LVMH Suffers Record 28% Quarterly Plunge, Rattling the Luxury Sector

Bernard Arnault lost more than $55 billion in a single quarter as LVMH shares fell 28%, the group's worst performance since its 1989 IPO.

Bernard Arnault's personal fortune contracted by more than $55 billion between January and March. That figure tracks precisely with what LVMH's share price did over Q1 2026: a fall of 28.2%, the steepest recorded since the group went public in 1989. The drop performed worse than the burst of the dot-com bubble in 2001, the 2008 financial crisis, and even the lockdown shock of 2020.

Bloomberg analysts Angelina Rascouet and Levin Stamm mapped the decline against every comparable crisis in LVMH's history, noting that cautious forward-looking signals from the group's leadership earlier in 2026 had already primed investors for a rough quarter. The selloff pushed LVMH's valuation to roughly a 20% discount versus luxury peers and below approximately 20x expected next-12-month earnings, a level the market had long treated as a structural floor.

Two forces drove the repricing. A deterioration in global travel and tourism cut directly into the group's highest-priced transactions, while the Middle East conflict amplified broader macroeconomic anxiety: rising energy costs, slowing growth, and consumers watching disposable income compress in key markets. Wines and spirits, including Hennessy cognac, faced particular headwinds from reduced premium liquor consumption. LVMH's own January shareholder letter had already flagged the pressure, acknowledging weaker demand for cognac even while noting revenue stability in champagne and wines.

The Q1 revenue results confirmed the picture. The fashion and leather goods division saw revenue fall 4%, while beauty and spirits remain the categories most exposed to tariff disruption. The group has signaled it may consider price increases to defend margins, a familiar lever but an increasingly blunt one. Between 2020 and 2023, luxury brands raised prices by an average of 36% according to Bernstein, well above inflation, with Dior up 51% and Louis Vuitton up 32%. Bain has warned that those years of aggressive escalation have already alienated customers and threaten long-term growth.

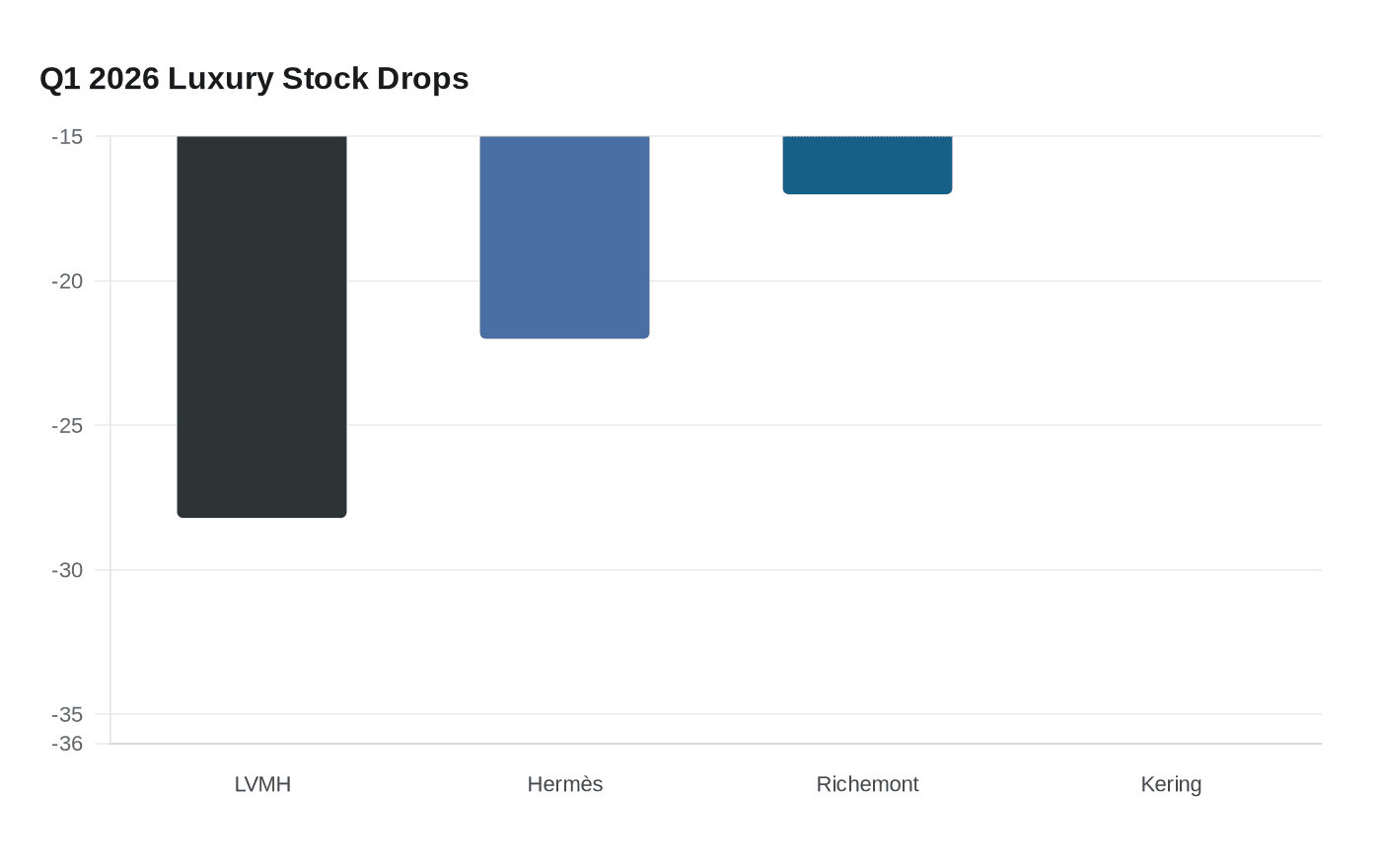

LVMH was not alone in its first-quarter pain. Hermès shed nearly 22%, Richemont fell 17%, and Kering dropped 12% over the same period, confirming the demand softening is structural rather than company-specific. The post-pandemic luxury boom, built on aspirational spending and a hoped-for Chinese recovery, normalized faster than the sector wanted.

For those who shop at the quieter end of luxury, that normalization has a practical consequence. If primary-market prices continue to climb at flagship boutiques while aspirational demand stays soft, a bifurcation opens: full price at the maison, selective markdowns through travel retail and wholesale channels. Fashion and leather goods, the division housing Louis Vuitton, Dior, and their quieter siblings, faces forecasts of low-single-digit or negative growth. When the houses that built their reputations on pricing discipline begin to crack that discipline under margin pressure, authenticated heritage pieces on the secondary market tend to look more rational, not less. The 28% quarterly drop is the market's way of saying that moment has arrived.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?