Fashion CFOs Face Rising Climate Costs, Sustainability Becomes Balance-Sheet Issue

Climate risk is now a line item, not a slogan. Raw materials, EPR fees and litigation are forcing fashion CFOs to price the cost of waiting.

The balance-sheet reckoning

Sustainability has moved out of the mood board and onto the income statement. The blunt new reality is that climate disruption is raising the price of raw materials, extended producer responsibility is turning waste into a fee structure, and carbon pricing and litigation risk are becoming costs that finance teams can no longer treat as abstract.

That is the message behind *Fashion CFO Agenda 2026: Building Financial Resilience Through Sustainability*, the new guide from Global Fashion Agenda and Boston Consulting Group. Released at Global Fashion Summit: Copenhagen Edition 2026, it is aimed squarely at finance leaders, not branding teams, because the pressure points now sit in the ledger: margins, procurement, compliance and risk reserves.

The timing matters. Global Fashion Summit ran from May 5 to 7 at Copenhagen Concert Hall and brought together more than 1,000 stakeholders from brands, retailers, NGOs, policymakers, manufacturers, innovators and adjacent industries under the theme “Building Resilient Futures.” That phrase sounds aspirational until you look at the numbers. Fashion is no longer debating whether sustainability matters. It is pricing what happens when the industry delays.

