Global 3D Printing Market Hits $16 Billion in 2025, Growth Momentum Returns

AM Research puts the global 3D printing market at $16B in 2025 with 10%+ growth, but consolidation is already reshaping the vendor field.

The $16 billion milestone matters less as a round number than as confirmation of something AM Research EVP Scott Dunham put plainly: 2025 was "a story of two markets." The first half dragged. The second half surged. And if you've been watching filament and resin availability tighten over the past two years while wondering when commercial investment would catch back up, AM Research's Q4 2025 market update has the answer.

The firm put total global additive manufacturing output at approximately $16 billion for 2025, representing year-over-year growth just above 10%. That's a meaningful acceleration from the slower pace of 2023 and 2024, and it came specifically in the back half of the year. Q4 alone climbed from $4.0 billion to $4.26 billion, a jump the report flagged as evidence of strengthening momentum heading into 2026. The longer-term projection points toward continued expansion well beyond the current figure by 2034, framing the current period as a transition from hype-driven experimentation to pragmatic, workflow-integrated adoption.

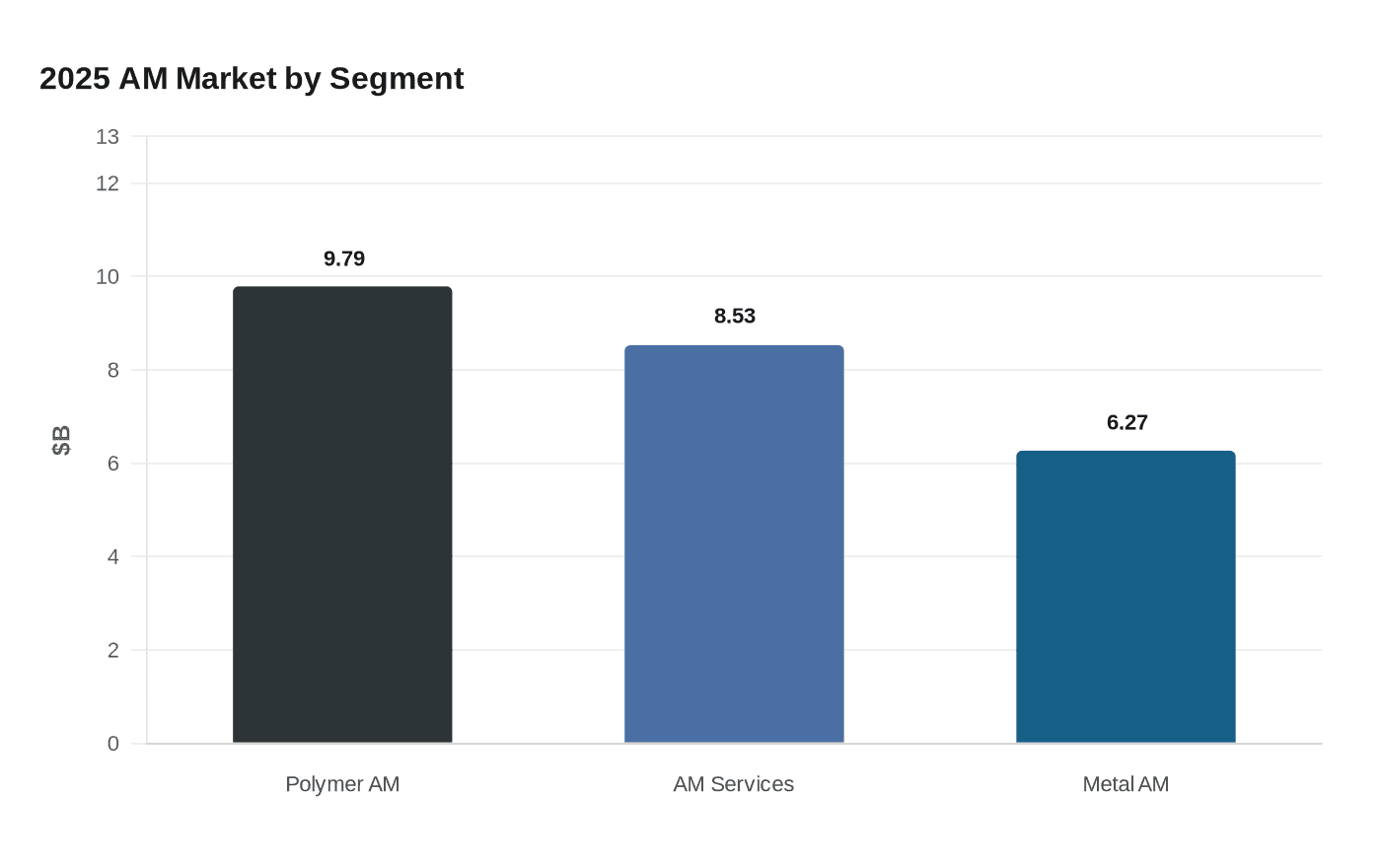

The segment breakdown gives a clearer picture of where the dollars are actually moving. Polymer AM led the field with $9.79 billion, which tracks with the sheer volume of FDM and resin output across desktop and industrial platforms worldwide. Metal AM reached $6.27 billion, driven heavily by medical implants, aerospace structures, and defense components where the per-part value makes additive economically competitive with or superior to traditional manufacturing. AM services came in at $8.53 billion, with the report acknowledging some overlap between categories in the methodology.

That services number deserves particular attention. AM Research projects the services segment will eventually overtake the others as more companies choose to outsource additive production rather than invest in in-house hardware and expertise. For anyone running a small service bureau or considering using one for short-run printing, that trajectory means more professional capacity, more mature post-processing options, and broader material availability through third-party providers. The shift toward services-led growth reflects what's already visible at the shop level: more customers want parts, not printers.

Dunham's description of the latter half of 2025 as "the start of a significant turnaround for AM" was measured, not triumphant. That framing matters because the same report that documented the recovery also documented exits. Several companies left the market in 2025, and AM Research expects industry rationalization to continue through 2026. The consolidation isn't a footnote; it's part of the same story as the growth.

The consolidation cuts two ways for desktop operators and small studios. On the upside, a healthier broader market pulls capital into materials research, slicer development, and integrated print-to-product workflows. The growing services segment in particular creates more mature options for makers who need professional output without industrial-scale hardware investment. On the downside, niche suppliers, the small independent filament brands and specialty resin formulators that serve specific community needs, are more exposed in rationalization cycles. Vendors that can't compete on volume or find a defensible specialty tend not to survive when larger players consolidate market share.

The AM Research framework positions 2025 not as a peak but as a base. The move from experimental to pragmatic adoption the firm describes means the technology is entering a phase where software integration, material consistency, and end-to-end workflow reliability matter more than raw printer specs. That's broadly good news for anyone building reliable production workflows at any scale, but it puts renewed pressure on hardware and material vendor choices. Platforms with staying power will get better resourced. Those that don't survive consolidation will leave users scrambling for compatible filament or discontinued resins.

The message from the numbers is clear: growth is back, but the market it's returning to is more selective than the one it left.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?