Smucker Q3 Sales Rise on Coffee Price Hikes, Cuts Forecast After Fire

Smucker's Q3 net sales climbed to $2,339.4M as U.S. Retail Coffee surged 23% to $908.2M on price hikes, but the company cut full-year sales growth guidance after a recent plant fire.

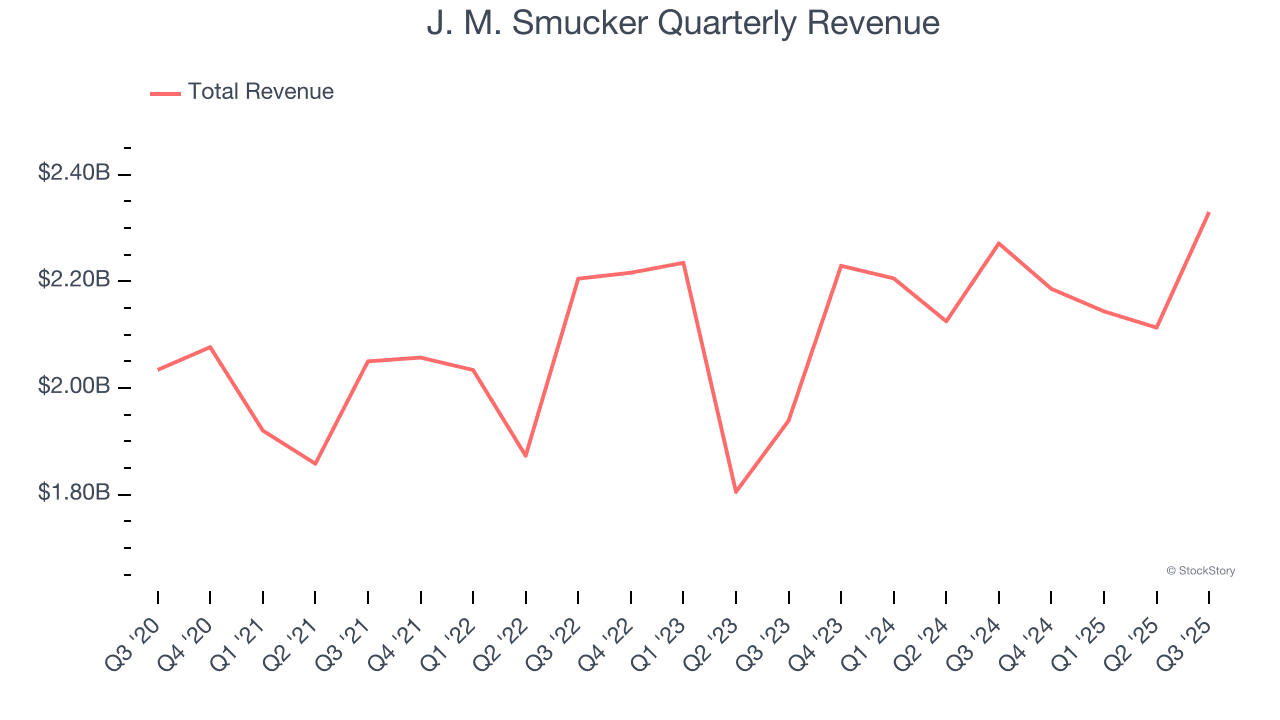

J.M. Smucker reports third-quarter fiscal 2026 net sales of $2,339.4 million, up 7% year over year and above a Zacks consensus of $2,324 million, driven largely by pricing in its coffee business. Management says comparable net sales rose 8% excluding prior-year divestitures and foreign exchange, with a 10 percentage point contribution from net price realization and a 2 percentage point drag from volume and mix.

The U.S. Retail Coffee segment was the standout, with net sales of $908.2 million, a 23% increase equivalent to $167.6 million. Smucker attributes that gain to pricing: net price realization increased net sales by 23 percentage points across Folgers, Dunkin' and Café Bustelo brands. Volume and mix trimmed results by 1 percentage point, reflecting softness in Dunkin' and Folgers that was partially offset by gains for Café Bustelo. Segment profit declined 5% to $199.0 million and segment margin fell to 21.9%, down 630 basis points as higher green coffee costs and tariff impacts more than offset pricing benefits.

Company-wide profitability shows strain from commodity and trade headwinds. Adjusted gross profit decreased 3%, which Smucker links to elevated green coffee costs, tariff expense and unfavorable volume/mix; the company notes pricing actions partly mitigated those pressures. Adjusted earnings and net sales outpaced the company’s internal-reported consensus targets for the quarter, though the releases do not disclose an exact adjusted EPS figure.

A separate business unit in the company’s results posted a 12% net sales increase, rising $36.7 million; excluding $2.0 million of favorable foreign currency exchange the improvement was $34.7 million, or 12%. For that unit, net price realization added 11 percentage points while volume/mix was neutral as increases in Uncrustables sandwiches and coffee offset declines in fruit spreads, portion control products, cat food and peanut butter. Segment profit for that row rose by $10.4 million, reflecting higher net price realization partially offset by higher costs, tariffs and unfavorable mix.

Smucker also announced it has lowered its full-year sales growth forecast due to a recent fire at one of its manufacturing facilities. The company’s disclosures do not provide the date, location, name of the plant, extent of damage, or a quantified revision to guidance; Smucker has not supplied an estimated financial impact tied to the incident in the materials released with the quarter.

Investors reacted to the release with a notable equity move in intraday trading, and Smucker emphasizes that as the operating environment remains dynamic it will continue to prioritize driving organic growth, strengthening margins and maintaining disciplined capital allocation. For now, higher coffee pricing has bolstered top-line results, while green coffee costs, tariff expense and the factory fire inject uncertainty into margins and full-year projections.

Know something we missed? Have a correction or additional information?

Submit a Tip