Walmart releases 2026 benefits book with new coverage dates, 401(k) details

Walmart’s 2026 benefits book locks in new effective dates for health, 401(k), and stock plans, while PPTO rules still drive the biggest attendance mistakes.

What the 2026 benefits book actually changes

Walmart’s new Associate Benefits Book is the clearest roadmap yet for medical coverage, pharmacy, dental, vision, disability, life insurance, COBRA, the 401(k), and the Associate Stock Purchase Plan. Most benefits take effect January 1, 2026, but the 401(k) starts February 1 and the stock purchase plan follows on April 1, giving associates three different coverage dates to track.

That matters because the book is not just a brochure. It is the consolidated source for the Summary Plan Descriptions for the Associates’ Health and Welfare Plan and the Walmart 401(k) Plan, with the stock purchase prospectus included as well. Walmart also reminds associates that every benefit still comes with eligibility rules, premiums, limitations, and exclusions, so the fine print still controls what a worker can actually use.

Health coverage, virtual care, and the cost question

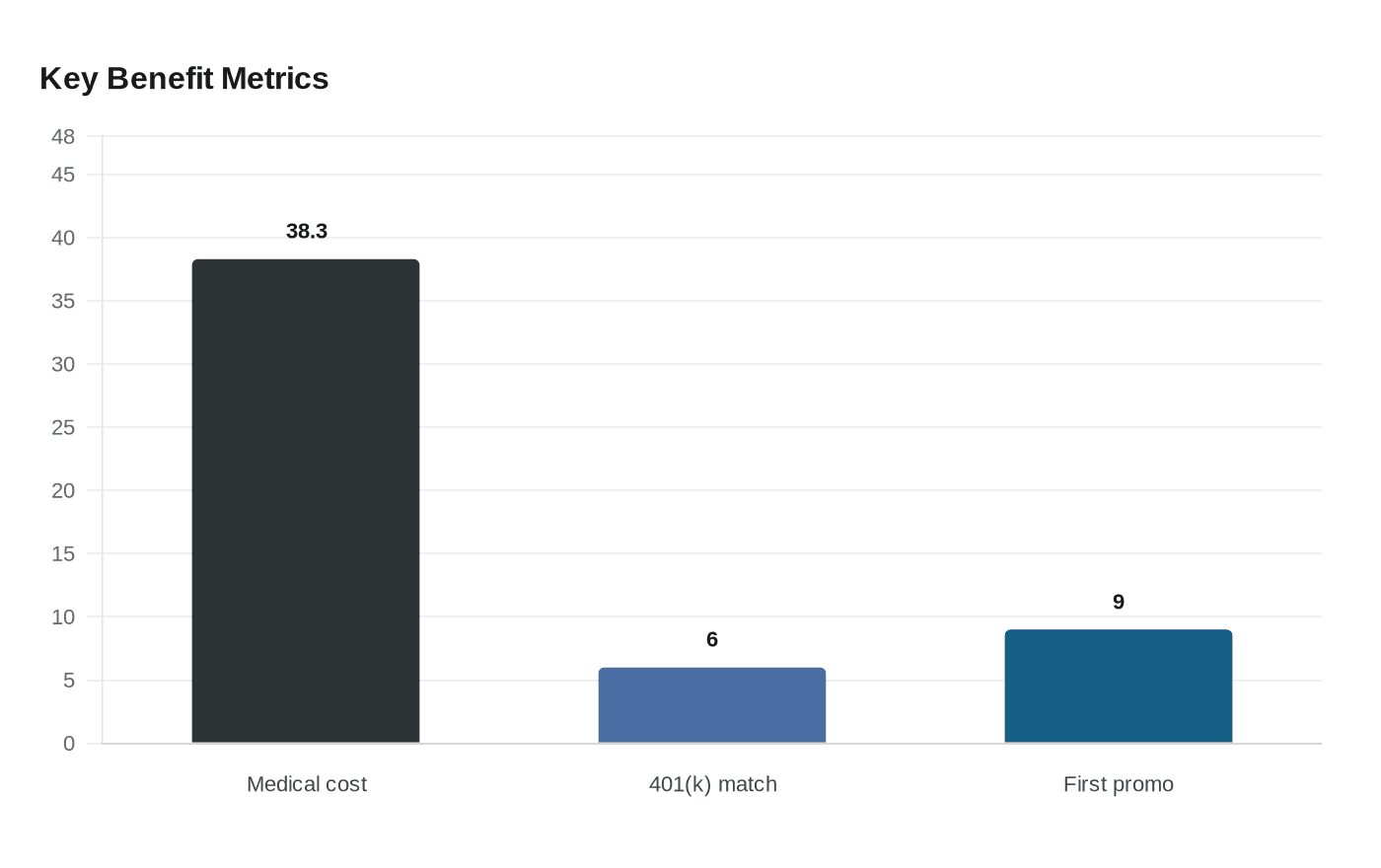

For hourly workers trying to figure out whether coverage is worth it, the headline number is the entry price: eligible full-time and part-time associates can access medical coverage starting at $38.30 per biweekly pay period. That price point sits alongside a broader package that includes pharmacy, dental, vision, disability, life insurance, and COBRA information in the same guide.

