Walmart Releases 2026 Benefits Rates, Revealing Biweekly Costs Across All Medical Plans

The Premier PPO starts at $38.30 biweekly (under $1,000 a year), but a tobacco-user surcharge on a family plan can add more than $5,600 annually to your deductions.

Walmart's published 2026 Benefits Rates document sets concrete payroll deduction schedules across four plan options, and the gap between the cheapest associate-only tier and a family plan carrying two tobacco-user surcharges now runs more than $14,800 per year. For any associate still cross-referencing paystub deductions against expected coverage, the numbers below are the foundation.

The Premier PPO is the lowest-cost national option, pegged at $38.30 per biweekly period for associate-only, tobacco-free enrollment. Across 26 pay periods, that comes to $995.80 annually, and Walmart has noted the figure runs roughly one-third below the average national-company premium. The Saver HSA runs $42.80 biweekly for associate-only coverage, or $1,112.80 for the year. That $117 annual difference looks modest, but the Saver HSA carries a matching contribution from Walmart: $350 deposited into a HealthEquity HSA for associates covering only themselves, and $700 for those adding dependents. An associate who opens the account and contributes anything through payroll deductions effectively closes that gap and then some. The 2026 IRS contribution ceiling is $4,400 for individual HSA coverage and $8,750 for family, both inclusive of Walmart's match.

The Contribution HRA operates at a higher premium tier and includes $250 in annual Walmart dollars for self-only enrollees or $500 for those covering dependents; those dollars pay down eligible medical expenses automatically until exhausted. Associates in California, Kentucky, Louisiana, Mississippi, New Jersey, Tennessee, Washington, and West Virginia should flag this now: the Contribution HRA is being discontinued in those eight states at the end of 2026, and any remaining HRA balance will be forfeited on January 1, 2027.

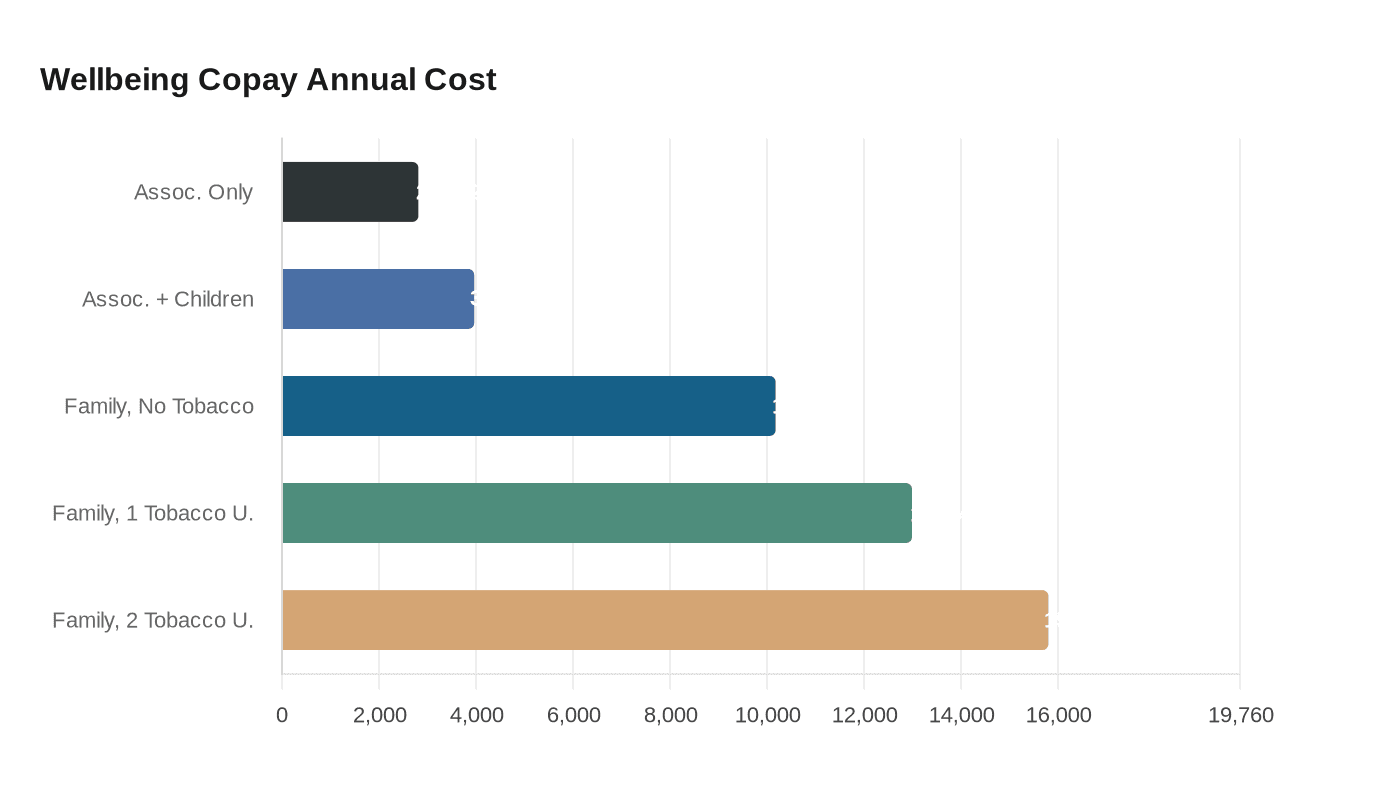

In those same eight states, associates have access to the Personalized Wellbeing Copay plan, where rates run significantly higher. Associate-only tobacco-free enrollment costs $108.20 biweekly, or $2,813.20 annually. Add children and the tobacco-free rate climbs to $152.50 biweekly ($3,965 per year); full family coverage without any tobacco users comes to $391.60 biweekly, or $10,181.60 annually. The tobacco-user surcharge is where deductions can spike sharply: one tobacco user on a family plan pushes the biweekly charge to $499.80 ($12,994.80 per year), and two tobacco users bring it to $608.00 biweekly, totaling $15,808 for the year. That is $5,626.40 more per year than the tobacco-free family rate for the same plan.

California associates also have the Health Net Salud Y Mas option, starting at $70.60 biweekly for associate-only coverage and scaling to $275.90 for associate plus spouse or partner.

Before assuming your deductions are correct, verify four things: first, confirm the coverage tier on your paystub matches what you actually enrolled in (associate-only, plus spouse/partner, plus children, or full family); second, check whether any enrolled dependent is coded as a tobacco user, since the surcharge applies per user; third, if you are in the Saver HSA, confirm your HSA is open through HealthEquity and that you are making payroll contributions to trigger Walmart's match; and fourth, check your plan name, because Walmart renamed all three national plans this year. The former Premier is now the Premier PPO, the former Saver is now the Saver HSA, and the former Contribution Plan is now the Contribution HRA. Aetna is no longer the third-party administrator for any Walmart medical plan; if your plan ID card still shows Aetna, contact People Services at 1-800-421-1362.

For plan selection, the Premier PPO favors associates who want predictable flat copays, starting at $35 per visit, with no need to manage a savings account. The Saver HSA is the stronger financial vehicle for generally healthy associates or those who want to build a tax-advantaged balance they keep even after leaving the company. Any associate expecting heavy prescription usage should pull the Summary of Benefits and Coverage document for each plan under consideration at One.Walmart.com/Benefits before locking in a choice, since formularies and out-of-pocket maximums vary enough to change the math considerably.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?