Walmart's 46x Earnings Multiple Draws Scrutiny Compared to Amazon's 28x

Walmart trades at a 46x trailing P/E while Amazon sits at 28x, yet Walmart's Q4 net income fell 19% and FY27 guidance missed Wall Street's growth target.

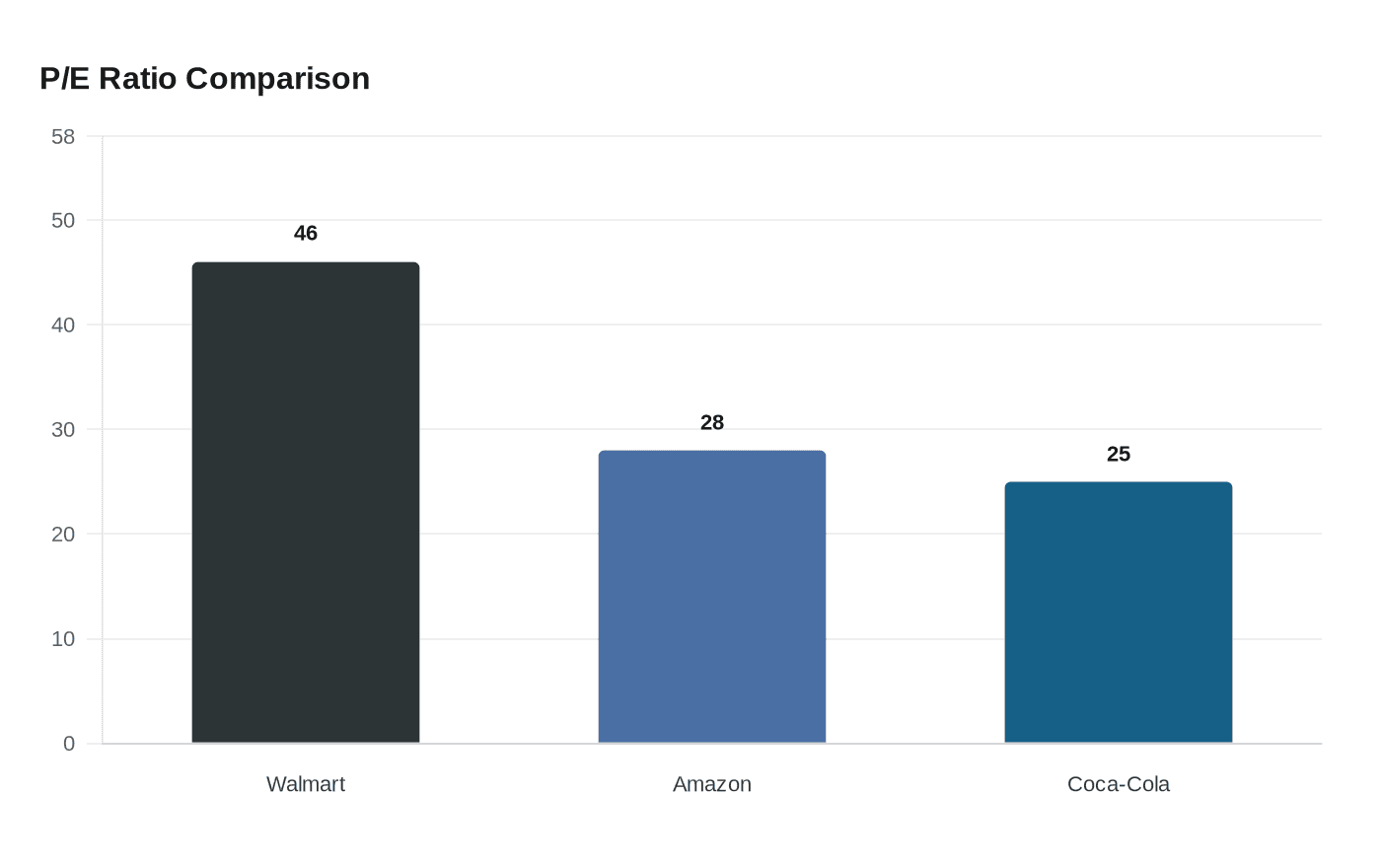

Walmart is priced like a tech company but generating margins that look nothing like one. The stock's trailing price-to-earnings ratio sits at roughly 46x, a figure that has drawn pointed scrutiny from investors and analysts who note that Amazon, with its enormously profitable AWS cloud division, trades at a comparatively modest 28x. The gap has become one of the more debated valuation questions in retail investing, with the disconnect sharpening after Walmart's latest quarterly results delivered a mixed picture.

On the surface, the Q4 numbers looked solid. Walmart posted adjusted EPS of $0.74, beating the consensus estimate of $0.70, on revenue of $190.66 billion. The underlying business is genuinely shifting: e-commerce now accounts for 23% of Walmart U.S. net sales, the global advertising business hit nearly $6.4 billion, and store-fulfilled expedited delivery grew more than 60%. CEO John Furner framed it as a transformation in progress: "The pace of change in retail is accelerating. It's exciting. And our financial results show that we're not only embracing this change, we're leading it."

But dig a layer deeper and the bear case sharpens quickly. Q4 net income fell 19% year-over-year even as revenue grew. Profit margin on $713 billion in trailing revenue sits at roughly 4.8%. FY27 net sales growth was guided to 3.5% to 4.5%, missing Wall Street's roughly 5% expectation. That combination, a growth-stock multiple attached to a slowing-growth, thin-margin retailer without a cloud business, is precisely what critics have seized on. The central question is whether Walmart's advertising flywheel and e-commerce momentum can structurally re-rate the business, or whether the multiple is simply running ahead of the fundamentals.

The skepticism has found a vocal home on Reddit, where a thread titled "Someone fucking explain why Walmart ($WMT) is at 47x earnings?" accumulated 1,471 upvotes and 518 comments. One poster drew an unflattering comparison to Coca-Cola, arguing the beverage giant offers "similar growth, better brand, international growth potential and a 25x PE." The r/investing community has also flagged a "150-day tariff clock" with implications for July, pointing to mounting trade policy exposure that could squeeze free cash flow further. Walmart already absorbed $26.6 billion in capital expenditures, a figure that has left free cash flow little room to absorb additional cost pressure.

Wall Street's professional analyst community sees the story differently. Thirty-nine analysts carry buy or strong-buy ratings on the stock versus just one sell, with a consensus price target of $135.90, implying roughly 10% upside from current levels. The bull case centers on the advertising revenue trajectory, the upper-income customer gains Walmart has made, and the argument that its e-commerce and fulfillment infrastructure is building a durable competitive moat.

The Amazon comparison cuts to the heart of the debate. Amazon's lower multiple is notable precisely because Amazon has AWS, a cloud business that generates operating margins that dwarf anything in retail. For Walmart to justify trading at a higher multiple than Amazon, investors effectively need to believe that the $6.4 billion advertising business, e-commerce growth, and logistics buildout will compound into something that changes Walmart's fundamental earnings quality. The $26.6 billion capex burden and tariff uncertainty make that a harder argument to sustain in the near term.

Know something we missed? Have a correction or additional information?

Submit a Tip