Walmart is also pushing a practical benefit that has immediate day-to-day value: associates enrolled in most medical plans can get no-cost virtual primary care, urgent care, and mental health care through Doctor On Demand by Included Health. For a worker juggling shifting hours, daycare, school schedules, or a second job, that kind of access can be the difference between getting care and skipping it until a problem gets worse.

The 401(k) timing workers need to watch

The 401(k) is one of the biggest details buried in the new book because its effective date is different from the rest of the benefits package. The plan becomes effective February 1, 2026, not January 1, and Walmart says associates can contribute at any time.

Once someone is match-eligible, Walmart matches each dollar contributed up to 6% of eligible pay. That is the number that should matter to associates trying to stretch every paycheck, because it turns the 401(k) into more than a retirement deduction. It is also part of Walmart’s broader message that pay, benefits, and advancement are tied together, especially as the company says many benefits start on day one and that U.S. associates receive their first promotion in nine months, on average.

The stock purchase plan comes later

The Associate Stock Purchase Plan has its own effective date: April 1, 2026. That separate start date is easy to miss if a worker assumes all benefits kick in at once, which is exactly why the book lays out different dates by plan.

For associates who buy Walmart stock through payroll deductions, that date matters because it sets when the new-year version of the plan becomes active. The company includes the prospectus in the book, signaling that this is meant to be a working reference, not just a summary for HR shelves.

PPTO is still the attendance rule most associates get wrong

The biggest operational issue for hourly workers remains Protected PTO, not medical coverage. Walmart’s PPTO FAQs say hourly field associates and hourly campus/corporate associates in locations with local paid sick leave laws earn time in two separate buckets: regular PTO and Protected PTO. In those locations, PPTO is Walmart’s way of providing paid sick leave even where local law does not require it.

The key distinction is simple but easy to mishandle: PPTO protects an absence from attendance points when enough time is used to satisfy the Attendance Policy. That means the attendance system is not just about whether you are paid. It is about whether the shift is marked as protected, which is why workers can get tripped up by using the wrong bucket or using too little time.

How PPTO works when you are sick, late, or miss a shift

Walmart says associates can use PPTO for unexpected absences, which is the most common use. Full-time and part-time associates can also use it for a planned absence if they do not have regular PTO available. Temporary associates have narrower rules, limited to covered sick, family-care, or paid-leave reasons.

The company’s manager guidance makes the real-world examples even clearer: missed shifts, tardy or late-ins, and early-outs can all fall under the PPTO rules if enough PPTO is used to satisfy the Attendance Policy. Associates can request PPTO in the GTA system, and documentation is not required when PPTO is used. That last point is important because it makes PPTO less cumbersome than many leave processes, but only if the associate uses it correctly and reports the absence properly.

The costly mistakes: no-call/no-show and uncovered time

The part that still trips people up is what happens when the process is only partly followed. Failing to report an absence can trigger no-call/no-show points, which means even a valid reason for being away from work can turn into an attendance problem if the shift is not reported correctly.

Walmart’s older Protected PTO guides reinforce the same warning: if an associate does not have enough Protected PTO to cover the full absence, regular PTO may pay the remainder, but any portion not covered by Protected PTO can still lead to an attendance occurrence under the location’s policy. In plain terms, pay and protection are not always the same thing. A shift can be partially paid and still count against attendance.

Why this benefits book matters now

Walmart has spent years telling workers that it is investing in wages and career movement, saying hourly pay has risen by around 30% over the past five years and that the U.S. average hourly wage is now close to $18. Against that backdrop, the 2026 benefits book is part of a larger package the company uses to sell stability, not just hourly pay.

For associates, the practical takeaway is narrower and more urgent: know the three coverage dates, know which bucket your PTO lives in, and know when PPTO protects an absence from points. In a store where attendance can affect both pay and standing, the difference between regular PTO, PPTO, and a no-call/no-show is the difference between a covered day and a policy problem.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip