EU Canners Cut Frozen Tuna Imports, Shift Toward Pre-Cooked Loins

EU canners slashed fresh air-flown tuna imports by over 45% in Q1 2025, pivoting hard to pre-cooked loins as processed tuna volumes smashed records at 225,558 tonnes.

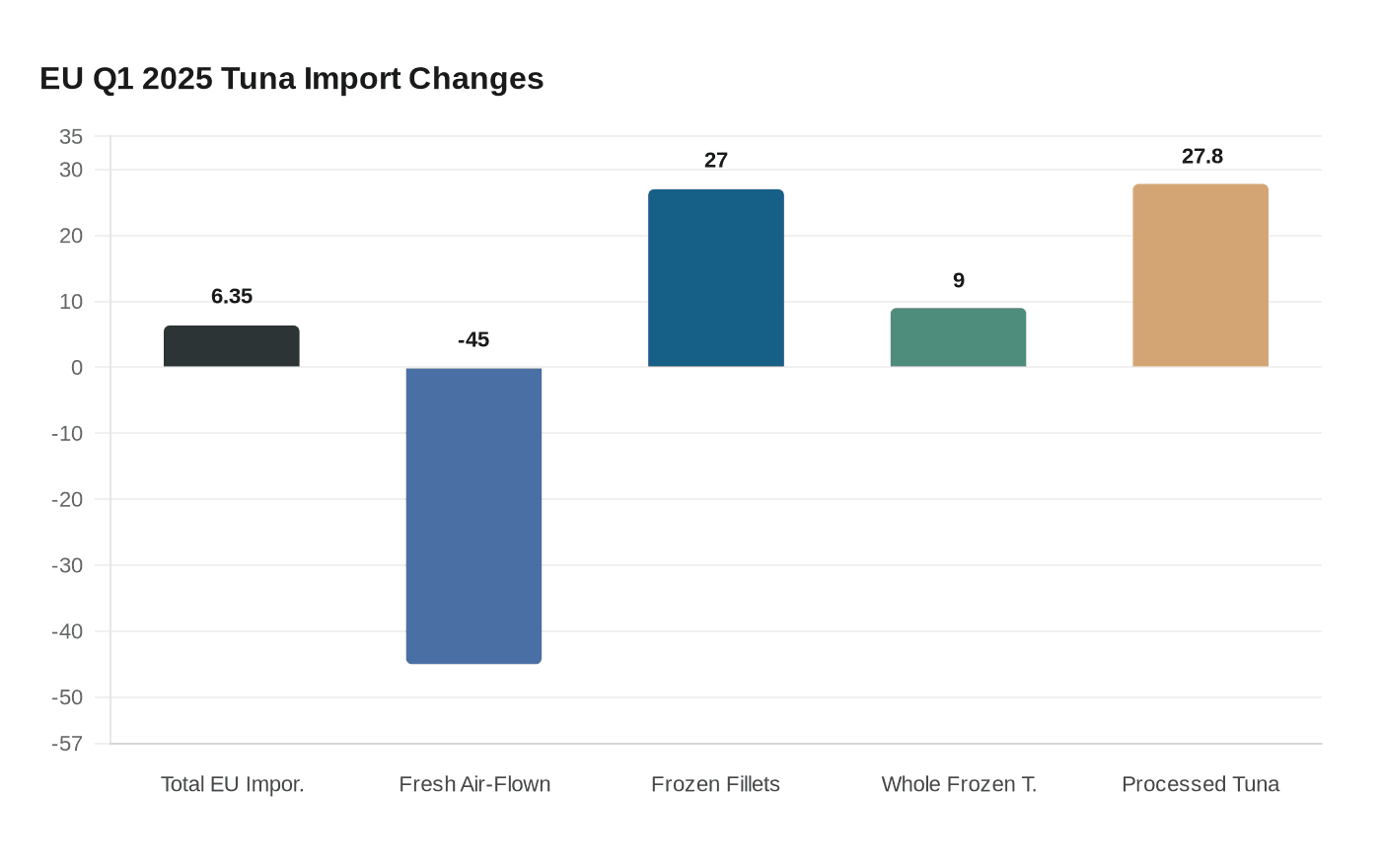

European tuna canners made a decisive break from whole frozen yellowfin and skipjack as raw material in early 2025, cutting purchases in favor of pre-cooked loins amid shifting supply flows from the Seychelles and Spain. The pivot showed up clearly in Q1 2025 trade figures tracked by 3MMI Europe: the same trend was observed among European tuna packers, whose supplies primarily originate from the Indian and Atlantic Oceans. Total EU tuna imports for the quarter reached 68,668 tonnes, up 6.35% year-on-year, but the headline number obscures a far more dramatic reshuffling of product formats underneath it.

Fresh, air-flown volumes, covering bluefin, bigeye, and yellowfin tuna, collapsed by more than 45% on weaker demand. At the same time, imports of frozen fillets, largely yellowfin and bigeye, surged nearly 27%, and whole frozen tuna, dominated by skipjack destined for canning lines, rose 9%. The real movement, though, was in processed formats. The EU imported 225,558 tonnes of processed tuna in Q1 alone, a 27.8% jump compared to the same period in 2024, with 83,809 tonnes of that total consisting of cooked frozen loins described by 3MMI Europe as "a key input for European canneries."

It is common practice in the European canning industry to perform all the processing up to tuna loin production as close as possible to the landing areas in developing countries, then export the semi-processed product, frozen pre-cooked tuna loins for canning, to canneries in developed countries. The Q1 2025 data shows that preference hardening into a clear procurement strategy, with canners moving away from the labor and yield costs of processing whole frozen fish in-house. Labour costs for processing raw material in Europe are usually higher than elsewhere, and if canners choose to process tuna themselves, they would incur production losses; yields for skipjack and yellowfin are normally between 50% and 55%, with most losses happening in deboning and cleaning.

