Rabobank Forecasts Record 180 Million-Bag Global Coffee Crop for 2026/27

Rabobank forecasts a record 180 million-bag global crop for 2026/27, with Arabica already at a 16-month price low; freight costs may keep your café bill stubbornly high.

The world's coffee trees are set to deliver more beans than they ever have, and green-bean prices are already reflecting it. Rabobank projected on March 4 that global coffee production will reach a record 180 million 60-kg bags in 2026/27, up about 8 million bags from the prior season, driven almost entirely by Brazil's biennial on-year cycle. That forecast, combined with ICE Arabica certified stocks rebuilding on exchange warehouses, helped push New York Arabica futures to a 16-month low on February 24 before a partial rebound. Rabobank now projects the first meaningful global surplus in five years: 7 to 10 million bags for 2026/27, ending a three-season run of cumulative deficits that totaled 14.6 million bags and had lifted Arabica above US$4.40/lb in early 2025.

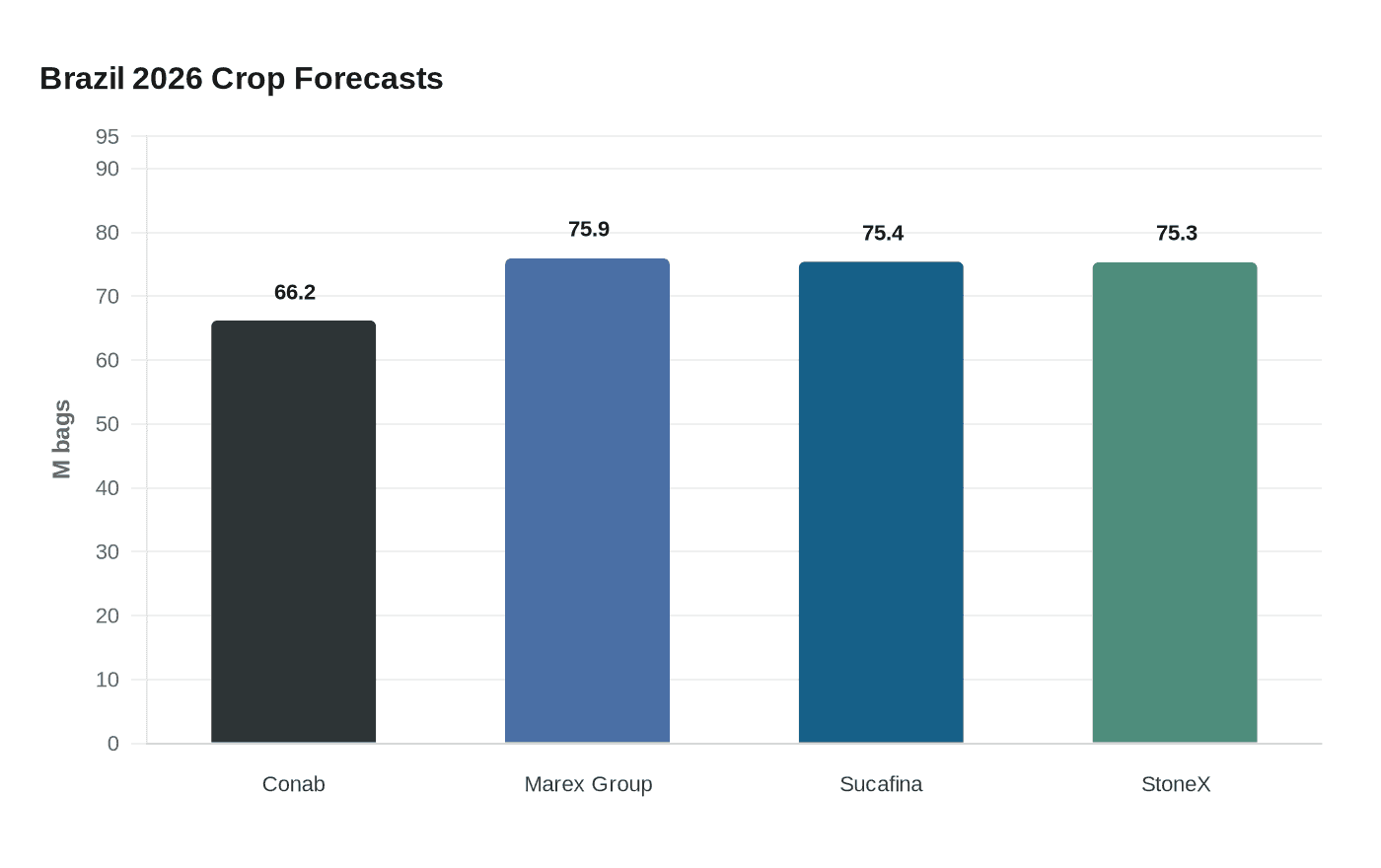

Brazil's supply picture is where forecasters diverge most sharply. Conab, Brazil's official crop agency, said on February 5 that the 2026 harvest will reach 66.2 million bags, a 17.2% year-on-year gain, split between Arabica up 23.2% to 44.1 million bags and Conilon up 6.3% to 22.1 million bags. Commercial analysts run considerably higher: Marex Group projected 75.9 million bags for Brazil 2026/27, above Sucafina's 75.4 million and StoneX's revised 75.3 million, raised from 70.7 million in November. Season-definition and methodology differences likely explain part of the spread, but every major forecaster now points to a record. Hedgepoint Global Markets puts Brazilian exports at nearly 47 million bags in the 2026/27 July-to-June harvest year, which would eclipse the current export record of 46 million bags set in 2023/24.

On February 25, the ICE Arabica May contract closed in New York at 284.85 cents per pound. Rabobank attributed the broader price slide to "optimistic production prospects, combined with the gradual replenishment of ICE Arabica certified stocks," while cautioning that "speculative fund liquidations" have exacerbated the fall and "an upward correction in the short term cannot be ruled out." Producers are already rushing sales while buyers hold back, waiting for the surplus to land. The World Bank's longer view aligns directionally: it projects Arabica prices falling 13% in 2026 and a further 5% in 2027 as Brazil, Vietnam, and Ethiopia all post higher yields.

None of that necessarily means cheaper coffee at your roaster or local café. Foodingredientsfirst flagged that the Strait of Hormuz closure amid the Iran war is pushing freight rates, insurance premiums, and fuel costs higher at exactly the moment the supply picture looks most benign. Logistics costs of that kind can absorb a significant portion of any futures-market discount before it reaches a green-coffee invoice. Rabobank itself pegs the Arabica landing zone at US$2.50 to US$3.00 per pound by late 2026, still above pre-2022 norms, and expects no return to contango in Arabica futures before December 2026, when larger volumes from Brazil's new harvest begin arriving at destination warehouses in scale.

For those tracking the buying window, the sharpest milestones over the next six to twelve months are Conab's next crop revision, weekly ICE-certified Arabica stock reports for evidence that exchange-warehouse replenishment is accelerating, and the sequence of updates from Marex, StoneX, and Sucafina as the Brazilian harvest progresses through the second half of the year. Rabobank's December 2026 contango trigger is the clearest structural signal: when the Arabica futures curve normalizes, it will confirm that Brazil's record volumes have arrived at destination in scale and the projected surplus has become the market's new reality.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?