EU Omnibus Directive Reshapes Sustainability Reporting Rules for Fashion Brands

EU Directive 2026/470 cuts CSRD scope by 90%, but fashion giants like LVMH and Inditex with 1,000+ staff still face mandatory sustainability disclosure from 2028.

The EU's Omnibus I Directive didn't just trim the paperwork. It fundamentally restructured which fashion brands owe consumers any answers at all about what happens inside their supply chains.

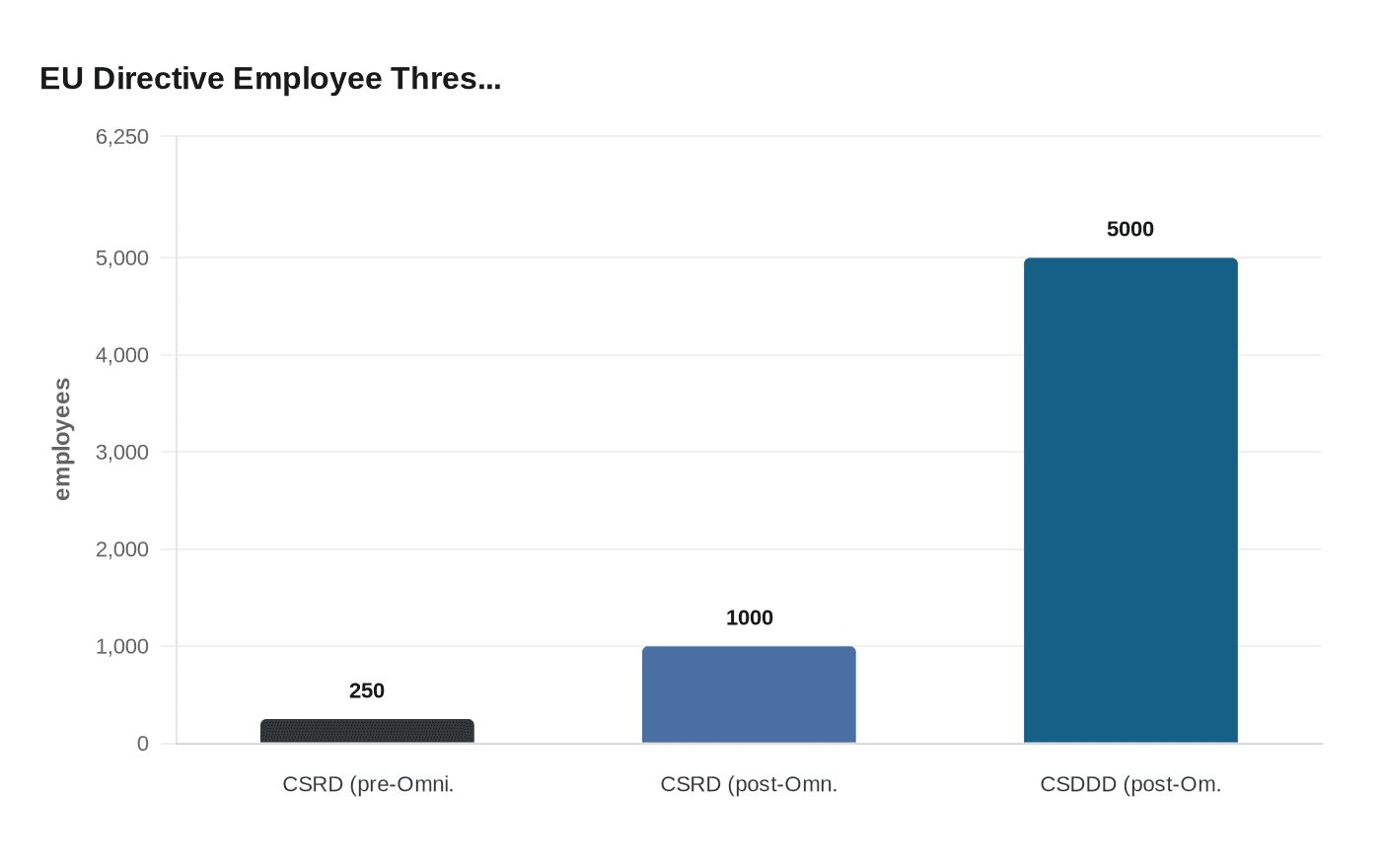

Directive (EU) 2026/470, published in the EU's Official Journal on February 26 and in force since March 18, significantly simplifies corporate sustainability reporting and due diligence requirements. The combined effect is a dramatic narrowing of scope. The final omnibus deal reduces the CSRD scope by 90%, raising the employee threshold from the original 250 to 1,000 full-time employees and setting a net turnover floor of €450 million. For CSDDD due-diligence obligations, the turnover threshold has been raised to €1.5 billion and the employee threshold to 5,000 workers. This leaves roughly 1,600 companies across the EU in scope for due-diligence obligations.

That threshold distinction matters enormously when scanning a brand's sustainability page and trying to figure out whether their claims are backed by mandated disclosure or marketing copy. Groups like LVMH, Inditex (whose portfolio runs from Zara to Massimo Dutti and Bershka), and Hennes & Mauritz are large enough to remain in scope on both counts. Companies already required to report under the CSRD for financial years starting in 2024, the so-called Wave 1 companies, but that no longer meet the revised thresholds shall be out of scope for financial years 2025 and 2026, subject to national transposition. Mid-sized European labels and most independent brands are effectively off the regulatory hook.

The timeline has also shifted significantly. Member states are required to transpose the directive's provisions related to the CSRD by March 19, 2027, and those related to the CSDDD by July 26, 2028. CSDDD due diligence is limited to very large companies and its application is deferred until July 2029, a structural shift rather than simply stop-the-clock timing relief. For most fashion companies still in scope, the first CSRD-aligned sustainability reports, covering financial year 2027, won't appear until 2028.

