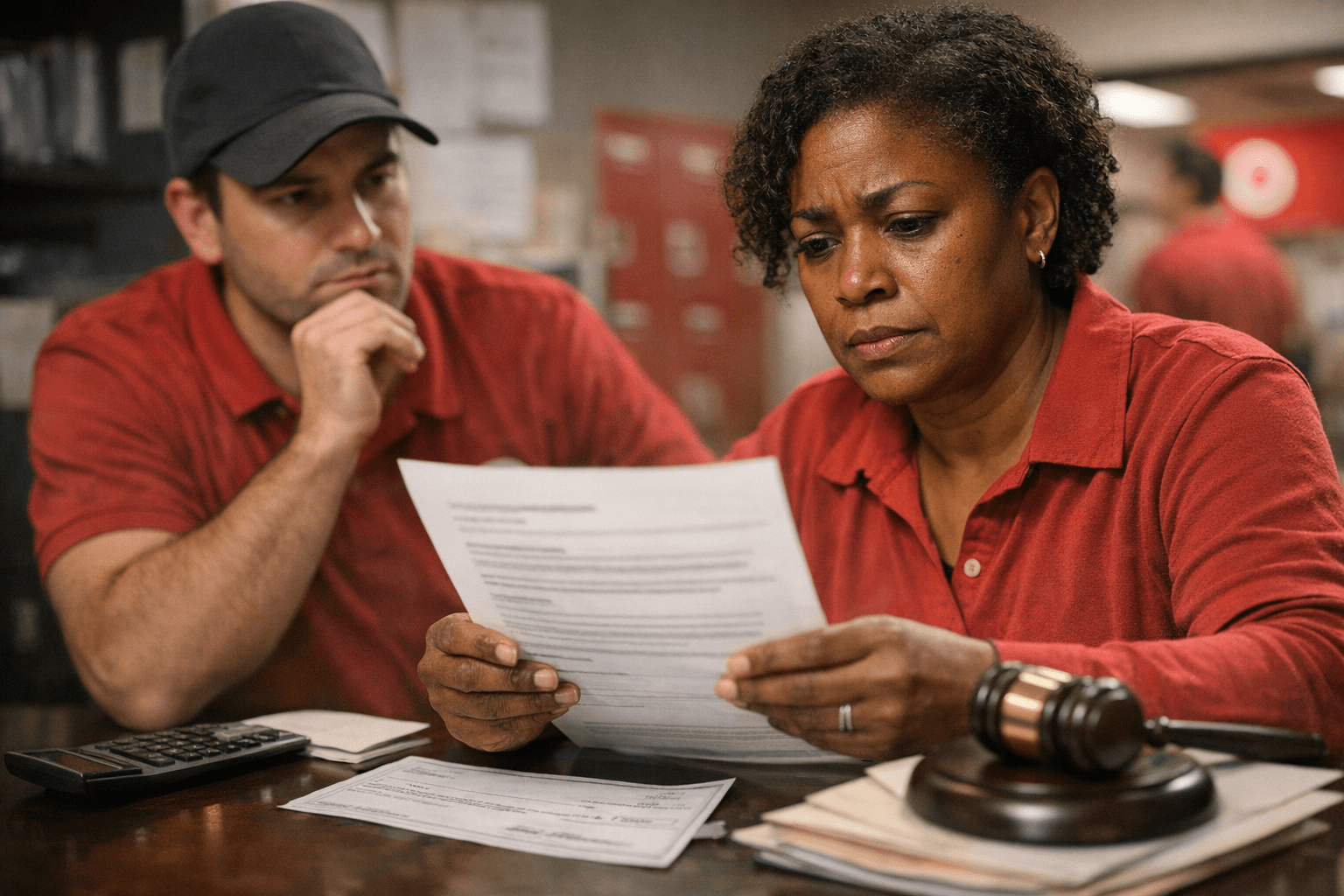

What Target Employees Should Know About Payroll-Based Class Settlement

Workers named in the Sadler v. Target payroll-based class settlement should verify their status with the settlement administrator and act before listed deadlines to preserve rights or object. The settlement affects how payments are issued and taxed, and accurate contact information and documentation will determine whether affected employees receive the correct payment.

Employees identified in the Sadler v. Target payroll-based class settlement should check their status with the court-appointed settlement administrator, Epiq, and make sure their mailing address and contact details are up to date. Settlement administrator web pages contain case documents, frequently asked questions and contact information; using the administrator’s phone or email to confirm placement on the class list is the fastest way to resolve questions about eligibility and payment timing.

Deadlines in the settlement notice are consequential. If you want to opt out or formally object to the terms you must follow the exact exclusion and objection procedures by the deadline stated in the notice. If you do nothing you will normally receive an automatic payment but you will also give up the right to sue separately on the same claim. For that reason, employees who are unsure whether to accept the payment or challenge the calculation should study the notice carefully and act before the cutoff dates.

Tax treatment can affect actual take-home amounts. Settlement payments often separate wage and non-wage components, which are reported differently for tax purposes (for example W-2 versus 1099 forms). The settlement documents typically explain the anticipated tax handling; employees with questions about how a payout will affect withholding or tax filings should consult a tax advisor for personalized guidance.

If you do not receive a notice but believe you worked for Target during the class period, contact the settlement administrator and keep records proving your employment. Pay stubs, W-2s and other payroll documents are the primary evidence used to confirm eligibility when settlements are based on payroll records. The administrator can confirm eligibility and outline next steps for missing or incorrect notices.

For disputes over eligibility, payment calculations or procedural questions, the settlement notice should list class counsel contact details. Employees can contact class counsel or seek independent employment-law counsel to evaluate options. Consumer protection organizations and state wage agencies can also offer guidance about class-action procedures and rights under wage laws.

Taking these practical steps now, verifying identity with Epiq, meeting deadlines, preserving payroll records and consulting appropriate counsel or tax professionals, will help named employees understand their options and protect their financial and legal interests in the Sadler v. Target settlement.

Know something we missed? Have a correction or additional information?

Submit a Tip