EU Textile Recycling Faces Sorting, Quality, and Demand Bottlenecks

The EU has the policy pressure, but recycling still stalls at the least glamorous step: sorting blended, dirty clothes into feedstock brands will actually buy.

The new EU textile brief

The European Union is no longer treating textile waste as a vague sustainability problem. Its 2030 vision is crisp and almost brutally practical: clothes should be durable, repairable, recyclable, and increasingly made from recycled fibres, because the current system throws away too much of what it makes. The scale is hard to ignore: the EU generates 12.6 million tonnes of textile waste a year, including 5.2 million tonnes of clothing and footwear, while less than 1% of textiles worldwide are recycled into new products.

That is why textile recycling in Europe has become an accountability story rather than a lifestyle story. The old language of consumer virtue does not explain why mountains of cast-off clothes still end up burned, buried, or exported. What matters now is whether the industry can build an operating system that turns discarded knits, jerseys, wovens, and blends into clean, repeatable industrial inputs, at a cost brands can actually carry.

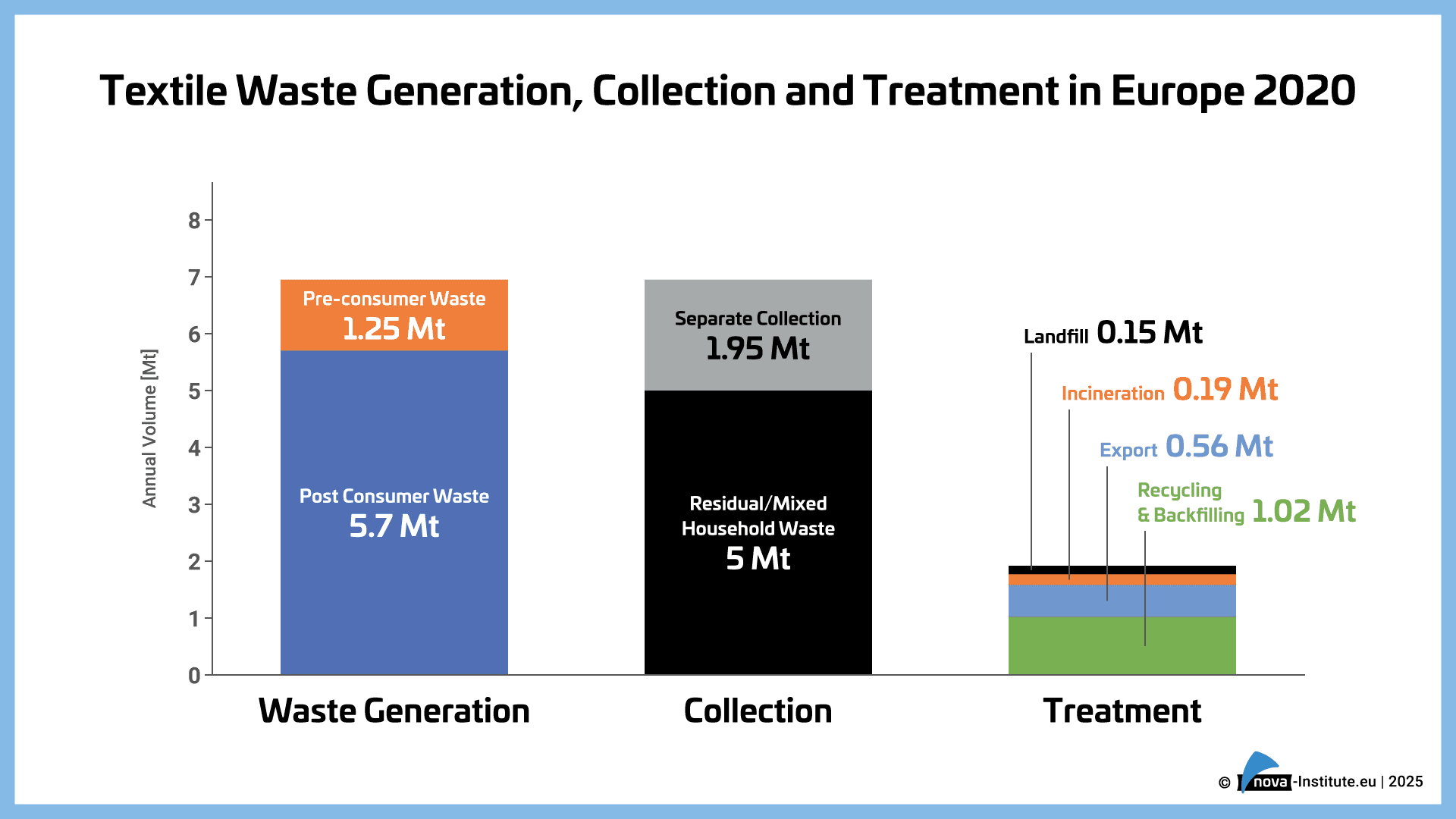

Where the chain breaks

The policy push is real. Separate textile collection was already meant to be mandatory across the EU by January 1, 2025, and lawmakers adopted new textile-waste rules in September 2025 that require producers placing textiles on the EU market to cover the costs of collecting, sorting, and recycling them. Member states then have 20 months to transpose those rules into national law, which means the pressure now shifts from Brussels into municipal systems, sorting facilities, and brand procurement teams.

But collection is only the first doorway. A bin on the street does not create recycled fibre any more than a rack creates a collection. Once garments are gathered, they still have to be sorted, stripped of hardware, separated by fibre type and quality, and prepared into feedstock that recyclers can use without ruining output or inflating costs. That middle stretch is where the system keeps catching on its own seams.

The hardest step: making feedstock clean enough

The single biggest bottleneck today is not the existence of recycling technology. It is the lack of clean, consistent, competitively priced post-consumer feedstock at scale. Fashion for Good launched Project FAE, or Feedstock Activation Europe, precisely because sorters cannot currently prepare post-consumer material at the price, quantity, and quality recyclers require. In other words, the fashion system has waste, but not enough recycler-ready waste.

