Estée Lauder Eyes Puig Deal, Adding Gaultier and Paco Rabanne

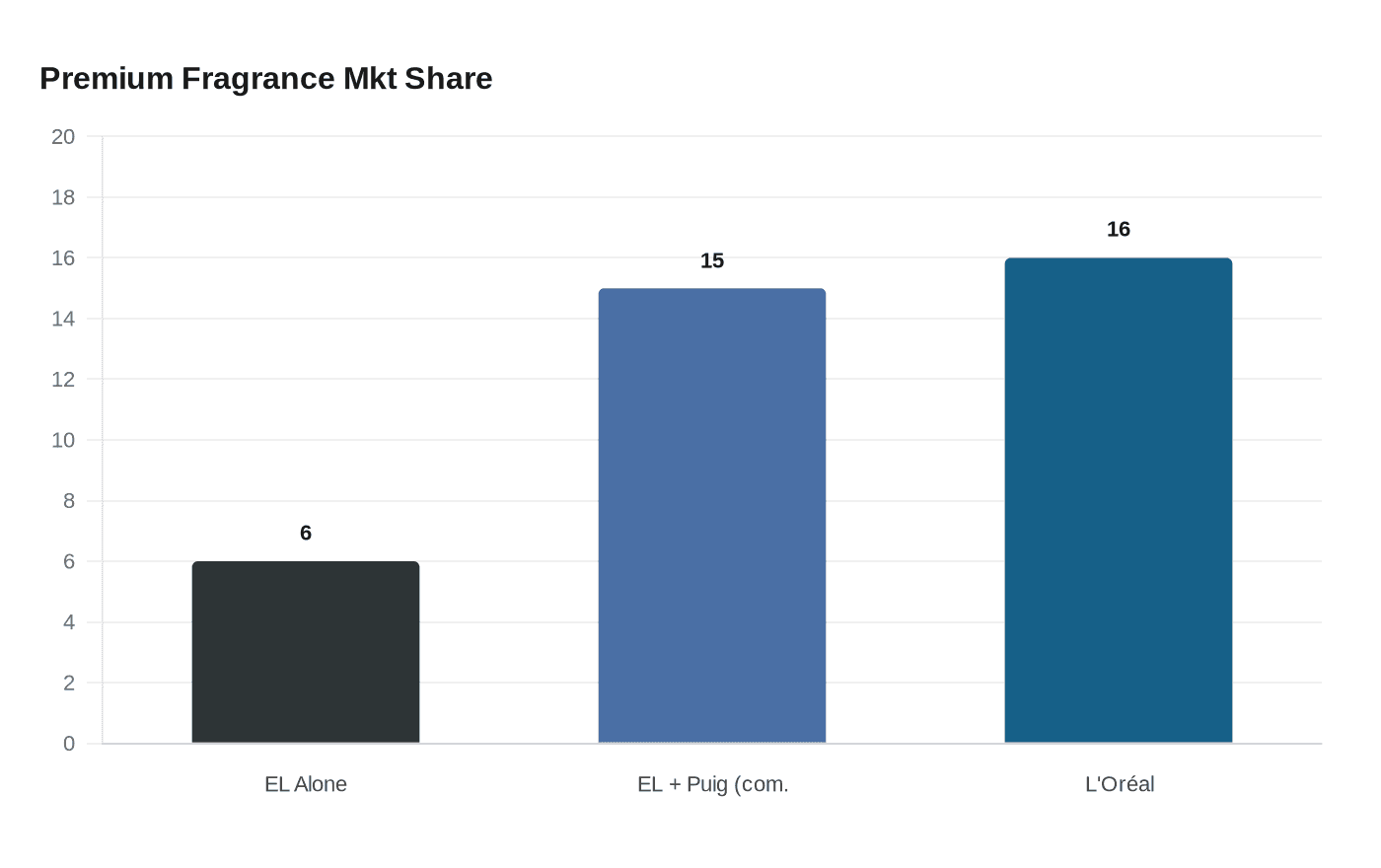

A potential Estée Lauder-Puig merger would lift the American giant's premium fragrance share from 6% to 15%, narrowing L'Oréal's 16% lead, yet its own stock fell 7.75% on the news.

