3D printer market splits, entry-level and industrial tiers surge

The old $3,000 to $20,000 comfort zone is getting squeezed as stronger cheap printers and true industrial systems pull buyers away from the middle.

Entry-level 3D printers priced at $2,500 or below captured 54% of all system revenues in CONTEXT’s July 9 analysis. The market is splitting into two places that actually make sense: cheap, capable desktop machines on one side, and real production hardware on the other. The weak spot is the old $2,500 to $20,000 comfort zone, where "good enough" no longer buys much. If you are shopping today, the real question is which tier still earns its price.

The market is no longer one broad middle

CONTEXT has tracked global 3D printer shipments since 2012, and its four-way split makes the pressure obvious: Industrial at $100,000 and up, Midrange at $20,000 to $100,000, Professional at $2,500 to $20,000, and Entry-level below $2,500. In its July 9 analysis, total hardware system revenues were up 32% year on year, while the Professional band fell 22% in shipments and 31% in revenue.

Buyers who want a home machine are moving toward affordable printers that are already good enough for multicolor work, enclosed chambers, ecosystem accessories, and polished software. Buyers with real production needs are skipping the middle entirely and going straight to industrial systems that justify their footprint with throughput, materials, and support.

The low end is not low capability anymore

The entry-level tier is being dominated by the same names that now shape expectations for the whole desktop market. Bambu Lab, Creality, Elegoo, and Anycubic together shipped 88% of the entry-level category, which is a big reason the floor keeps rising. In CONTEXT’s Q1 2025 data, entry-level printers shipped more than one million units globally, Chinese manufacturers accounted for 95% of those shipments, Bambu Lab posted a 64% year-on-year shipment increase, and Creality held 39% of the market by volume.

A first-time buyer is no longer choosing between a bargain machine and a serious machine. You are often choosing between a very capable sub-$1,000 desktop printer and a much more expensive box that only makes sense if you need a specific material stack, a more rigid production workflow, or support that a consumer brand cannot provide.

Why the $2,500 to $20,000 band is getting squeezed

The pattern spans more than one quarter. In Q2 2024, entry-level shipments grew 65% year on year and entry-level printers accounted for 48% of global system revenues, while industrial shipments fell 25% and professional revenues fell 21%. In Q1 2025, the pattern repeated in a slightly different form: entry-level surged again, industrial shipments were down 14%, and industrial revenue fell 6%.

CONTEXT’s latest split shows the pressure coming from both directions at once. At the bottom, consumer printers are better, cheaper, and easier to live with. At the top, production buyers are finding enough reason to leap over the middle. A printer that is merely decent at $5,000 or $12,000 has a hard time competing against a sub-$1,000 desktop that is good enough for everyday work, or against a six-figure industrial system that earns money in a factory.