That is where the fabric of the problem shows up, quite literally. Post-consumer textiles are highly heterogeneous and often blended, which makes them difficult to sort and even harder to recycle industrially. A dress can be a puzzle of polyester, cotton, elastane, thread, labels, zippers, coatings, and finishes, and every extra material raises the cost of separating usable fibres. A 2025 review of textile recycling found that mixed fibre compositions, quality degradation, and weak market demand for recycled fibres remain major barriers to scaling.

A sharp statistic reveals how narrow the funnel still is: BCG’s 2026 Europe analysis found that the region generated about 13.3 million tonnes of post-consumer textile waste in 2025, but only 1.5 million tonnes were collected and sorted, roughly one ton in nine. That is the reality behind the rhetoric. Even before fibre-to-fibre recycling begins, most of the material never becomes an industrially usable stream.

Why demand is still the other half of the problem

Even when recycled fibres can be produced, they still have to compete. The market does not absorb them automatically, because recycled textile feedstock often carries higher processing costs and more variable quality than virgin fibre. The 2025 review from Springer Nature said more than 80% of textile waste is still handled through landfilling or incineration, with only about 10% recycled, and it singled out economic feasibility and limited demand for recycled fibres as core constraints.

That demand problem is why the industry keeps talking about scale as a system, not a single technology. BCG and ReHubs estimate that a viable European textile-to-textile ecosystem would need to reach about 2.7 million tonnes of recycling a year by 2035, requiring roughly €8-11 billion in capital investment and €5-6.5 billion in recurring annual operating costs. Those numbers explain why recycled textile supply still falls short of brand ambitions: brands want circular fibres, but the market still has not built the collection, sorting, and pre-processing capacity to supply them in volume, consistently, at a price that competes with the old order.

What scale looks like now

This is why the current moment feels less like a trend cycle and more like industrial design. Project FAE is building regional sorting and pre-processing hubs across Europe, with adidas, BESTSELLER, and Inditex involved, because the missing infrastructure is no longer theoretical. The goal is not to make waste sound noble. It is to standardize, grade, and purify it until post-consumer textiles behave like a credible raw material.

That is the editorial truth of textile recycling in Europe: the policy frame exists, the waste stream is vast, and the technology is advancing, but the system still fails at the unglamorous middle. Until sorting is cheaper, feedstock is cleaner, and brands commit to buying recycled fibre at meaningful volume, the industry's circular dreams will remain beautifully cut, and structurally underfed.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?