Spain illustrated the split personality of the European market in Q1 2025. Canned tuna imports nearly doubled to approximately 70,000 tonnes compared to the prior year, reclaiming Spain's role as the continent's primary processing and redistribution hub. Italy grew its canned tuna imports by roughly 30% to around 42,190 tonnes over the same period, while Germany, France, and the UK each posted double-digit gains. Spain itself is a major actor: not only does it catch tuna globally, but it processes significant quantities in domestic factories, particularly in Galicia. Yet across the broader January-to-September 2025 window tracked by Infofish Trade News, Spain actually reduced its imports of whole frozen tuna, while Portugal, Italy, and France recorded higher volumes of whole frozen material, pointing to a partial rebalancing of raw material flows within the region.

The European shift toward processed inputs fits a wider global contraction in whole frozen tuna trade. Revised data for January-September 2025 showed global imports of whole frozen tuna, used primarily as raw material for canning, declined 9.21% year-on-year to 1.68 million MT. Frozen skipjack prices recorded a rising trend despite weaker demand for end-products in international trade, as well as from the large tuna canning industry in Thailand, and global uncertainty related to wide-ranging tariffs announced by the United States. In Asia, whole frozen imports fell across several major processing hubs including Thailand, Vietnam, the Philippines, and China, though Thailand retained its position as the world's largest importer of whole frozen tuna despite a sharp year-on-year decline. Japan moved in the opposite direction, lifting whole frozen imports to 165,478 MT from 148,565 MT a year earlier. Ecuador also recorded an increase in frozen tuna imports during the period, having been granted duty-free access for tuna products to the EU, making it a key supplier to Europe, exporting frozen yellowfin loins, both raw and cooked, to Spain, Italy, and other markets.

For the EU canning industry, the Q1 2025 numbers signal that the preference for shelf-stable, ready-to-process inputs over whole frozen round fish is no longer a marginal trend. With 83,809 tonnes of cooked loins flowing into European canneries in a single quarter and processed tuna volumes up more than a quarter year-on-year, the procurement model is changing in a way that will continue to reshape sourcing relationships from the Seychelles and the Atlantic to the Eastern Pacific.

Know something we missed? Have a correction or additional information?

Submit a Tip