What the CFOs are being asked to count

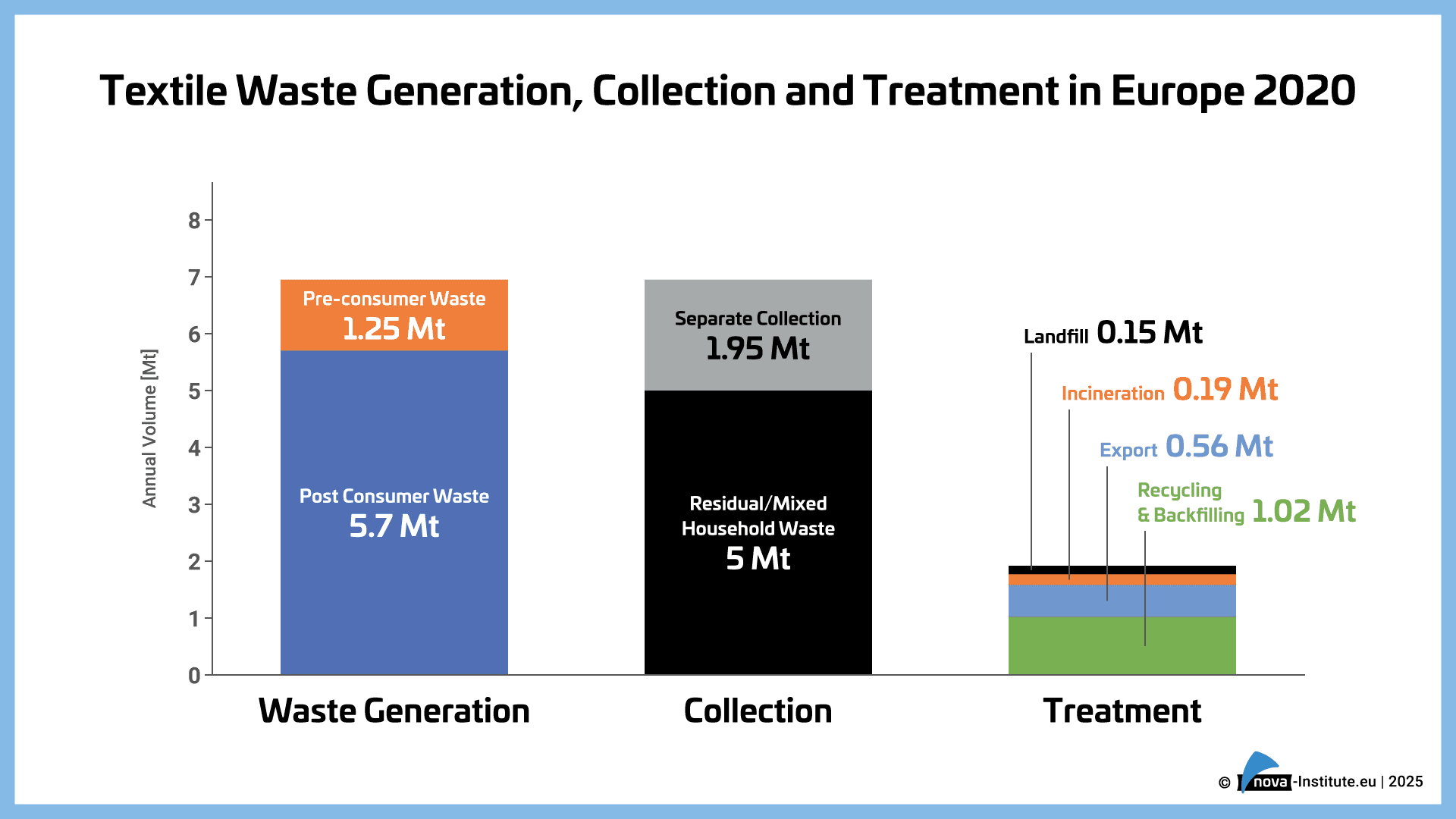

BCG says the report is built on engagement with more than 30 CFOs and senior executives and on an analysis of over 150 fashion brands. That matters because it shifts the conversation from broad ambition to measurable exposure. Over the next 12 to 24 months, the costs brands can most clearly quantify are the ones tied to inputs, waste and regulation, and the report is explicit about all three.

Start with materials. BCG says climate-related disruptions are already pushing up costs across fashion, with price spikes of up to two times for key raw materials such as cotton and wool. That is not a distant scenario, it is a procurement problem with direct consequences for gross margin, assortment planning and inventory strategy. If the fabric bill becomes volatile, everything from opening price points to seasonal buys starts to wobble.

Then comes extended producer responsibility. As textile EPR rules spread, BCG says large mass fashion players could see net profits reduced by roughly 4% by 2030. That figure is especially important because it turns a sustainability issue into a profitability issue. EPR fees do not live in a brand deck. They land in the same place as freight, labor and markdowns, and they force companies to decide whether to absorb the cost, redesign the product, or pass it on to shoppers already feeling pressure from inflation.

Carbon pricing and litigation risk sit beside those costs as quieter but increasingly serious line items. They may not hit every company with the same force, but they shape reserves, insurance decisions and long-term planning. Once those exposures are measured, sustainability stops being a communications exercise and becomes a finance discipline.

Why the old language is fading

The irony in all this is that the financial case for action is getting stronger just as sustainability is disappearing from the corporate conversation. BCG says sustainability mentions on fashion earnings calls have fallen by roughly one third since 2022, as companies focus on slower growth, AI adoption, earnings volatility and geopolitical uncertainty.

That silence is revealing. It suggests many brands are still treating sustainability as a side lane, even as the costs of climate disruption move straight into the main road. In a softer market, executives tend to talk about what feels most immediate. Right now that is growth, automation and volatility. But the report makes the case that sustainability is part of the volatility, not separate from it.

There is also a strategic shift underway inside the industry itself. Global Fashion Agenda chief sustainability officer Justin Pariag described a maturity shift from small investments in sustainable materials toward a real sustainable material strategy. That distinction matters. A few test capsules in recycled nylon or organic cotton are not the same thing as a sourcing model that can survive raw-material shocks, regulatory fees and margin pressure.

Federica Marchionni, Global Fashion Agenda’s chief executive, framed the moment as a crossroads for fashion, with climate disruption, economic uncertainty and rapid technological transformation all colliding at once. She is right to put those forces in the same sentence. The brands that keep treating them as separate conversations will keep paying for that fragmentation in different parts of the P&L.

Where the savings and growth still are

The most useful part of the report is that it does not position sustainability only as a cost. BCG says roughly 70% of fashion-sector greenhouse-gas emissions can be reduced at low cost or with cost savings, which means a large share of decarbonization is not a luxury spend. It is an efficiency play disguised as a climate strategy.

The report also argues that circular business models can deliver double-digit top-line growth. That is the kind of claim finance leaders notice because it moves the conversation beyond defense. Circularity is not just about avoiding waste. It can mean resale, repair, rental, redesign and better material recovery, all of which can create revenue while reducing dependence on virgin inputs.

Global Fashion Agenda’s broader mission points in the same direction. The organization says its impact goals are to reduce virgin resource use by 50%, ensure a living wage for all and eliminate emissions and pollution. Those are big structural aims, but they also map back to practical business questions: how much raw material do you need, how exposed are you to labor volatility, and how expensive will compliance become if you wait too long to redesign the system?

What fashion finance should be watching next

The smartest brands will treat the next 12 to 24 months as a testing ground for financial resilience, not a waiting period. The most immediate pressure points are already visible:

- Raw-material inflation tied to climate disruption, especially cotton and wool.

- EPR fees and waste obligations that will start to shape product economics.

- Carbon pricing exposure, which may not be uniform but will affect planning and reserves.

- Litigation risk, especially where disclosure and environmental claims meet legal scrutiny.

- Circular models that can widen the top line while lowering dependence on virgin inputs.

The old sustainability playbook asked fashion to justify itself morally. The new one is far less forgiving. It asks a harder question, and a more useful one: what happens to the business if you do nothing, and how quickly can you prove the cost of doing better?

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?