Industrial is still healthy, just in a different way

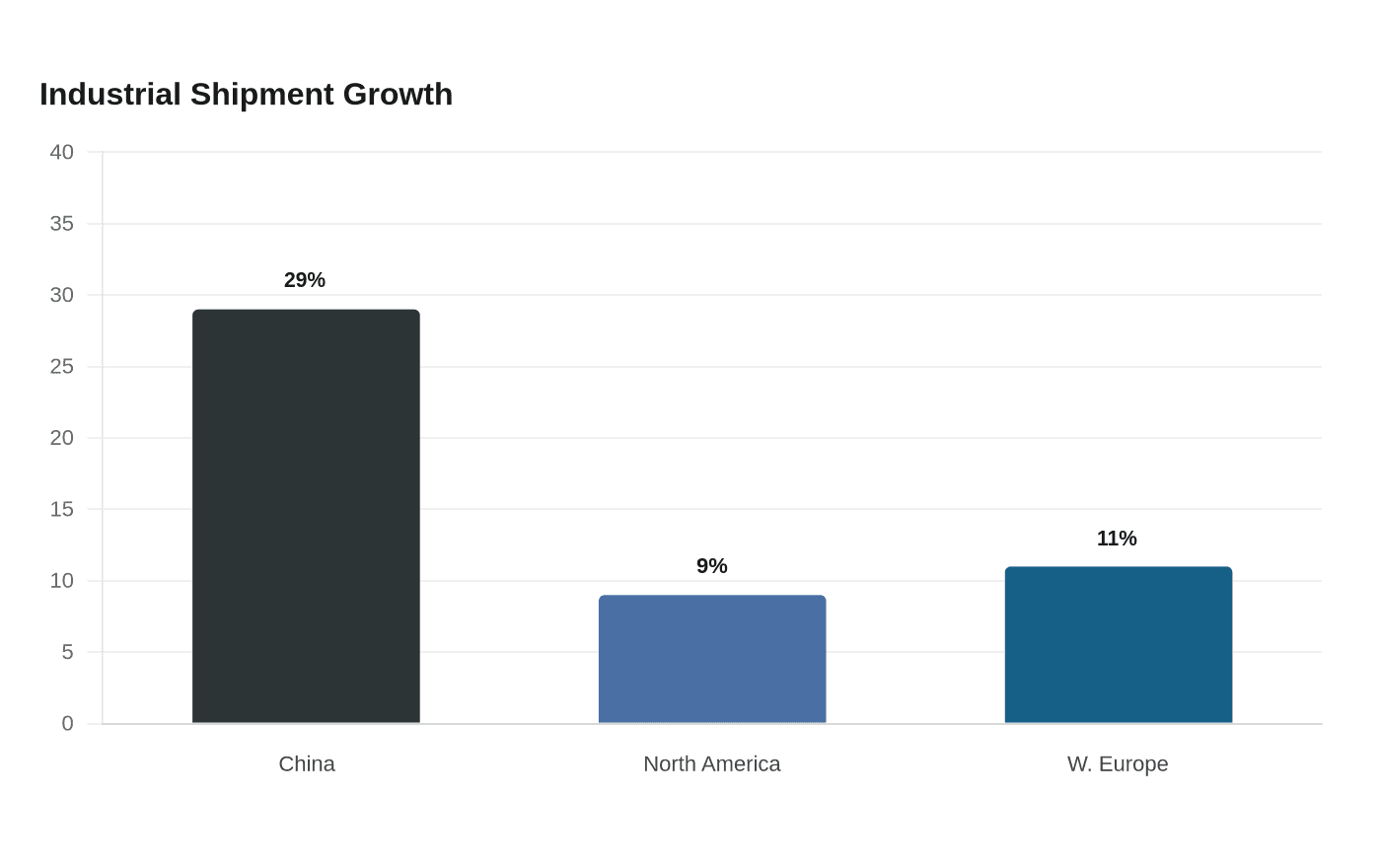

The industrial side is not fading. In CONTEXT’s Q1 2026 data, industrial systems posted their third consecutive quarter of growth after two years of declines, and industrial shipments rose across China by 29%, North America by 9%, and Western Europe by 11%. Industrial metal system shipments were up 10% year on year, and powder bed fusion accounted for 81% of the industrial metals market.

Chris Connery, CONTEXT’s vice president of global analysis, called the demand picture a "disparate demand outlook." Some vendors are seeing demand tied to global conflicts and defense initiatives, while others are still dealing with inflation, higher interest rates, and a sluggish European economy. CONTEXT’s July 9 report shows EOS more than doubled its metal shipments from a year earlier and separately announced the biggest contract in its history with a defense drone maker.

China remains the largest market for industrial shipments, and strong demand for Chinese industrial vendors such as HBD, Farsoon, and BLT has been helped by the 3C sector.

Who should still buy the prosumer middle

The $2,500 to $20,000 range still has a job, but it has to earn it. This is the range for buyers who need more than a hobby machine and less than a full production cell, especially when the machine has to bring something genuinely different to the table.

- If you need better reliability than a consumer printer but do not need a factory line, the middle can still make sense.

- If you care about a more validated material workflow, stronger support, or a genuinely differentiated toolchain, this is where that premium has to show up.

- If the selling point is only a nicer screen, a slightly stronger frame, or a prettier enclosure, the case is weak.

A smart buyer looking at a first machine can usually spend less and get more usable capability than before. A shop with real production needs is increasingly better off leaping higher, because industrial systems are the ones being pulled forward by defense, 3C, and high-volume manufacturing. The broad market is still forecast to sit somewhere between $28.55 billion and $34.85 billion in 2026.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?