Vietnam Coffee Chains Slow Expansion, Focus on Efficiency and Margins

Vietnam’s café boom is entering cleanup mode. Big chains are closing stores, trimming menus and chasing margins instead of chasing every empty corner.

Margin pressure is finally showing up in Vietnam’s café map

After years of aggressive expansion, Vietnam’s best-known coffee and bubble tea chains are shrinking their footprints. That is the real story here: a market that once rewarded pure outlet count is now forcing operators to prove each store can earn its keep, and the shift is showing up in closures, smaller formats, tighter menus and a much harder eye on operating costs.

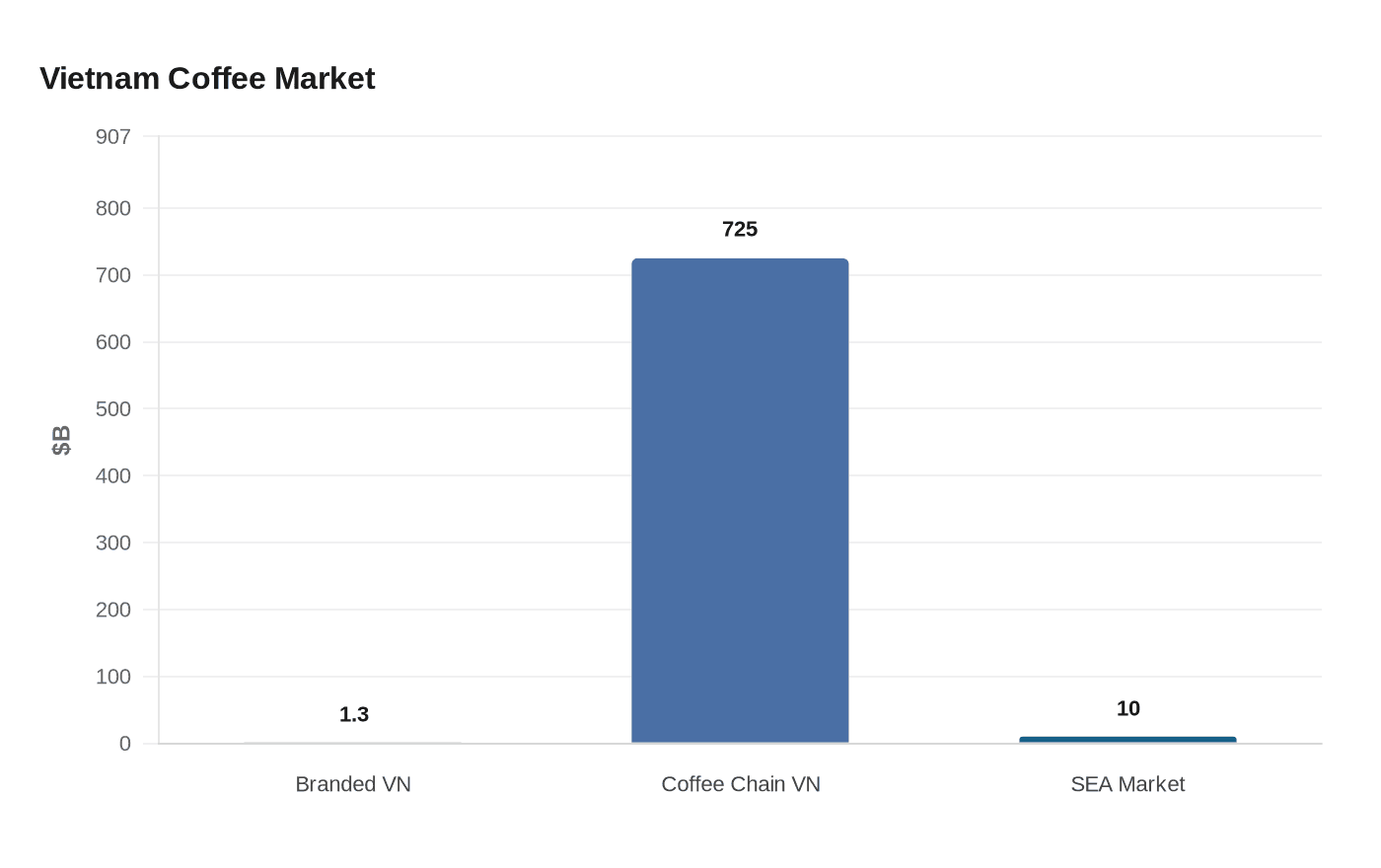

The numbers still look big. Vietnam’s branded coffee and milk tea shop market is now worth more than US$1.3 billion, and Momentum Works says the coffee-chain segment alone reached US$725 million in 2025, up 27% year on year. Across Southeast Asia, the coffee and tea chain market was worth nearly US$10 billion in 2025. But in Vietnam, growth is no longer just about planting more signs on more street corners. It is about margins.