What actually changes on those reports is equally significant. The draft simplified European Sustainability Reporting Standards (ESRS) were published in December 2025, and the Commission will adopt a final version within six months. These amended standards cut mandatory data points by 61% in response to the Omnibus package. The Omnibus Directive also eliminates the requirement for sector-specific ESRS standards, meaning the granular textile-specific requirements on fiber sourcing, chemical use, and Scope 3 emissions that advocates pushed for will not materialize.

Climate transition plans have been fully removed as an implementation duty from the CSDDD. However, companies in scope of CSRD must still publish information on their climate transition plans, or in their absence, state whether and when they intend to adopt one. The legal obligation to actually execute the plan is gone. The due-diligence framework, however, reintroduces a full risk-based approach to the value chain, making companies address impacts where they occur, while adding stricter restrictions on information requests to smaller suppliers.

Companies with 1,000 employees or fewer are no longer bound to provide information to reporting companies that go beyond the scope of voluntary standards, with the Commission set to develop the content of those standards by July 19, 2026. That provision creates a structural blind spot: a luxury conglomerate or fast-fashion giant can now face limits on how deeply it demands transparency from its own Tier 2 or Tier 3 suppliers.

For consumers who want to distinguish genuine accountability from glossy sustainability theater, the watchlist is now more targeted but no less useful. For CSRD-covered brands, the mandatory quantitative data on Scope 1, 2, and 3 emissions remains in play, alongside labor standards metrics and water and waste figures, even without sector-specific ESRS. The climate transition plan disclosure is the document to watch: if a brand says it has no plan and no timeline, that is now a legally permissible omission rather than a red flag. For CSDDD-covered groups, the annual due-diligence statement is the key document, mapping actual or potential adverse human rights and environmental impacts across the supply chain.

The Omnibus I Directive did not make greenwashing easier for the brands that remain in scope. It reduced the number of brands required to answer for it at all, and that is a distinction worth holding onto the next time a smaller label talks about its values without being required to prove them.

Know something we missed? Have a correction or additional information?

Submit a Tip