3D Printing Revenues Jump 25%, Entry-Level and Industrial Shipments Rebound

Entry-level printers surged 47% and industrial shipments rose 12% in Q4 2025, pushing additive hardware revenue up 25% as the market split into two fast-moving tiers.

The 3D printing market ended 2025 looking healthier, but also more divided. CONTEXT said aggregated additive manufacturing hardware revenues rose 25% year over year in the fourth quarter, powered by a 47% jump in entry-level shipments and a 12% rebound in industrial systems. That translated into a 53% revenue increase for entry-level printers and a 16% lift for industrial hardware, a sign that the sector was no longer moving in one straight line.

The clearest engine remained the low-cost desktop side. CONTEXT said Chinese vendors accounted for more than 90% of global entry-level shipments in recent reporting, with Creality, Anycubic, Elegoo and Bambu Lab sitting at the center of that surge. Chris Connery said entry-level 3D printing has never been hotter, pointing to the energy buyers were bringing to the recent TCT Asia show in Shanghai. For a market that had spent much of the previous stretch grinding through weaker demand, that kind of volume matters because it keeps desktop ecosystems expanding even as more expensive categories cool.

Industrial printing also showed a real turn. CONTEXT said industrial system shipments rose 12% in the quarter, while metal powder bed fusion grew 24% in unit shipments. BLT, Eplus3D, ZRapid Tech and Farsoon led unit share in that segment, while EOS and Nikon SLM Solutions held the lead in revenue share. In China, UnionTech was singled out as a meaningful growth driver in metals, helped by demand in the shoe-mould market. Connery said the industrial high end had moved beyond the old "expansion-at-any-cost" mindset and was now focused on places where additive already delivered clear economic value, especially aerospace, defence and domestic Chinese manufacturing.

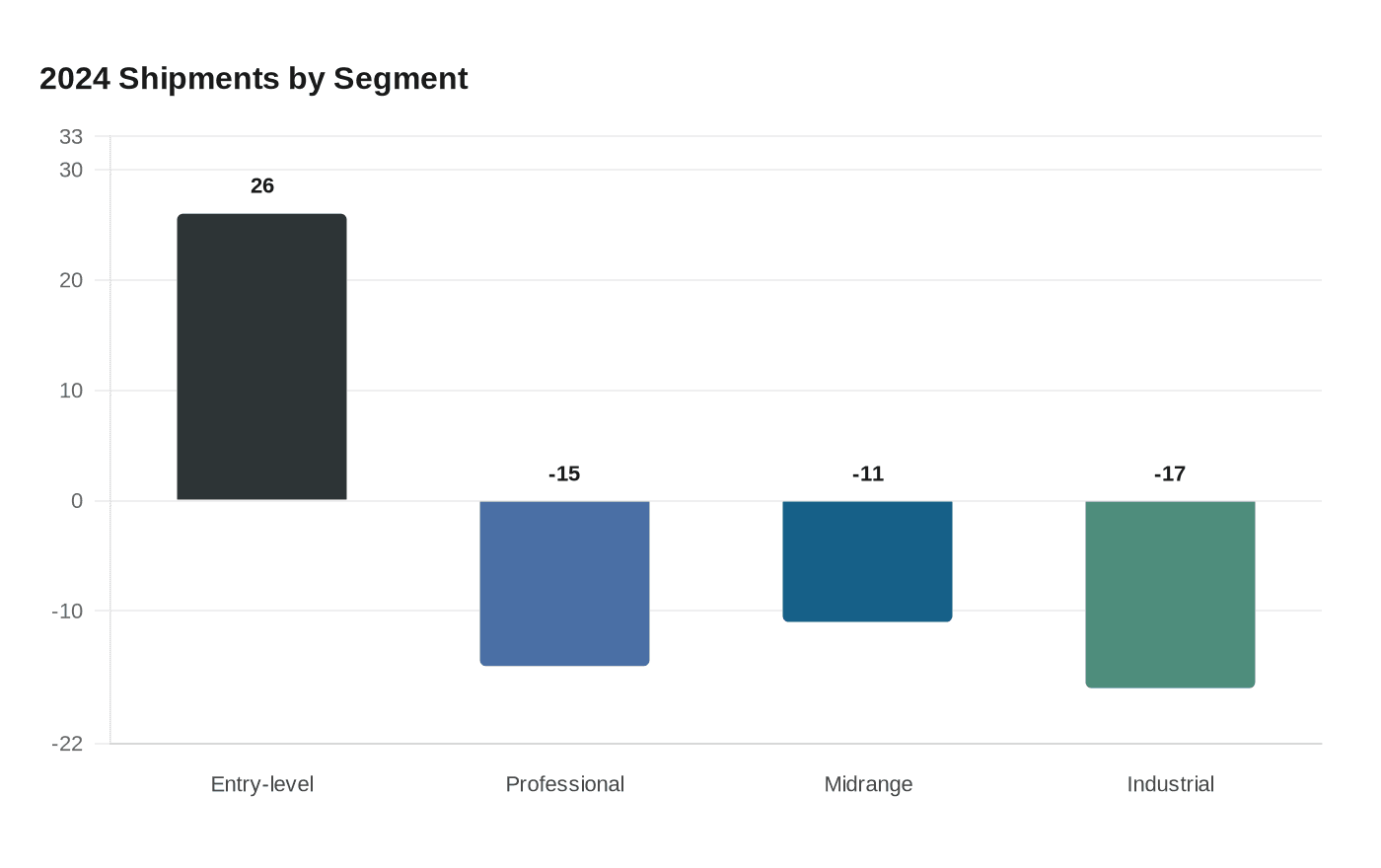

That recovery stands out because the market had been under real strain. In the third quarter of 2024, industrial shipments fell 24% year over year and midrange shipments dropped 8%, while entry-level printers still managed a 28% gain. For full-year 2024, entry-level shipments rose 26%, but professional systems fell 15%, midrange systems fell 11% and industrial systems fell 17%. CONTEXT also said the professional segment was down 14% in a recent quarter and the midrange segment down 13%, showing how demand continued to migrate toward cheaper machines.

The result is a printer market that is not simply polarizing. It is reorganizing around two strong poles, a fast-growing consumer tier and a recovering industrial tier, while the middle still feels pressure. CONTEXT-linked reporting says all key segments are expected to grow in 2026, with entry-level again leading and industrial shipments approaching double-digit growth.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?