The fragrance licensing game has fundamentally shifted, and Estée Lauder's confirmation on March 23 that it was in talks to acquire Spain's Puig Brands SA exposed exactly how much catching up the American beauty giant needs to do. A deal that would push a combined entity's global premium fragrance market share from 6% to 15%, landing one point behind L'Oréal's 16% according to Morningstar analysts, is less a statement of ambition than an acknowledgment of structural necessity.

Puig, the Barcelona-based group founded in 1914, controls one of the most strategically significant brand collections in global beauty, and critically, it owns its marquee names rather than merely licensing them. Carolina Herrera, Paco Rabanne and Jean Paul Gaultier each generate sales approaching $1 billion. Charlotte Tilbury, acquired in 2020, is expanding aggressively. Byredo, Dries Van Noten, Nina Ricci and Penhaligon's fill out a portfolio that recorded net sales of $4.7 billion in 2023. Xavier Brun, portfolio manager at Trea Asset Management in Barcelona, put the structural logic plainly: "Carolina Herrera, Paco Rabanne and Jean Paul Gaultier are each close to a billion in sales, they're world-recognised, so you can leverage that, plus they bought Charlotte Tilbury which is expanding."

That ownership structure, not merely the brand names, is what Estée Lauder is really acquiring. A licensing arrangement gives a beauty conglomerate the right to produce scents under a designer's name, but the designer holds the renewal card. Owning the brand changes every downstream conversation, from retailer shelf allocation and celebrity scent deals to product architecture decisions such as refillable formats and ingredient sourcing, commitments that require a single P&L rather than a negotiated contract. Puig has been steadily building exactly this kind of structural control, having shed major licenses years ago in favor of brands it owns outright, and its formalized sustainability program reflects how deeply that ownership model runs.

The competitive pressure behind the talks is hardly subtle. L'Oréal's $4.6 billion acquisition of Kering's beauty business handed the French group exclusive development rights for fragrances under Gucci, Bottega Veneta and Balenciaga, alongside the Creed line. For Estée Lauder, sitting at a 6% premium fragrance share, a proportionate response was overdue. A combination with Puig would produce a beauty group valued at roughly $40 billion with approximately $20 billion in annual sales, Jefferies analyst Sydney Wagner estimated, shifting the new entity's portfolio balance to 38% skincare, 34% fragrance, 26% makeup and 3% hair.

Markets registered the news as a double-edged development. Puig's shares surged 13% in Madrid following the disclosure, though the stock remained below its €24.50 listing price, trading around €17. Estée Lauder fell 7.75% on the New York Stock Exchange on March 23, with losses deepening to roughly 17% across the two-day period, reflecting investor unease about the scale and timing of a potential $10 billion-plus acquisition. Estée Lauder posted a $1.13 billion loss in fiscal 2025, has announced plans to cut up to 7,000 jobs, more than 11% of its workforce, and is midway through a restructuring it calls "Beauty Reimagined." Barclays analyst Lauren Lieberman was pointed: "While likely financially accretive to [Estée Lauder], we believe the potential acquisition of Puig would be dilutive to the company's Beauty Reimagined turnaround strategy."

Both companies confirmed the discussions but stated no agreement had been reached and no final terms set. As of April 1, the negotiations had advanced toward a deal consisting mostly of stock that could be formally announced within weeks. Marc Puig, who built the group into a global force, stepped back from the CEO role to concentrate on the combination. The underlying category argument is hard to dismiss: U.S. prestige fragrance grew 5% by value last year and finished as the second-largest segment in prestige retail according to Circana data. Whether that growth trajectory is enough to justify the integration complexity of merging two iconic but very different beauty dynasties is the question neither balance sheet alone can answer.

Know something we missed? Have a correction or additional information?

Submit a Tip