What the pullback looks like in practice

Mixue is the clearest example of the pivot. The Chinese beverage chain entered Vietnam in 2018 and had reached around 1,000 outlets in the country by 2023, helped by low-priced drinks that Tuoi Tre says usually sold for about VND25,000 to 30,000, or roughly US$0.94 to US$1.13. Now the brand says it has closed more than 400 stores under the Mixue name, mainly in Indonesia and Vietnam, as part of efforts to optimize operations.

That kind of correction tells you a lot about the current market. The playbook is no longer “open everywhere and let demand catch up.” It is “keep the locations that work, cut the ones that do not, and make the remaining network leaner.” In practical terms, that usually means fewer deadweight stores, more disciplined site selection, and less tolerance for outlets that look busy on weekends but bleed cash on weekdays.

The broader market is crowded enough that this correction was inevitable. Tuoi Tre also reported that Vietdata counted nearly 500 Toco Toco milk-tea outlets in 2023, while Ding Tea had around 200 stores. Those are not niche numbers. They are proof that the beverage boom spread fast, then ran into the real wall every chain eventually hits: rent, labor, ingredients and too many similar cups chasing the same customers.

A market crowded with too many doors

Vietnam’s café scene is massive at the street level too. Mibrand data cited by Vietnam News puts the country at more than 500,000 coffee shops as of early 2025. At the same time, the General Statistics Office said more than 58,300 businesses withdrew from the market in January 2025 alone, an 8.1% increase year on year. That is the kind of backdrop where weak operators get exposed fast.

The pressure is not just on branded chains. iPOS says Vietnam’s coffee market was worth about US$510 million in 2024 and is projected to reach US$765 million by 2029, but that growth is coming with a cost. The iPOS and Nestlé Professional 2024 F&B report, built from research across 4,005 restaurants and cafés, 4,453 consumers nationwide and nearly 100 experts and business leaders, said revenue kept rising while profits were squeezed by higher input costs. That is the trap: more sales do not automatically mean better businesses.

For coffee drinkers, this changes the market in two directions at once. On one hand, surviving chains will likely get sharper about consistency, waste and inventory. On the other, some neighborhoods may lose the convenience of having a branded café on every block. When the rent no longer works, the weakest location disappears first.

The big names are still growing, but differently

This is not a retreat from the category. It is a change in the way the category is trying to win. Mibrand CEO Li Tin Mnh has pointed to the post-pandemic period, when remote work made cafés attractive as workspaces and Decree 100 pushed more people toward non-alcoholic drinks, as one reason the sector grew so quickly. Brand Finance Vietnam General Manager Lương Thuý Quyên has also argued that competition is forcing brands to innovate and differentiate.

You can see that in the way the biggest players have behaved. Highlands Coffee, Phúc Long, Starbucks and Katinat have all competed for share with different formats and expansion strategies, but the emphasis is no longer just on opening more shops. Highlands Coffee had 605 outlets at the end of 2022 and more than 170 additional stores by mid-2023. A March 2026 report cited by Vietnam News said Highlands Coffee had 985 stores and revenue growth of nearly 16% in 2025. That is a large network, but it is also a sign that scale now has to be defended with better execution.

Phúc Long has leaned into a different kind of buildout. It opened about 25 flagship stores in the last six months of 2023 and spent VND500 billion on a roasting factory in Bà Ra-Vũng Tàu. That kind of investment matters because it shows where the battle is moving: not only on the sales floor, but also in roasting, sourcing and supply control. Milano Coffee, meanwhile, had about 2,500 outlets nationwide in 2025, the largest network in Vietnam, and the report said it was the only brand to have passed the 1,000-store mark in Vietnam. That makes Milano the clearest proof that distribution still matters, but it also underlines how rare true national scale has become.

What it means for specialty coffee and independents

For specialty cafés and independents, the reset creates a real opening. When the big chains stop spraying stores across every district, customers have more room to notice places with better beans, better milk prep, a more thoughtful roast profile or simply a room that feels less assembly-line. A market obsessed with network size can drown out nuance; a market obsessed with margins usually lets nuance breathe again.

But do not mistake a pullback for an easy win. The chains are not disappearing, and the category is still growing. What changes is the standard. The next round of competition in Vietnam is being built around operational efficiency, digital infrastructure and supply-chain optimization, not just signboard count. That favors operators who know their labor model, control their waste and can keep quality steady without overbuilding.

That is why Vietnam’s café boom feels different now. The land grab phase is giving way to a more disciplined market, and the winners will be the ones that can make every store, every cup and every gram of coffee pay for itself.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?